This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

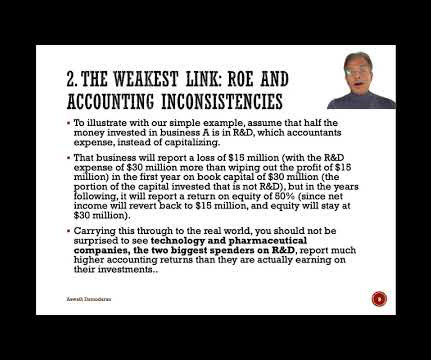

The first was the response that I received to my last data update , where I looked at the profitability of businesses, and specifically at how a comparison of accounting returns on equity (capital) to costs of equity (capital) can yield a measure of excess returns.

While the value crowd, bereft of victories for a long time, may be inclined to do a victory dance, it is worth noting that the same phenomenon occurred between February and March of 2020, at the start of the COVID crisis, but that growth companies quickly recouped their losses and finished ahead of mature companies by the end of 2020.

While the value crowd, bereft of victories for a long time, may be inclined to do a victory dance, it is worth noting that the same phenomenon occurred between February and March of 2020, at the start of the COVID crisis, but that growth companies quickly recouped their losses and finished ahead of mature companies by the end of 2020.

He developed the Ginnie Mae contract, which at one time was a big thing in treasury bond contract. They announced a $640 million loss and ouch. But if, if it has a history of not being profitable, you you really want to exclude that. The visibility on earnings they grew but they stayed profitable as, as they grew.

But as a private equity owner, again, first of all, you do invest heavily of your own money in the transactions, plus you have additional ownership through, you know, the carried interest, the profits interests. September 13, 1981, I think the 10-year Treasury was 15.84 You got 60 percent of losses ahead of you. RITHOLTZ: Yeah.

Blue-collar workers in developed markets : The flip side of the rise of China and other countries as manufacturing hubs, with lower costs of operation, has been the loss of manufacturing clout and jobs for the West, with factory workers in the United States, UK and Europe bearing the brunt of the cost.

Profiteering fraud. It just, the, the, the profiteering really was utterly insane. That the focus on profits, on pleasing shareholders and on profits that can be sustainable means that, that, that the response in a pandemic isn’t going to be what you think. Absolute disaster. And that was it.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content