This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

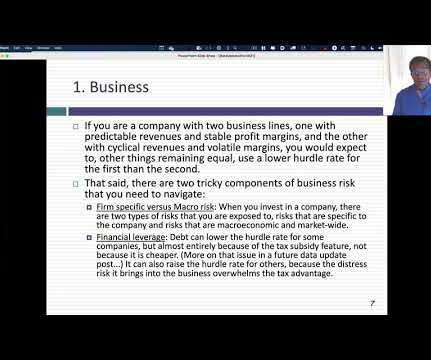

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Insider, CEO & Institutional holdings 2.

Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all. Data universe : In my sample, I include all publicly traded firms with market capitalizations that exceed zero, traded anywhere in the world.

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there.

It also boosts adaptability and maintains stability in challenging markets. According to a report published by market research and consulting firm IMARC Group, the global SCF market reached $7.5 According to a report published by market research and consulting firm IMARC Group, the global SCF market reached $7.5

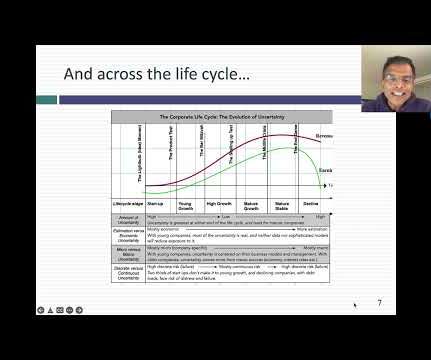

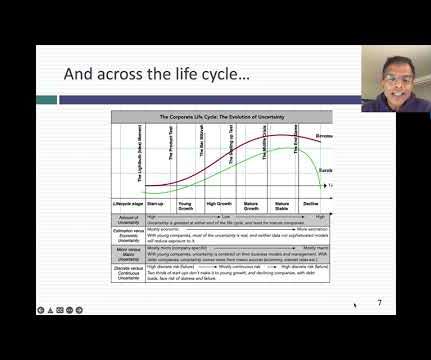

The second is to look at the industry group or sector that a company is in, and then follow up by classifying that industry group or sector into high or low growth; for the last four decades, in US equity markets, tech has been viewed as growth and utilities as mature.

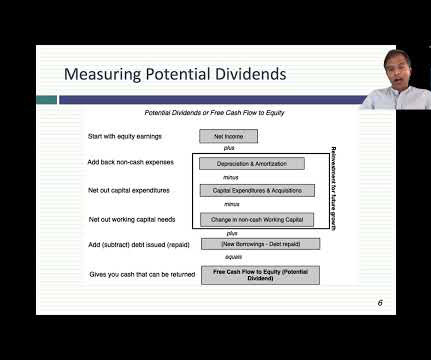

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all. Data universe : In my sample, I include all publicly traded firms with market capitalizations that exceed zero, traded anywhere in the world.

And then in a fit of madness, I guess, at the end of 2006, the credit markets were pretty uninteresting. So I had an interest in the Russian market. One, the London market is where it’s been most of my career. I knew the market, but I also knew the people there. There wasn’t a lot to do. SALISBURY: Yes.

directly via email: Resources Featured In This Episode: Looking for sample client service calendars, marketing plans, and more? And we’re going to talk about what’s going on in the markets, briefly talk about the portfolio. ” look at the Monte Carlo simulations, look at what is the hurdlerate.

Note that this framework applies for all businesses, from the smallest, privately owned businesses, where debt takes the form of bank loans and even credit card borrowing and equity is owner savings, the largest publicly traded companies, where debt can be in the form of corporate bonds and equity is shares held by public market investors.

And I love business, I love the markets, I want to go there. What sort of challenges — BUCKLEY: A couple of bear markets. BUCKLEY: We’ve had, let’s see, inflation at a 40-year high, tightest labor market of our lifetimes. We were losing market share in the critical retirement, the 401(k) business.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. RITHOLTZ: That’s how you know it’s going to be low?

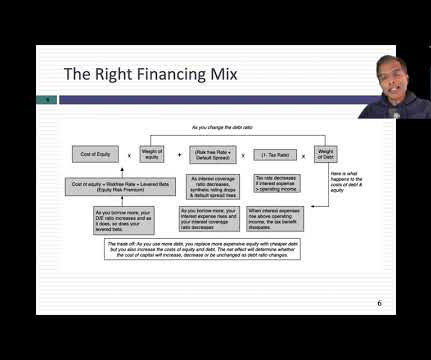

The cost of debt is lower than the cost of equity : If you review my sixth data update on hurdlerates , and go through my cost of capital calculation, there is one inescapable conclusion. At every level of debt, the cost of equity is generally much higher than the cost of debt for a simple reason.

He, he does some really, really interesting research and gets deep into the weeds on things like market structure, liquidity cascades, what really drives returns, how much should you be focused on alpha versus beta. And I, and I really like the application of math and statistics and computer science to markets. It’s just a model.

You work at Capital Growth Financial and in former global markets before you join investing Giant Merrill Lynch in 2007, what was that transition like from smaller shops to a really, really big one? You go on the road, you see offices, they ask you questions about markets, stocks, things like that. That’s right.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content