This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

In my last post, I noted the decline in costs of capital for firms over time, noting that the median cost of capital at the start of 2022 is only 6.33%, across global firms, and argued that companies that demand double-digit hurdlerates risk being shut out of investments.

In my last post, I noted the decline in costs of capital for firms over time, noting that the median cost of capital at the start of 2022 is only 6.33%, across global firms, and argued that companies that demand double-digit hurdlerates risk being shut out of investments.

Societe Generale also offers a dedicated and simplified solution to retail clients or small and midsize enterprises (SMEs) based on their ESG rating. Finally, establishing connectivity to CRX Markets improves support for Societe Generales largest clients to help grow the banks SCF programs.

In January 1993, I was valuing a retail company, and I found myself wondering what a reasonable margin was for a firm operating in the retail business. Employee Count & Compensation I nvesting Principle Financing Principle Dividend Principle HurdleRate Project Returns Financing Mix Financing Type Cash Return Dividends/Buyback s 1.

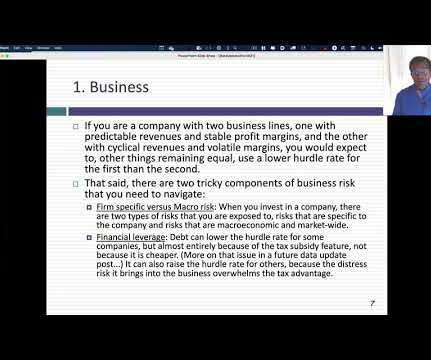

With more mature companies, as investment opportunities become scarcer, at least relative to available capital, the focus not surprisingly shifts to financing mix, with a lower hurdlerate being the pay off.

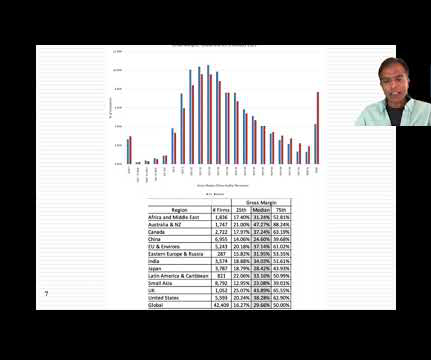

Some of that variation can be attributed to different mixes of businesses in different regions, since unit economics will result in higher gross margins for technology companies and commodity companies, in years when commodity prices are high, and lower gross margins for heavy manufacturing and retail businesses.

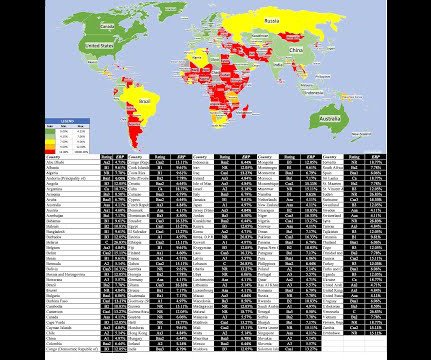

Thus, if a country derives 50% of its economic output from iron ore, a drop in the price of iron ore will cause pain not only for mining companies but also for retailers, restaurants and consumer product companies in the country.

So it’s gonna take a little more confidence, you know, and equities to, because you get your, your hurdlerates higher, you know? So bears capitulated from institution, from retail investors, and the three month VIX versus VIX move below one to suggest, you know, capitulation on that indicator.

So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. You had all these retail traders who started trading crypto and the available functionality of what you could build in crypto really exploded. You had a market that was being dominated by retail.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content