This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you are interested, you can see my valuations from 2014 , 2016 and 2017. The automobile business has been in trouble for quite a while, struggling with anemic revenue growth in the aggregate, and abysmal profit margins, with even the very best in the group struggling to earn returns that match, let alone beat, their costs of capital.

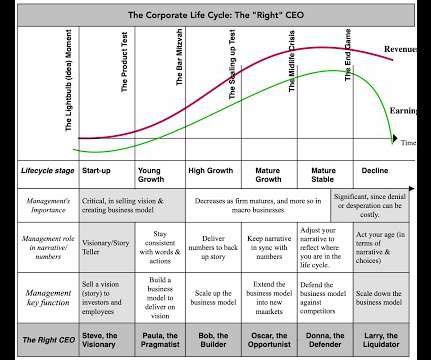

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

However, a poorly executed deal can cause financial losses, employee dissatisfaction, and even the downfall of a company. Valuation: How to Determine the Right Price A major part of analysing an M&A deal is figuring out how much the target company is worth. Several methods are used to value businesses, including: 1.

How Attention to Inventory Can Make or Break Manufacturers A major factor in determining the success of a manufacturer is how well it manages its inventory. When manufacturers have too little inventory, they can’t fully meet customer demands and lose out on revenue as a result. A benchmark exercise can also provide insight here.

Silvergate Capital — Shares of the crypto-focused bank fell 2.6%, adding to its 42% loss from the previous day. JPMorgan downgraded SI to neutral from overweight, citing Silvergate’s worse-than-expected deposit outflows and called into question the company’s long-term profitability. Greenbrier Companies — Shares fell 17.9%

Operating Performance/Profitability Narrative : While it is easy to attribute rising stock prices entirely to mood and momentum, the truth is that momentum has its roots in truth. I agree, but I remain a believer that intrinsic valuation is the only tool that you have for assessing whether g.

As has been the case for the past several quarters, the prevailing characteristic of the economy is one of bifurcation, with interest rate-sensitive sectors remaining in a recession (as evidenced by the manufacturing sector's 16-month-long contraction), while the services sector (which accounts for nearly 80% of U.S. GDP) continues to expand.

While it is just one quarter, there are clear signs of more slowing to come, as scaling will continue to push revenue growth down, the unit economics will be pressured as chip manufacturers (TSMC) push for a larger slice and operating margins will decrease, as competition increases.

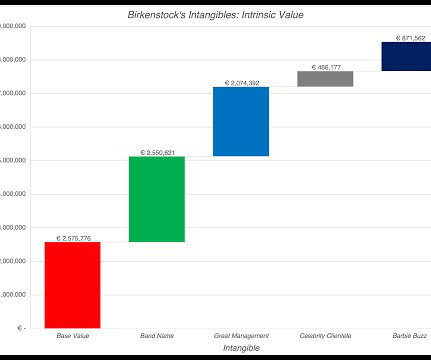

The Value of Intangible Assets Accounting has historically done a poor job dealing with intangible assets, and as the economy has transitioned away from a manufacturing-dominated twentieth century to the technology and services focused economy of the twenty first century, that failure has become more apparent.

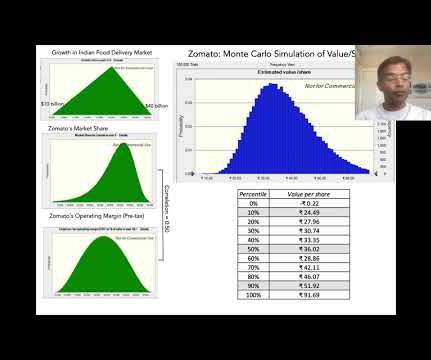

The primary attraction of the company, to investors, comes not from its current standing (modest revenues and big losses), but from its positioning to take advantage of the potential growth in the Indian food delivery market.

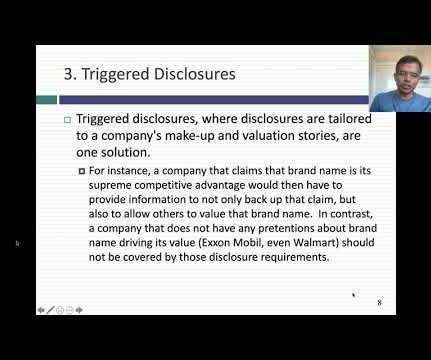

It extends into materiality, by reframing that concept in terms of value, rather than profits, and connecting it to disclosure, with disclosure requirements increasing proportionately with the value effect. One size (does not) fit all!

While M&A value dropped dramatically in 2022, a loss of 36% in deal value, Bain’s report confirms that deal activity continues to be a central corporate strategy for growth and profitability. Five M&A themes to watch According to the report, Bain has identified five M&A themes to watch this year.

