This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the major IFRS 17 challenges is that it’s disrupting business as usual for insurers. According to a WTW IRS 17 survey, there are major post-implementation challenges that insurers still need to overcome after reporting their half-year 2023 results under IFRS 17 for the first time.

Insurers have reported that there is still a huge amount of work to complete in order to successfully deliver IFRS 17 ahead of the 2023 deadline, said WTW recently. According to WTW’s latest survey, entitled ‘IFRS 17: Will we make it?’, insurers report material progress has been made since WTW’s previous IFRS 17 poll in 2021.

IFRS 16, published by the International Accounting Standards Board (IABS), came into effect on January 1, 2019. In an effort to boost transparency, IFRS 16 eliminates the distinction between finance leases, which were previously capitalized on corporate balance sheets, and operating leases, which were not.

The total IFRS cost faced by the global insurance sector to implement the standard is estimated to hit the range of US$15 billion - US$20 billion, said Willis Towers Watson recently. Estimated IFRS costs vary significantly by insurer size, according to a Willis Towers Watson study which polled 312 insurers from 50 countries.

Todays financial systems integrate with Enterprise Resource Planning (ERP) software, cloud computing, and artificial intelligence (AI) to provide instant access to up-to-date financial information. This shift allows businesses to move from reactive decision-making to proactive planning.

Follow standard accounting rules In most industries, this means using IFRS (International Financial Reporting Standards) or IFRS for SME (International Financial Reporting Standard for Small and Medium-sized Entities) to prepare financial statements. IT teams manage the software systems used to collect and store financial data.

Many companies hedge on a budgetary basis and qualify hedges of future cash flows by applying the so-called "cash-flow hedge" method under IFRS 9 (ex-IAS 39). Thus, when circumstances required it, companies had to shift the timing of transactions initially planned for a specific date.

Brian O’Donovan from KPMG International Standards Group provides an update on plans to amend IFRS 16 Leases in response to the COVID-19 coronavirus pandemic. The post What changes are being made to IFRS 16 because of COVID-19? appeared first on FutureCFO.

Although over half (62%) of companies studied have included sections on nature and biodiversity in their sustainability report, only 7% disclosed that they currently refer to the TNFD framework for their nature and biodiversity reporting, while 11% plan to align with it in the future.

Financial governance allows your organization to meet compliance requirements, such as IFRS and GAAP updates, by having the right financial controls in place. All the data you need is captured in real-time for improved financial forecasting, reporting, and planning accuracy.

From a global perspective, the International Sustainability Standards Board (ISSB), which was established by the IFRS in November 2021 at COP26 in Glasgow, has issued its first two standards. IFRS S1 requires companies to communicate the sustainability risks and opportunities they face over the short, medium, and long term.

Financial planning and analysis (FP&A) is important in automating all of the manual tasks in the finance department and giving everyone greater insights into the data. FP&A not only supports business and financial decision-making but also provides management with insights into the organization’s strategic plans and investments.

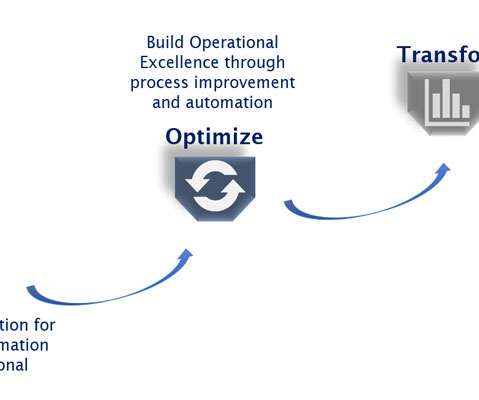

Of course, one of the things that we've all learned over the years is that there is rarely a perfect one-size-fits-all solution for everyone, so we encourage clients to consider all the available options, especially when planning a major business transformation program. Overview of Comply, Optimize, Transform.

Ensuring Data Integration In today’s interconnected world, your FIS must seamlessly integrate with other business systems, such as Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), and Human Resources (HR) systems. Planning for Scalability Finally, it’s crucial to design your FIS with the future in mind.

For leasing, this means International Accounting Standards Board’s (IASB’s) IFRS 16 and US GAAP Financial Accounting Standards Board’s (FASB’s) ASC 842. For revenue recognition, they also must comply with ASC 606 and IFRS 15.

Market dynamics and uncertainties are making revenues less predicable for MedTech manufacturers, thereby impairing forecasting and planning processes. The shift from CAPX purchase models to subscription based offerings requires medical device manufacturers to adapt their revenue recognition and reporting systems to assure compliance.

But Robert Kugel , SVP and Research Director at Ventana Research, recently published an article highlighting the impact the new guidelines can have on budgeting and planning. However, the revenue recognition guidance offered under US GAAP vs. IFRS has differed and was in need of improvement. Background – What’s Changing and When?

Within the Five-Step model, Step 4 of ASC 606 and IFRS 15 requires an allocation of the total consideration in a contract, which your company is entitled to collect for each distinct performance obligation. Digital Transformation: Is there a way to map out an incremental plan for migrating our business to S/4HANA? What are the options?

ISSB preparedness The research looked at companies’ readiness for meeting the requirements for IFRS S2 Climate-related Disclosures. Yet the study shows that only 53% of the surveyed companies are providing disclosure against some kind of transition plan.

