This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Role of IFRS in Simplifying Cross-Border Financial Reporting In todays interconnected world, businesses are no longer confined by borders. This is where International Financial Reporting Standards (IFRS) come into play. But what does it really mean to be IFRS-compliant? What is IFRS Compliance? Why is it important?

The next logical step might be to take your company to international markets by listing on a foreign stock exchange. IFRS is principles-based and allows for some judgment in financial reporting, while GAAP is more rigid, rules-based, and less forgiving. Under IFRS 16, virtually all leases go on the balance sheet as liabilities.

The new IFRS sustainability standards will impact businesses large and small, says Suresh Kana, trustee and deputy chair of the IFRS Foundation. Kana also notes that IFRS will work on industry-specific standards. “If So you could use these standards in the US or you could use them in [IFRS jurisdictions].”

Load shedding also contributes to market volatility “Our biggest challenge is the ongoing market volatility. Obviously, we know US markets are extremely strong, but it’s the uncertainty of the rand that’s the biggest challenge. However, as a modern CFO, you cannot only rely on your IFRS textbook or your technical abilities.

Navigating IFRS , Key Updates and Changes Introduction In today’s fast-paced financial world, staying up to date with the latest International Financial Reporting Standards (IFRS) is critical for CFOs. IFRS 16 Leases: Impact on Balance Sheets IFRS 16 has changed the way leases are recorded on balance sheets.

IFRS 16, published by the International Accounting Standards Board (IABS), came into effect on January 1, 2019. In an effort to boost transparency, IFRS 16 eliminates the distinction between finance leases, which were previously capitalized on corporate balance sheets, and operating leases, which were not.

The total IFRS cost faced by the global insurance sector to implement the standard is estimated to hit the range of US$15 billion - US$20 billion, said Willis Towers Watson recently. Estimated IFRS costs vary significantly by insurer size, according to a Willis Towers Watson study which polled 312 insurers from 50 countries.

Why Maake believes Treasury was right A core point of Maake’s argument is that State Owned Companies (SOCs) like Eskom are expected to not only adhere to IFRS and the Companies Act, but also the PFMA. All these elements are covered under IFRS. By the time you investigate, the report is already out in the market.”

That said, about 31% of the net profits of all publicly traded firms listed globally in 2021 were generated by financial service firms; that percent is lower in the US and higher in emerging markets. IFRS and GAAP now treat as leases as debt, but that is still not the case in many other markets that are not covered by either standard).

Listed companies (on the stock exchange) They must meet strict financial disclosure rules, often set by stock market regulators like the JSE (Johannesburg Stock Exchange). Retail and e-commerce Companies must follow tax and consumer protection laws, ensuring customers receive fair pricing and honest business practices.

The extremely high market volatility during the health crisis, one of the economic consequences of COVID, also forced many companies to review their hedging strategy. Many companies hedge on a budgetary basis and qualify hedges of future cash flows by applying the so-called "cash-flow hedge" method under IFRS 9 (ex-IAS 39).

Driven by sweeping changes such as digital transformation, globalization of markets, the subscription-based Digital Solutions Economy™ (DSE), carbon-accounting mandates, a rising emphasis on artificial intelligence, and other disruptive trends, the role of Chief Financial Officer (CFO) is undergoing radical transformation too.

