This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

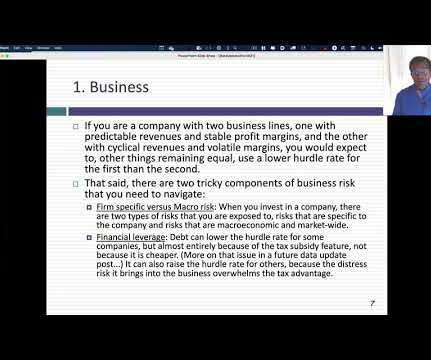

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

Not surprisingly, the operating metrics change as companies age, with high revenue growth accompanied by big losses (from work-in-progress business models) and large reinvestment needs (to delivery future growth) in early-stage companies to large profits and free cash flows in the mature phase to stresses on growth and margins in decline.

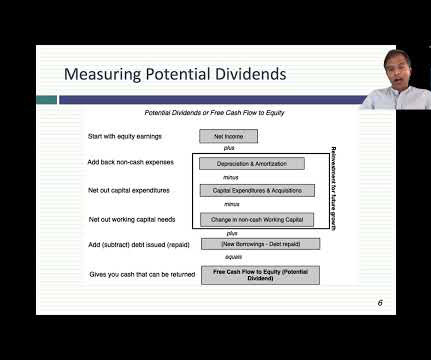

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

And you know, just simple things like, hey, the value of tax loss harvesting, how do you make that apparent to people? But the true change comes when, hey, you know what, those loyal to that technological change figure out over not one, two, but three, five years, how to drive change and how to leverage it. BUCKLEY: Oh, how about 2?

So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. This is implicitly leverage. Leverage is a tool that accentuates both the good and the bad. And you need to be aware of the leverage risk that’s embedded. The second is behavioral.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content