This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

IFRS 9 is changing hedge accounting forever. Companies in the European Union have only begun to kick off their IFRS 9 initiatives since the European Commission endorsed the standard in November 2016. IFRS 9 Advantages in a Nutshell. IFRS 9 enables hedgers to treat “costs of hedging” as a separate component of equity.

IFRS 16, published by the International Accounting Standards Board (IABS), came into effect on January 1, 2019. In an effort to boost transparency, IFRS 16 eliminates the distinction between finance leases, which were previously capitalized on corporate balance sheets, and operating leases, which were not.

Written by Staff Writer There was outrage when National Treasury abruptly announced last month that it was exempting Eskom from reporting irregular, fruitless and wasteful expenditure in its financial statements. However, seasoned finance professional, Thabo Maake believes that National Treasury was correct in its decision.

Treasury management is “anticipation”. This explains why the treasury manager, “the custodian of cash”, has become a centre of attention and why Cash Flow Forecasts (CFF) have become so essential. not all cash can be reported to central treasury. Often, we heard “ cash is king”. Managing cash is easier than forecasting cash.

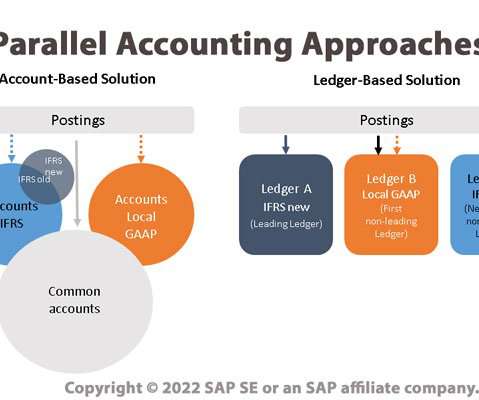

For example, a company with branches doing business in the United States and the European Union will need to comply with both GAAP and IFRS accounting principles. The account-based approach uses account logic identifiers to assign accounting principles, such as using unique prefixes to determine which accounts use IFRS vs GAAP principles.

Many companies hedge on a budgetary basis and qualify hedges of future cash flows by applying the so-called "cash-flow hedge" method under IFRS 9 (ex-IAS 39). Any hiccup may require readjustment of the accounting of the transactions, as required by IFRS 9. "Cash-Flow Hedge (CFH) Method applied.

The other is the International Accounting Standards Board (IASB), whose rules for financial reporting are known as International Financial Reporting Standards (IFRS). IFRS S1 requires companies to communicate the sustainability risks and opportunities they face over the short, medium, and long term.

With our years of experience in helping clients achieve compliance with new mandates such as revenue recognition (ASC 606 and IFRS 15), lease accounting (ASC 842 and IFRS 16) and optimizing Office of the CFO processes for treasury, cash flow, risk management and more, Bramasol has long advocated a comprehensive, integrated approach - as exemplified (..)

However, with a good counterparty risk the return is hardly better, and even often, still negative with, as a bonus on top, an intermediate volatility for those who report in IFRS (because of quarterly mark-to-market valuations). This interim volatility arises even if they keep the bonds until their redemption.

Operational Accounting is concerned primarily with the processes for areas like sales, revenue, treasury, cash flow, margins, KPIs, etc. This has enabled clients to smoothly comply with ASC 842 and IFRS 16. However, treasury functions are not always unified and integrated.

For leasing, this means International Accounting Standards Board’s (IASB’s) IFRS 16 and US GAAP Financial Accounting Standards Board’s (FASB’s) ASC 842. For revenue recognition, they also must comply with ASC 606 and IFRS 15.

The Need for Specialized Technology Solutions To address this pressing need, treasury teams are relying on CS Lucas Treasury Management System’s dedicated syndicated loan modules. Let’s explore some of the key capabilities of CS Lucas: 1. Management and auditors gain on-demand reporting.

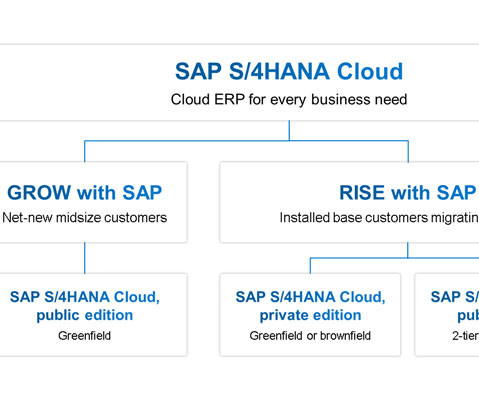

Leveraging RISE with SAP to Comply, Optimize, and Transform your Business With Bramasol's years of experience in helping clients achieve compliance with new mandates such as revenue recognition (ASC 606 and IFRS 15), lease accounting (ASC 842 and IFRS 16) and optimizing Office of the CFO processes for Order-to-Cash-to-Compliance, treasury, cash flow, (..)

Bringing an Expanded RevRec "Compliance Mindset" into New Business Models: Even though subscription-based, Digital Solutions Economy (DSE) business models are radically changing many industries, RevRec compliance under ASC 606 and IFRS 15 is still required.

Accounting knowledge (IFRS and taxation). Treasury and investment management. Information quality and control rationalisation are top-of-mind issues for the Steward. Competencies include: Working knowledge of risk management, budget, and forecasting tools. Investment and credit risk knowledge. Competencies include: Staff planning.

Bringing an Expanded RevRec "Compliance Mindset" into New Business Models: Even though subscription-based, Digital Solutions Economy (DSE) business models are radically changing many industries, RevRec compliance under ASC 606 and IFRS 15 is still required.

Treasury and cash management. These systems provide built-in support for complexities such as currency translation, intercompany eliminations, and reporting under multiple accounting guidelines, such as US GAAP or IFRS. Here are some of the key processes supported by an ERP system: Purchasing. Accounts payable. Fixed asset management.

So a lot of invoices, accounts payable, accounts receivable, cash flow management, treasury working with procurements, so really the back office function at Anheuser-Busch, really pushing, making sure that everything works efficiently. So a lot of it was leading back office finance for the company.

For instance, I have always computed the present value of lease commitments in future years and treated that value as debt, a practice that IFRS and GAAP have adopted in 2019, but that computation requires explicit disclosures of lease commitments in future years.

With our core focus on financial applications such as order-to-cash, revenue recognition, subscription-billing, leasing, treasury and other solutions, Bramasol has significant experience in virtually all aspects of S/4HANA migration that involve the Office of the CFO.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content