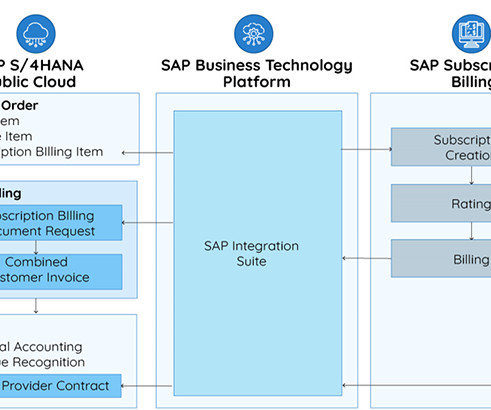

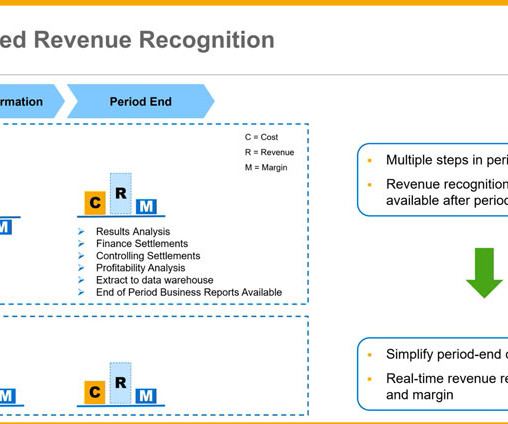

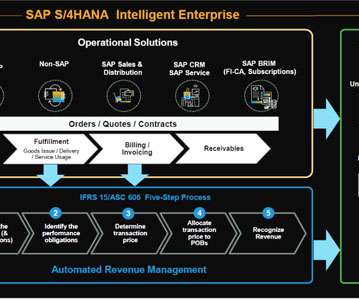

Compliance with ASC 606 / IFRS 15 requires separate cumbersome processes. To overcome these limitations, many market leading companies are leveraging SAP's Billing and Revenue Innovation Management (BRIM) solution to holistically innovate and scale recurring revenue-based order-to-cash processes. Complex allocations of revenue.

However, with a good counterparty risk the return is hardly better, and even often, still negative with, as a bonus on top, an intermediate volatility for those who report in IFRS (because of quarterly mark-to-market valuations). This interim volatility arises even if they keep the bonds until their redemption.

The ability to receive those quick business insights also helps you respond to rapidly changing market conditions, so you remain highly competitive in a very demanding business environment. GAAP, IFRS, and cash base side by side for better visibility. The benefits don’t end there. . Ability to implement user-access controls.

Meanwhile, the EC has extended the deadline to release its review of the effectiveness of the Interchange Fee Regulation (IFR), which came into effect in 2015. The issue at hand is the IFR’s focus on protecting individual cardholders, whereas corporations are the “consumer” in the case of the commercial card.

According to Allied Market Research, "The global medical equipment rental market was valued at $56.0 For leasing, this means International Accounting Standards Board’s (IASB’s) IFRS 16 and US GAAP Financial Accounting Standards Board’s (FASB’s) ASC 842. For revenue recognition, they also must comply with ASC 606 and IFRS 15.

The medical device market has traditionally evolved around a capital equipment acquisition model in which customers, such as hospitals, clinics or other providers, purchase or lease the equipment and separately purchase consumables and/or maintenance.

Within the Five-Step model, Step 4 of ASC 606 and IFRS 15 requires an allocation of the total consideration in a contract, which your company is entitled to collect for each distinct performance obligation. Standalone Selling Price: What is SSP, why is it needed, and how is it determined?

Autonomously driven vehicles emerging for both commercial and consumer markets. Some of the key challenges and disruptive trends in the transportation sector include: Supply chain inefficiencies exposed by the pandemic and shifts in consumer buying behavior. Public transportation systems need to improve accessibility and cost of ridership.

Hence, it is crucial to adopt established standards and frameworks such as the International Financial Reporting Standards (IFRS) Sustainability Disclosure Standards issued by the International Sustainability Standards Board (ISSB), the Greenhouse Gas Protocol and ISO 14064.

Integrated financial sustainability reporting is here In June 2023 the International Sustainability Standards Board (ISSB) issued its first two IFRS Sustainability Disclosure Standards, IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures.

When it comes to sustainability standards, the needs of mid-market businesses must be taken into account, said Grant Thornton International recently. Setting the bar too high is likely to affect the ability of the mid-market to comply, he said. “We

Also problematic for London will be continued access for the single labor market, since immigration concerns were central to the Brexit debate. To head off some of the worst outcomes, the BBA suggests government officials negotiate new market access arrangements in a bilateral agreement with the EU.

We know that construction has been a bit of a saturated market but hopefully there will be a turnaround once infrastructure spend starts again. I think the challenges that we have are really around the volatility that we’re dealing with in the markets, we’re dealing with ongoing volatility.

The South African market offers a range of solutions, from cloud-based platforms that offer flexibility and scalability to on-premises systems that provide greater control and customization. Choosing the Right Software and Technology Selecting the appropriate financial software is a critical decision.

Over the past eight years, many episodes in this blog series have focused on revenue recognition and how SAP solutions such as Revenue Accounting and Reporting (RAR) have provided a robust foundation for compliance with ASC 606 and IFRS 15. This provides the basis for real-time matching of revenue and cost.

