This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I spend most of my time in the far less rarefied air of corporate finance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

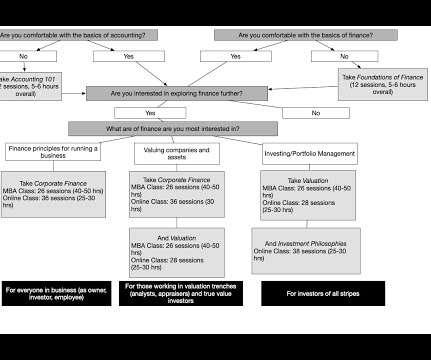

I know that this classification is at odds with the industry classifications based upon SIC or NAICS codes, but it works well enough for me, at least in the context of corporate finance and valuation. Since I teach corporate finance and valuation, I find it useful to break down the data that I report based upon these groupings.

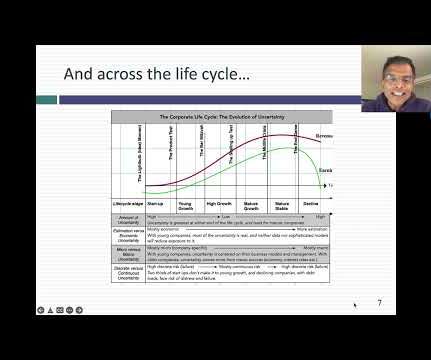

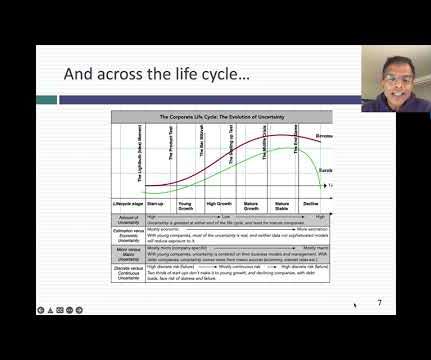

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

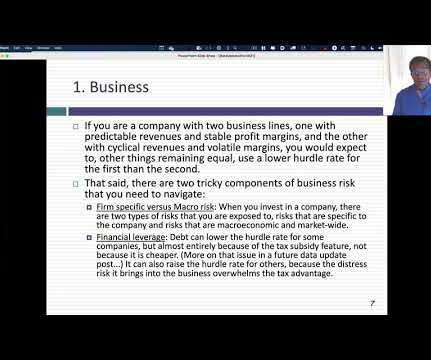

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporate finance, this takes the form of a hurdlerate , a minimum acceptable return on an investment, for it to be funded.

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporate finance, this takes the form of a hurdlerate , a minimum acceptable return on an investment, for it to be funded.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. By the same token, it is impossible to use a pricing metric (PE or EV to EBITDA), without a sense of the cross sectional distribution of that metric at the time.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. If anything, as rates have decreased over the last decade, and costs of capital for companies hit historic lows, companies are finding it more difficult to earn returns that exceed their costs of capital. .

That year, I computed these industry-level statistics for five variables that I found myself using repeatedly in my valuations, and once I had them, I could not think of a good reason to keep them secret. Valuation Pricing Growth & Reinvestment Profitability Risk Multiple s 1. Insider, CEO & Institutional holdings 2.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. I will use this data to draw three broad conclusions: Low HurdleRate ? The proverbial bottom line for success in business is the capacity to deliver profits, at least in the long term.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post. and the reverse will occur, when risk-free rates drop.

Thus, you and I can disagree about whether beta is a good measure of risk, but not on the principle that no matter what definition of risk you ultimately choose, riskier investments need higher hurdles than safer investments. pm (New York time) Valuation (MBA): Mondays & Wednesdays, 2.00 Don't get me wrong!

It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. Data Update 4 for 2021: The HurdleRate Question. Data Update 2 for 2021: The Price of Risk!

In the picture below, I make my best judgments on each of these dimensions, using consensus estimates of earnings in 2021 and 2022 to get started, but then slowing growth in earnings to match the growth rate in the economy, which I approximate with the risk free rate. Data Update 4 for 2021: The HurdleRate Question.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. All these factors have an interest rate embedded in them.

One, when people have asked me to compare and contrast today versus 2007, 2008, what you hear from a lot of people is, yes, there’s some fairly heady valuations. But I don’t think this is a wholesale shift, we’re in a higher rate environment, obviously, for now. We’ve seen a couple of these events now.

” look at the Monte Carlo simulations, look at what is the hurdlerate. So, last year, valuations were high, interest rates were low. And I said, “Look, you’ve got to look at where we are with valuations, and you have to look at where the 10-year Treasury is at. Is it at 1.5%?

Company HurdleRates This post has already become much longer than I intended it to be, but I want to end by bringing these equity risk premiums down to the company level, and examining how they play out in hurdlerates, to be used in investment analysis by companies and valuation by investors.

And one of the worst performing factors has been valuation. So we’re now in an environment where all the 45-year-old portfolio managers out there have been, have worked their entire careers in these momentum fueled markets, and they’ve been trained to believe that valuation doesn’t matter. 00:50:03 Not anymore.

00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. The second is behavioral.

Country Risk in Business Most corporate finance classes and textbooks leave students with the proposition that the right hurdlerate to use in assessing business investments is the cost of capital, but create a host of confusion about what exactly that cost of capital measures.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content