This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Notably, the work-from-home movement has resulted in a dramatic drop in office valuations that could lead to a whole host of issues, including lending constraints in the banking sector, which is already sitting on a mountain of unrealized losses on Treasuries and mortgages.

In my third post at the start of 2023, I looked at US treasuries, the long-touted haven of safety for investors. In 2022, they were in the eye on the storm, with the ten-year US treasury bond depreciating in price by more than 19% during the year, the worst year for US treasury returns in a century.

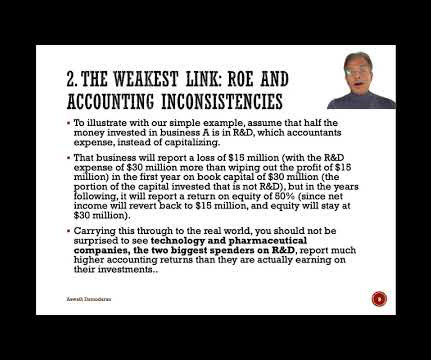

The first was the response that I received to my last data update , where I looked at the profitability of businesses, and specifically at how a comparison of accounting returns on equity (capital) to costs of equity (capital) can yield a measure of excess returns.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post. For an investment to be risk free then, it has to meet two conditions.

RITHOLTZ: And those were Treasuries. And so, you know, it was relatively, I wouldn’t say straightforward because I don’t think generating consistent profits has ever been something that’s so straightforward or so easy. RITHOLTZ: Like, very different universe, right? TROPIN: Right. TROPIN: Yeah. No, no, no.

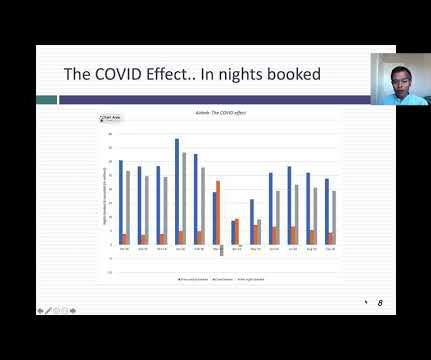

Setting the Table As with any valuation, the first step in valuing Airbnb is trying to understand its history and its business model, including how it has navigated the economic consequences of the COVID. In addition, growth in the experiences business will also push this metric upwards, since Airbnb keeps a 20% share of those revenues.

If revenue goes up, if profits go up, stock prices are going to go up. The, the longest period we had in our data was 17 years of losses of purchasing power, so after inflation, purchasing power. How should investors think about equities when valuations are a little elevated? for inflation. Barry Ritholtz : Right?

And while Chinese holdings of US Treasuries have declined notably since the pandemic, China’s holdings of agency securities and US corporate equities have picked up of late, though some of this is simply down to valuation increase.” Ryan, Deutsche Bank: China is holding fewer US treasuries and more agency and corporate securities.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. It is very likely that these rules of thumb were developed from data and observation, but at a different point in time.

While the value crowd, bereft of victories for a long time, may be inclined to do a victory dance, it is worth noting that the same phenomenon occurred between February and March of 2020, at the start of the COVID crisis, but that growth companies quickly recouped their losses and finished ahead of mature companies by the end of 2020.

While the value crowd, bereft of victories for a long time, may be inclined to do a victory dance, it is worth noting that the same phenomenon occurred between February and March of 2020, at the start of the COVID crisis, but that growth companies quickly recouped their losses and finished ahead of mature companies by the end of 2020.

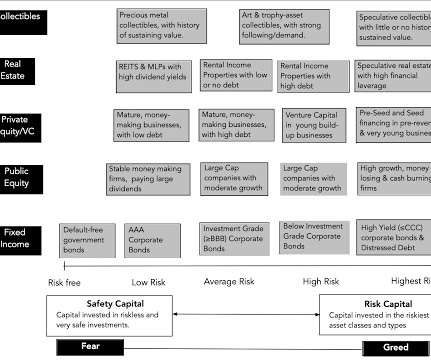

For others, it can be the portion of their capital with the longest time horizon (pension fund savings or 401Ks, if you are a young investor, for example), where they believe that any losses on risk capital can be made up over time. There are two macro factors that will come into play, and both are in play in markets today.

For others, it can be the portion of their capital with the longest time horizon (pension fund savings or 401Ks, if you are a young investor, for example), where they believe that any losses on risk capital can be made up over time. There are two macro factors that will come into play, and both are in play in markets today.

While private valuations have soared in recent years, public markets continue to be less kind to RIAs. Outside of work, he serves as a volunteer financial planner and class instructor for non-profits in the Northern Virginia area. Enjoy the ‘light’ reading! Author: Adam Van Deusen. Team Kitces. He can be reached at [email protected].

And they go on longer and longer and obviously more profitable for the states that run the lottery. But it makes a big, big difference to your long-term outcomes if you can just avoid those big losses. Then the volatility and, and the valuation makes an enormous difference. That’s the $2 that the lottery is worth for me.

He developed the Ginnie Mae contract, which at one time was a big thing in treasury bond contract. They announced a $640 million loss and ouch. But if, if it has a history of not being profitable, you you really want to exclude that. The visibility on earnings they grew but they stayed profitable as, as they grew.

I had no money back in 87, but certainly, you know, some of the managing directors and other people that had some money, they, they made quite a, quite a bit of of profits on, on some of the left for dead Microsoft and others that were just, you know, sold to very low levels as 00:06:28 [Speaker Changed] Opposed.

He sunk all the profits into Bitcoin, he’s levered up and borrowed money and bought Bitcoin. The profits are very small, but Alameda’s cost of capital was very low since they were borrowing all the customer money. Put it in Riskless Treasuries. They release their profits every quarter. That’s right.

We participated in that with treasury and FHFA and the regulators, the White House. And so, so we sort of felt pretty stupid for a while because we did a lot of losing trades in 2006 that were the, you know, that obviously didn’t come to fruition until the actual people could see the losses. The homes are here.

Blue-collar workers in developed markets : The flip side of the rise of China and other countries as manufacturing hubs, with lower costs of operation, has been the loss of manufacturing clout and jobs for the West, with factory workers in the United States, UK and Europe bearing the brunt of the cost.

And, you know, therein began, I think the unraveling and, and a little bit of the, the loss of that, you know, cultural juice that had kind of historically made that firm special. And when we experience a loss, right, a 50% loss can happen right? I don’t wanna experience loss. In a very short period of time.

00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. And instead of replacing a house, you’re replacing exposure like the s and p 500 or treasuries, where historically it’s been really hard to beat the market.

So, for example, the treasury was thinking about moving to direct deposit, but they wanted to know how much it was gonna cost them because direct deposit, they, they, they, they, the money clears, you know, sorry, almost instantly, right? So they wanna know how many days does it take a, a treasury check to get back to us.

Now you have to assume some losses. Barry Ritholtz : And these bonds are still profitable Jeffrey Sherman : And they don’t break, like they, they don’t, they don’t, they don’t lose money, especially at 50 cents on dollar. And you know, it’s the same thing when valuation gets outta control too.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content