Although the initial compliance phase for ASC 606 and IFRS 15 revenue recognition mandates is in the rear-view mirror for most companies, it's important to also keep a focus on the road ahead because optimization of overall RevRec processes across the enterprise will be key to ongoing success.

Today, not being of " investment grade " quality is an enormous handicap in the bank lending market. The bond market would appear to compensate for this lack, as do stock-market issues, although these are on the decline or still at an exceptionally low level, after a financial earthquake unique in the history of modern finance.

Public companies must prepare for investor, shareholder, and market demands in compliance with relevant reporting frameworks – as applicable to each Company’s jurisdiction and fact pattern, including: SEC’s Climate Disclosure Rules European Sustainability Reporting Standards (ESRS) IFRS Sustainability Reporting Standards Task Force on Climate-Related (..)

“The Committee believes that the accounting model for cryptocurrency that has an active market, and is held by an entity as a medium of exchange or investment, should be generally aligned with that for a foreign currency.” GAAP,” the letter stated.

The research “How to improve IFRS for intangible assets? The study found that many firms in China’s emerging high-tech markets are forced to expense their R&D entirely, which can stunt their growth and distort financial reports. A milestone approach” was authored by Shefei Ma and Weiguo Zhang in 2023.

ISSB preparedness The research looked at companies’ readiness for meeting the requirements for IFRS S2 Climate-related Disclosures. As such, it should be assessed in the context of the company’s value chain and wider market dynamics. The post The future of sustainability reporting appeared first on FutureCFO.

Financial Sector Conduct Authority (FSCA): The FSCA regulates financial institutions, including banks, insurers, and asset managers, focusing on market conduct to ensure fair treatment of customers. The FSCA plays a crucial role in maintaining market integrity and consumer confidence in the financial sector.

“As the business's nerve centre, the controller connects with external stakeholders, including the parent company, banks, and government bodies, having exposure to operations, marketing, consumer insights, and supply chain.”

Public companies must prepare for investor, shareholder, and market demands in compliance with relevant reporting frameworks – as applicable to each Company’s jurisdiction and fact pattern, including: SEC’s Climate Disclosure Rules European Sustainability Reporting Standards (ESRS) IFRS Sustainability Reporting Standards Task Force on Climate-Related (..)

What’s interesting is that the court concluded that a lawful level of credit interchange for the UK market would be over 65% higher than the 30bps rate cap imposed in the 2015 Interchange Fee Regulation (“IFR”). At the same time, the court criticized and rejected the ‘merchant indifference test,’ the cornerstone for the IFR.

Lim Lay Wah "According to Climate Bonds Initiative, the Southeast Asia sustainable finance market in 2022 raised US$36 billion, almost double the amount in 2020." "We We are seeing the same trend at UOB.

However, the revenue recognition guidance offered under US GAAP vs. IFRS has differed and was in need of improvement. In May of 2014 , the two bodies issued their converged guidance under ASC 606 and IFRS 15. Improves comparability of revenue recognition practices across entities, industries, jurisdictions, and capital markets.

A few days ago, I valued Instacart ahead of its initial public offering , and noted that the reception that the stock gets will be a good barometer of where risk capital stands in the market, right now. There is another measure that you can use to see the futility, at least so far, of accounting attempts to value intangibles.

Such technical breaches may trigger cross default clauses and jeopardize corporate reputations with credit markets more broadly. Accounting Compliance Specialist tools guarantee lending treatments comply fully with evolving IFRS accounting standards. Management and auditors gain on-demand reporting.

Accounting knowledge (IFRS and taxation). The Strategist provides a financial perspective on innovation and profitable growth, leverages this perspective to improve risk-awareness, strategic decision-making, and performance management integration, and translates the expectations of the capital markets into internal business imperatives.

That said, about 31% of the net profits of all publicly traded firms listed globally in 2021 were generated by financial service firms; that percent is lower in the US and higher in emerging markets. IFRS and GAAP now treat as leases as debt, but that is still not the case in many other markets that are not covered by either standard).

Other markets covered in the study fared better in the quality of disclosure, with Malaysia scoring 43% and Singapore at 41%. Furthermore, 71% of companies in Southeast Asia were found to have failed to perform scenario analysis in the context of the company’s value chain and wider market dynamics.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content