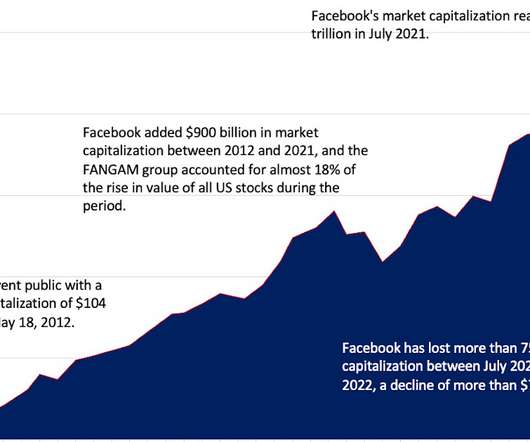

In the next post, I will use Facebook’s most recent earnings surprise to talk about inconsistencies in how accountants categorize corporate spending, and why these inconsistencies can skew investors perceptions of corporate profitability and financial health. billion in the third quarter of 2022. .

Manufacturing shows promising signs of recovery while nearshoring and friendshoring in new markets are becoming stronger trends. Greenfield project announcements dipped 6% in number but grew by 6% in value, driven in part by more encouraging numbers in the manufacturing sector. At an estimated $1.37

In the next post, I will use Facebook's most recent earnings surprise to talk about inconsistencies in how accountants categorize corporate spending, and why these inconsistencies can skew investors perceptions of corporate profitability and financial health. billion in the third quarter of 2022.

billion valuation and shares trading at $14-16 a share. At its post-IPO valuation and share price, Etsy was roughly 52 times its adjusted earnings. A pretty impressive feat, considering at the time of its IPO Etsy wasn’t actually profitable yet. A little over a year ago, Etsy IPOed, mostly to a round of applause.

We hope that we can invest behind and see stability so that there won’t be a loss of capital 00:28:00 [Speaker Changed] And, and above average GDP 00:28:02 [Speaker Changed] Growth. How, how are the higher rates affecting valuations amongst private companies? The auditors look at those valuations.

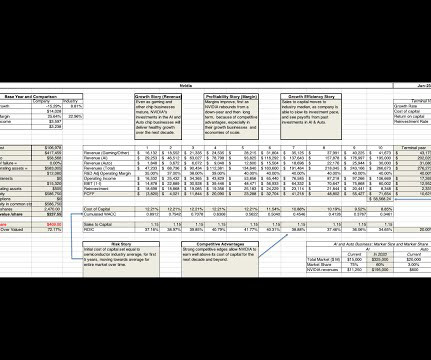

In the last four decades, computer chips have become part of almost everything we use, from appliances to automobiles, and the companies that manufacture these chips have seen their fortunes rise, and sometimes be put at risk, as technology shifts. Sustained Profitability, with Cycles! From High Growth to Maturity!

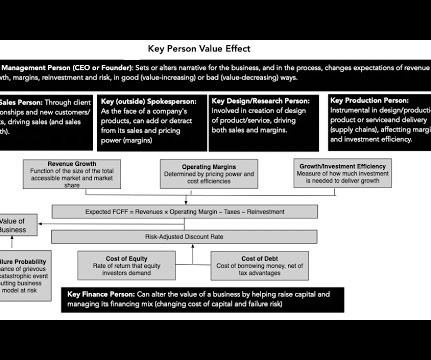

Of course, and with small businesses, especially those built around personal services (a doctor or plumber’s practice), it is part of the valuation process, where the key person is valued or at least priced and incorporated into valuation. Who is a key person?

And I found that subsegment really interesting because we did studies on kind of decision making biases, human biases like loss aversion and other biases that impact otherwise what should be rational decisions and make them less than rational. That is not being reflected in valuations from a top down standpoint. Absolutely.

The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961. MIAN: Valuations are ebb and flow. Manufacturing seems to be bottoming with ISM where it is right now.

And I think what I’m trying to imply is there’s a lot of informational value that’s already held within the valuations where these equities are trading that you can calculate, you know, a sense of the implied market probability of success for an opportunity for a company. There, 00:10:35 [Speaker Changed] There is.

And so, so we sort of felt pretty stupid for a while because we did a lot of losing trades in 2006 that were the, you know, that obviously didn’t come to fruition until the actual people could see the losses. So in mortgages, the borrower can stop paying maybe a year to two years before the lenders actually book a loss.

Note that the rise has not been all happenstance, and China deserves credit for taking advantage of the opportunities offered by globalization, making itself first the hub for global manufacturing and then using its increasing wealth to build its infrastructure and institutions.

Lately, though, they’re probably tossing and turning over the difficulties with raising capital coupled with the simultaneous descent of their venture’s valuations. And whether, if one and two come true, there’s a business model underneath all of it to profit from. ARE WE SOLVING THE RIGHT PROBLEMS FOR THE RIGHT PEOPLE?

Now you have to assume some losses. Barry Ritholtz : And these bonds are still profitable Jeffrey Sherman : And they don’t break, like they, they don’t, they don’t, they don’t lose money, especially at 50 cents on dollar. And you know, it’s the same thing when valuation gets outta control too.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content