This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The rattled corporation faces a rocky road through a wide-ranging restructuring, but some analysts see a more competitive company emerging. The decision, which was intended to help Anglo focus on its restructuring, swung the company from a net profit of $1.26 The restructuring itself is a complicated affair.

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

These companies are typically acquired through leveraged buyouts, growth investments, or other private equity strategies to enhance their value over time. Depending on the investment strategy, a PortCo may focus on expansion, restructuring, operational improvements, or preparing for an eventual sale or IPO.

Choosing transaction services can be invaluable for businesses navigating complex financial events, whether they involve acquisitions, mergers, divestitures, or restructuring. The team helps clients understand each deal’s potential returns and risks by providing accurate valuations and financial models.

I am not an accountant, but I do rely on accounting statements for the raw data that I use in corporate finance and valuation. In addition, accounting decisions to write off an asset or take restructuring charges will make the calculation of invested capital more difficult.

Macro Investment Market Challenges a Headwind for Private Equity Valuations Private Equity Sponsors are facing their most challenging valuation market since the great recession of 2008-09. Heightened inflation and interest rates will continue to be valuation headwinds.

To get there, they’re leveraging their respective strengths and forging partnerships to create new and innovative payment solutions that can move money across borders at any minute of the day with unprecedented speed. Big banks, like Citi, are jockeying to be their clients’ single “port of call” when it comes to transacting.

The growing variety and complexity of tasks within the finance function has resulted in the creation of a discipline that is supposed to become a bridge between the finance and business to support decision-making process by leveraging data and technology. This relates to FP&A which stands for financial planning and analysis.

Despite dwindling deal numbers, lucrative M&A opportunities continue to be available for those with the appetite and eye for lower valuations. They become transformational by leveraging new technology, processes or operating models from one business into the combined business. billion, according to Dealogic.

Choosing transaction services can be invaluable for businesses navigating complex financial events, whether they involve acquisitions, mergers, divestitures, or restructuring. The team helps clients understand each deal’s potential returns and risks by providing accurate valuations and financial models.

Choosing transaction services can be invaluable for businesses navigating complex financial events, whether they involve acquisitions, mergers, divestitures, or restructuring. The team helps clients understand each deal’s potential returns and risks by providing accurate valuations and financial models.

For companies with leases set to expire within the next two years, lease restructuring emerges as a prudent financial strategy. Quite simply, the name of the game for Landlords in this market is to retain your tenant roster and tenants can leverage this for an inexpensive deal. In 2021, the firm had revenue of $9.4

a share, a price that would decrease Uber’s $60 billion valuation by 30 percent. But, facing widening losses, Uber may prefer to take the haircut (and the corporate restructuring that goes with it) as it tries to get back on track for 2018. billion in funding. Initial payments skills will be tied to donations, restaurants and events.

Loans were primarily issued to SMB merchants that sell on the site, and bank partnerships were leveraged in some foreign markets. In Amazon’s case, the value of logistics is about $1 trillion, which is the valuation the company reached again this week, after the firm’s results and investments managed to impress investors.

For companies with leases set to expire within the next two years, lease restructuring emerges as a prudent financial strategy. Quite simply, the name of the game for Landlords in this market is to retain your tenant roster and tenants can leverage this for an inexpensive deal. In 2021, the firm had revenue of $9.4

You do the math and you’re like, “Okay, well, an advisor can handle about 100 clients, an associate advisor can help with some of those clients, you can leverage maybe an associate advisor with a couple of advisors, but there’s a capacity limit for each of the roles.” Is it at 1.5%? Cean: Yeah.

But, but I think if I was to go back through my career, that moment in time, you know, when there is this big wave coming, because it was the start of the high yield market, the leverage loan market grew dramatically, you know, from 200 billion in the mid nineties to $5 trillion today, high yield and leverage loans.

What happened over the last year and a half or so is rates went up and valuations went down. How do you institutionalize data management and, and how do you leverage the idea of, hey, we know a lot about this, here’s how we monetize it. 00:24:03 [Speaker Changed] So, so let’s talk about that. What is your approach to data?

The exposure you get in investment banking, I was a leveraged finance banker by background. And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from asset valuation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium.

And I think a lot of investors and, and lenders and really lost their way and agreed to terms and conditions that in under today’s market environment would not be acceptable levels of leverage that would not work. And if they don’t, we’re happy to own them at the valuation that we are creating that company act.

Default rates are near zero now, fault rates are, are kind of skewed a bit because you, you do have perhaps in high yield, if you look at, you know, with these liability management exercises and other restructurings outta court, it doesn’t default. But I, I think this extreme leverage is not as prevalent as it once was.

And we’d sort of turn that into a valuation business. MILLER: Well actually I thought, leading up to the great financial crisis, I thought to myself, we’re going to be out of business within a couple of years because nobody wanted an independent valuation. What are the, you know, I’d literally have it in my handheld.

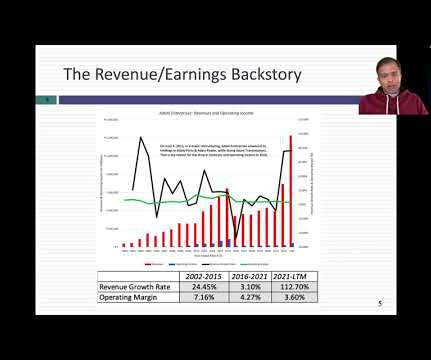

Download data Again, the steep drop off in invested capital that you see in 2015 is just a reflection of the restructuring of the company that year, as the invested capital in Adani Ports and Power was removed from the mix.

In fact, the infrastructure business is full of companies that borrow heavily, with little or no earnings buffer, and I am not sure that many of them will withstand the Hindenburg test for over leverage.

So, I graduated from business school in 1987 and went to GE Capital for two years, financing leveraged buyouts. I mean, you know, I probably shouldn’t have been doing it because I had been a journalist covering public schools and knew nothing about leveraged buyouts. COHAN: — and they’re restructuring.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content