This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It is the end of the first full week in 2025, and my data update for the year is now up and running, and I plan to use this post to describe my data sample, my processes for computing industry statistics and the links to finding them. Insider, CEO & Institutional holdings 2. Aggregate operating numbers 3. Beta & Risk 1.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

Additionally, SCF makes cash flow more predictable, aiding in better emergency planning. Financial institutions can better understand the risk profiles of small suppliers by leveraging alternative data and machine learning, thus expanding access to financing. It also boosts adaptability and maintains stability in challenging markets.

And we had prioritized all our strategic plans, we had to figure out how to get them done while people were remote. But the true change comes when, hey, you know what, those loyal to that technological change figure out over not one, two, but three, five years, how to drive change and how to leverage it. That means a low hurdlerate.

Michael Kitces is Head of Planning Strategy at Buckingham Strategic Wealth , a turnkey wealth management services provider supporting thousands of independent financial advisors. In 2010, Michael was recognized with one of the FPA’s “Heart of Financial Planning” awards for his dedication and work in advancing the profession.

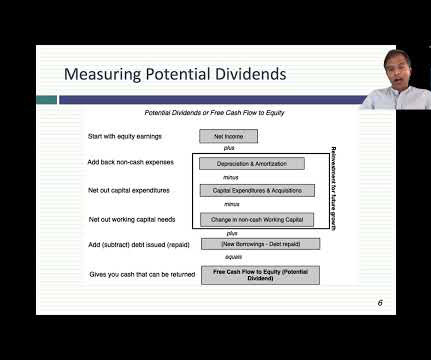

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

What was the original career plan? SALISBURY: Honestly, I didn’t really have a long-term plan. SALISBURY: Yes, I’d love to tell you there was some great master plan. A great example, you know, some of these things you can plan for and some you can’t. You begin in audit practice at KPMG.

I mean, I didn’t want to blow my own trumpet up too much because most of the positions were in place, the quality funds, which more defensive and less leveraged, and low allocation to — a relatively low allocation to equities, and then the hedge funds sort of long/short positions that benefited in the financial crisis.

Quantitative investing was, was that the plan from the beginning? So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. This is implicitly leverage. Leverage is a tool that accentuates both the good and the bad. It was not.

What was the original career plan? There was hardly any time for, for planning. 00:26:19 [Speaker Changed] It, it’s, it’s usually it is aggressive shorts from leveraged funds on s and p futures. And I think you will also, with no further ado, my conversation with B of A Securities, Steven Sutt Meyer.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content