Are you wondering how best to make the business case to your company for investing in a cloud-based planning or reporting solution? Reducing Reliance on Spreadsheets for Budgeting, Planning, and Reporting. The key challenges in using spreadsheets and email for budgeting and planning: Too much manual work – the process takes too long.

AI driven automation is expected to extend to more complex tasks such as, audits, risk management, and financial planning and analysis. Fine-tuned AI models could assist with complex regulatory requirements, such as those from IFRS, FINRA, and the SEC. With a large and diverse enough data set (e.g.

Financial indices are all positive, we’ve just presented our business plans to our shareholders and we’re still portraying a positive business plan for next year. I leave the younger generation to worry about the technicalities in the IFRS books, in the tax books, that’s what you have the specialist skills in the business for.

Information about climate-related targets and goals, and transition plan, if any. ISSB was established by the IFRS Foundation in response to the Glasgow COP 26 conference in November 2021. Certain climate-related financial statement metrics and related disclosures in a note to its audited financial statements; and ?

Unlike IFRS standards that are well-structured and finance practices that allow flexibility based on internal business needs, changing regulatory guidelines has caused ambiguity and anxiety due to the very fluid and subjective interpretations that can lead to material dollar spend for the company.”

This has enabled clients to smoothly comply with ASC 842 and IFRS 16. Financial Planning and Analysis (FP&A): In addition to capturing and reporting what has happened, CFOs and their staff also need tools for looking ahead to assure improved success in the future. That's where FP&A plays a key role.

Complex Reporting Standards: Adhering to both International Financial Reporting Standards (IFRS) and local regulations can complicate financial reporting. For SMEs, the IFRS for SMEs standard simplifies reporting but still requires thorough understanding and application.

Click on the link to download to discover in detail a list of the benefits that IBM Cognos Controller provide for finance teams: Data collection and validation Reconciliations Workflow and tasks to improve the close cycle Currency conversion Minority interest calculations Inter-company eliminations Group closing adjustments Management adjustments Allocations (..)

Bringing an Expanded RevRec "Compliance Mindset" into New Business Models: Even though subscription-based, Digital Solutions Economy (DSE) business models are radically changing many industries, RevRec compliance under ASC 606 and IFRS 15 is still required.

Held over two days, this year’s event focused on the expanding roles of CFOs in forecasting, planning, and strategic decision-making, highlighting the importance of technological advancements in driving business innovation. Pieter highlighted the importance of fostering collaboration and sharing best practices among CFOs globally.

As a small business owner or finance manager, it’s crucial to approach this process with a clear plan. An audit evaluates: Compliance with accounting standards (GAAP or IFRS.) Based on the audit findings, create an action plan to address any issues and refine your financial processes. What Do Financial Auditors Look For?

Strategic Measure: CFOs should focus on strong cash flow forecasting and planning for different scenarios. By creating different financial plans for various economic situations, CFOs can better prepare for and respond to potential problems.

Despite agreeing to climate commitments, about 56% of those surveyed in Southeast Asia do not disclose a transition plan to back these. Of those that do disclose plans (44%), the level of detail remains limited. Agriculture, however, falls behind, with 47% of those surveyed in that sector disclosing any form of transition plan.

Bringing an Expanded RevRec "Compliance Mindset" into New Business Models: Even though subscription-based, Digital Solutions Economy (DSE) business models are radically changing many industries, RevRec compliance under ASC 606 and IFRS 15 is still required.

Accounting knowledge (IFRS and taxation). Competencies include: Staff planning. Information quality and control rationalisation are top-of-mind issues for the Steward. Competencies include: Working knowledge of risk management, budget, and forecasting tools. Investment and credit risk knowledge. Project management. Corporate finance.

Better Insights : Provides deeper insights into revenue metrics and performance, supporting better decision-making and strategic planning. Upon the release of a service contract, revenue is calculated and posted according to the billing plan tied to the contract items. This PoC is then applied to the planned cost.

Consolidating the financial results following US GAAP or IFRS guidelines, including these steps: Performing currency conversions. The financial close and consolidation modules provided by cloud-based EPM providers, such as Planful , make the year-end close and reporting process much less painful. Enter cloud-based EPM software.

This is another key pillar of the leadership development for financial planning and analysis (FP&A) professionals. An FP&A leader should be able to integrate financial planning with strategic and operational planning in order to drive the overall business performance that will result in the financial success of the organization.

AI driven automation is expected to extend to more complex tasks such as, audits, risk management, and financial planning and analysis. Fine-tuned AI models could assist with complex regulatory requirements, such as those from IFRS, FINRA, and the SEC. With a large and diverse enough data set (e.g.

Our customers love to tell us how many inefficiencies they had in their reporting process before they started using the Planful Platform for financial reporting. Planful Reporting has even helped some of our customers reduce their reporting times by 90% ! That’s just one simple example. That’s huge, and it’s easily attainable. .

1 These pros and cons are enough to motivate the C-suite to expedite their ESG efforts, starting with determining the department responsible for ESG planning and reporting. Numerous associations, consultants, and analysts have promoted the idea of the finance function assuming the core responsibility for ESG planning, tracking, and reporting.

GAAP or International Financial Reporting Standards (IFRS). While these systems have historically been deployed in on-premises data centers, they are now available as Cloud Financial Planning and Analysis Solutions. . Consolidating the data following specific financial accounting rules and guidelines, such as U.S.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content