This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I spend most of my time in the far less rarefied air of corporate finance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. In this role, the cost of capital is an opportunity cost, measuring returns you can earn on investments on equivalent risk.

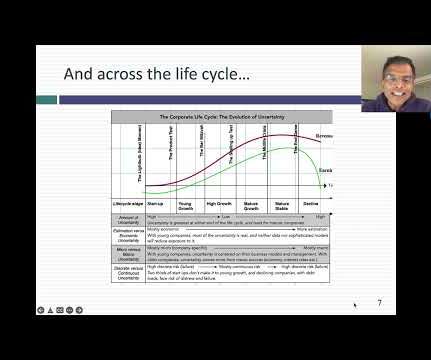

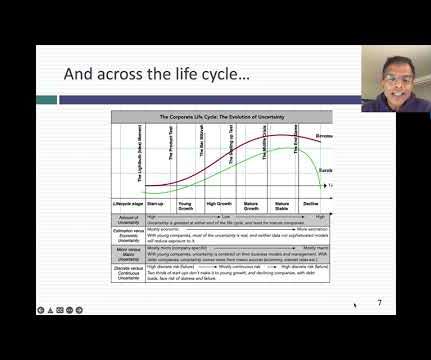

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Tech companies age in dog years, and the consequences for how we manage, value and invest in them are profound.

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Return on (invested) capital 2. Beta & Risk 1.

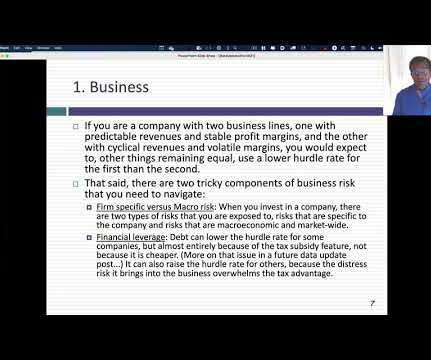

What is a hurdlerate for a business? There are multiple definitions that you will see offered, from it being the cost of raising capital for that business to an opportunity cost , i.e., a return that you can make investing elsewhere, to a required return for investors in that business. What is a hurdlerate?

In fact, almost every investment scam in history, from the South Sea Bubble to Bernie Madoff, has offered investors the alluring combination of great opportunities with no or low danger, and induced by sweet talk, but made blind by greed, thousands have fallen prey. Let me use two illustrations to bring this home.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a risk free investment?

In fact, almost every investment scam in history, from the South Sea Bubble to Bernie Madoff, has offered investors the alluring combination of great opportunities with no or low danger, and induced by sweet talk, but made blind by greed, thousands have fallen prey. Let me use two illustrations to bring this home.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. That said, to use mean reversion in analysis or investing, you need to know what these averages are, either over time or across companies, and data can help in that pursuit. .

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. To make comparisons, profits are scaled to common metrics, with revenues and book value of investment being the most common scalar. Returns on Invested Capital (or Equity).

In pursuit of an answer to that question, I used company-specific data from Value Line, one of the earliest entrants into the investment data business, to compute an industry average. In January 1993, I was valuing a retail company, and I found myself wondering what a reasonable margin was for a firm operating in the retail business.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. To make comparisons, profits are scaled to common metrics, with revenues and book value of investment being the most common scalar.

Thus, you and I can disagree about whether beta is a good measure of risk, but not on the principle that no matter what definition of risk you ultimately choose, riskier investments need higher hurdles than safer investments.

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He co-chairs a number of the asset management investment committees. I thought this was an absolutely fascinating way to see the world of investment management. Investment banks were not really a known concept in the area where I grew up.

It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses.

Put simply, I possess no exclusivity here, and staying consistent with my thesis, I don't expect to expect to make money by investing based upon this data. The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporate finance or valuation issues. So, why bother?

The Price of Risk The price of risk is what investors demand as a premium, an extra return over and above what they can make on a guaranteed investment (risk free), to invest in a risky asset. Intuitively, if you want to earn a higher risk premium on an investment, holding cash flows fixed, you will pay less for that investment today.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. You can imagine, you give a bearish message at a bullish investment conference, and no one listens to you.

” look at the Monte Carlo simulations, look at what is the hurdlerate. So, last year, valuations were high, interest rates were low. And I said, “Look, you’ve got to look at where we are with valuations, and you have to look at where the 10-year Treasury is at. Is it at 1.5%?

To the extent that divide is not just descriptive, but also drives real world investment, both companies and investors may be misallocating their capital, and I will argue for finer delineations of risk. I have my reasons. I know that the currency choice is the source of angst for many analysts, and I think unnecessarily so.

She is one of the few people who combine quantitative investing with behavioral finance. No, I think that that’s the part of it that I find the most interesting is the idea that, you know, a stock price doesn’t really have a, you know, the fair value of an an investment instrument is somewhat arbitrary. Right, right.

I, if you are at all interested in concepts of things like portable alpha or return stacking, or just want to know how a quant looks at the world of investing and tries to decide where there are opportunities. Quantitative investing was, was that the plan from the beginning? Let’s talk a little bit about your background.

Country Risk: Determinants At the risk of stating the obvious, investing and operating in some countries is much riskier than investing and operating in others, with variations in risk on multiple dimensions. Political Structure Would you rather invest/operate in a democracy than in an autocracy?

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content