This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For example, while South African companies follow International Financial Reporting Standards (IFRS), the US requires compliance with its Generally Accepted Accounting Principles (GAAP). IFRS is principles-based and allows for some judgment in financial reporting, while GAAP is more rigid, rules-based, and less forgiving.

Compliance with standards like ASC 606 and IFRS 15 is still crucial, but the focus has shifted to optimising operations for growth. Inconsistent application of IFRS 15 and ASC 606 can lead to significant risks, including audit adjustments, compliance penalties, and investor mistrust. Spreadsheets cause manual work and time delays.

Automation helps organizations comply with IFRS, GRAP, and local tax regulations by ensuring all reporting follows the latest legal frameworks. To mitigate this, CFOs can start small; automating reconciliation and reporting workflows first before scaling. More focus on strategic decision-making instead of crunching numbers.

The Financial Reporting Council (FRC) calls for IFRS 17 disclosures improvements in its recently published IFRS 17 'Insurance Contracts' thematic review. The IFRS 17 disclosures improvements that FR C expects include the following. The post IFRS 17 disclosures improvements needed: FRC appeared first on FutureCFO.

Since the release of new lease accounting standards ASC 842 and IFRS 16 in 2018, companies have taken a variety of approaches to comply, but many are now aiming to optimize their lease accounting processes for efficiency and long-term manageability.

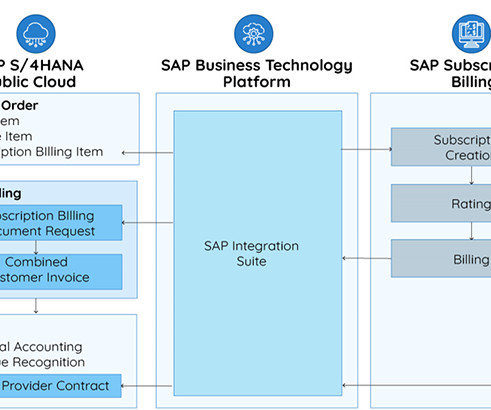

Over the past eight years, many episodes in this blog series have focused on revenue recognition and how SAP solutions such as Revenue Accounting and Reporting (RAR) have provided a robust foundation for compliance with ASC 606 and IFRS 15.

The move to embrace automation, said Krumwiede, represents a “slow evolution,” with inefficiencies still extant as there must be communication between departments and data must be compiled and formatted in the practice of reconciliation. The optimization of the accounting process, he said, is difficult at times with limited staff.

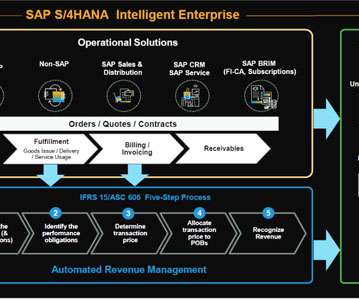

Within the Five-Step model, Step 4 of ASC 606 and IFRS 15 requires an allocation of the total consideration in a contract, which your company is entitled to collect for each distinct performance obligation. Manual Processes: Reliance on manual data entry and spreadsheet-based reconciliations can be time-consuming and error-prone.

Moreover, your system must be designed to comply with relevant financial regulations and standards, such as the International Financial Reporting Standards (IFRS), Generally Accepted Accounting Practice (GAAP), and local tax laws. Regular updates to the system to reflect changes in these regulations are also crucial.

It also helps finance teams deliver financial results, create informative financial and management reports, and provide the chief financial officer (CFO) with an enterprise view of key financial ratios and metrics.

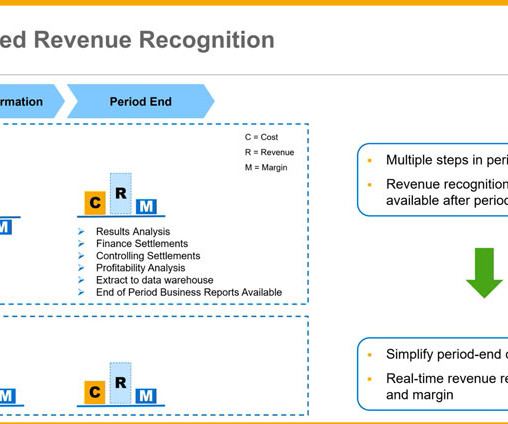

Although the initial compliance phase for ASC 606 and IFRS 15 revenue recognition mandates is in the rear-view mirror for most companies, it's important to also keep a focus on the road ahead because optimization of overall RevRec processes across the enterprise will be key to ongoing success.

Intercompany reconciliations were a nightmare, with many phone calls to the foreign subs. Consolidating the financial results following US GAAP or IFRS guidelines, including these steps: Performing currency conversions. Managing complex intercompany reconciliations. I think we used Lotus 123.) Multiple reporting hierarchies.

This has enabled clients to smoothly comply with ASC 842 and IFRS 16. As too many CFOs have learned the hard way, trying to close the books without accurate data from underlying operations, or resorting to offline manual spreadsheets for reconciliation is a recipe for major problems.

These results then require consolidation following US GAAP or IFRS guidelines. If the business operates in different geographies there will be the additional complexity of multiple currency conversions, intercompany reconciliations and accurate accounting of minority interests. Attend to Reconciliations Early.

There are ongoing efforts to establish International Financial Reporting Standards (IFRS) for nonprofits, which, if successful, could result in greater consistency and comparability of financial information across countries.

A tech startup might start with basic financial software, but as it scales and perhaps looks for external investment, the CFO will need systems that support more detailed and sophisticated financial reporting, such as investor reporting and compliance with IFRS standards. This saves time and ensures higher accuracy in reporting.

Not being compliant with US GAAP or IFRS. Streamline adjustments and intercompany reconciliations by 50 – 80%. Challenges in consolidating multiple spreadsheets and correcting errors. Limited reporting and analysis capabilities, and too much manual effort. Lack of controls and audit trails. Lack of security.

The matching principle is supported inherently and therefore no periodic batch jobs are needed for reconciliation. Improved Compliance - Ensures compliance with ASC 606, IFRS 15, and other relevant accounting standards through a robust set of predefined rules and configurable options.

Intercompany reconciliations. US GAAP, Canadian GAAP, IFRS, etc.). In an organization that’s operating with multiple divisions, in multiple countries and regions, the process can become complex. This includes dealing with the following issues: Currency translation. Non-controlling interest and minority ownership.

Compliance: Adherence to accounting standards and regulations, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). Bank Reconciliation: Xero's bank reconciliation features help ensure accurate financial data, which is crucial for reliable reporting.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content