This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Insurers have reported that there is still a huge amount of work to complete in order to successfully deliver IFRS 17 ahead of the 2023 deadline, said WTW recently. According to WTW’s latest survey, entitled ‘IFRS 17: Will we make it?’, insurers report material progress has been made since WTW’s previous IFRS 17 poll in 2021.

However, with a good counterparty risk the return is hardly better, and even often, still negative with, as a bonus on top, an intermediate volatility for those who report in IFRS (because of quarterly mark-to-market valuations). This interim volatility arises even if they keep the bonds until their redemption.

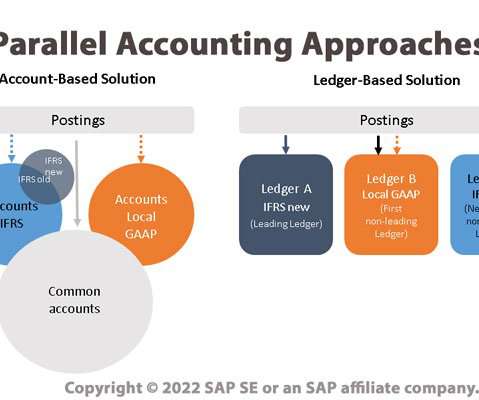

For example, a company with branches doing business in the United States and the European Union will need to comply with both GAAP and IFRS accounting principles. The account-based approach uses account logic identifiers to assign accounting principles, such as using unique prefixes to determine which accounts use IFRS vs GAAP principles.

The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies.

The research “How to improve IFRS for intangible assets? Boost company valuation : Properly capitalizing intangible assets can increase equity, improve financial ratios, and raise the company’s overall market valuation. A milestone approach” was authored by Shefei Ma and Weiguo Zhang in 2023.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. IFRS and GAAP now treat as leases as debt, but that is still not the case in many other markets that are not covered by either standard). The numbers yield interesting insights. .

Valuations are a classic example of hole-filled financial reporting. History is riddled with companies that went public based on inflated valuations and false narratives. WeWork expected to offer shares to the public at a $47 billion valuation. If you want to build shareholder trust, start with the data.

Goodwill = P− (A − L ) where: P=Purchase price A=Fair market value of assets L=Fair market value of liabilities T-Mobile/Sprint Merger: A Real Life Goodwill Valuation In 2018, T-Mobile acquired Sprint to the tune of $35.85 At the time of the acquisition, the fair market value for the Sprint corporation was determined to be $78.34

5 Other sustainability reporting initiatives in development include those of the International Sustainability Standards Board (ISSB), developed by the International Financial Reporting Standards (IFRS) Foundation.

Using the words of IFRS (1.7), ‘ Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity ’.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. IFRS and GAAP now treat as leases as debt, but that is still not the case in many other markets that are not covered by either standard). The numbers yield interesting insights.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. It is very likely that these rules of thumb were developed from data and observation, but at a different point in time.

IFRS, US GAAP). Valuation and Reporting: Properly recognizing and valuing intangible assets impacts financial statements, investor relations, and the company’s market valuation. Is there a significant difference between US GAAP and IFRS , or are we just being a bit too conservative here in South Africa?

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content