This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth.

What is a hurdlerate for a business? There are multiple definitions that you will see offered, from it being the cost of raising capital for that business to an opportunity cost , i.e., a return that you can make investing elsewhere, to a required return for investors in that business. What is a hurdlerate?

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income. The numbers yield interesting insights. .

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there. Let me use two illustrations to bring this home.

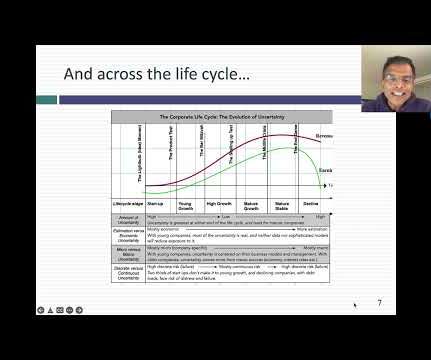

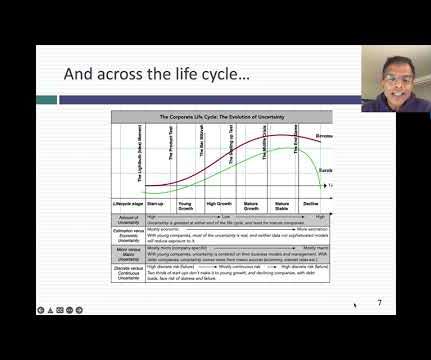

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Tech companies age in dog years, and the consequences for how we manage, value and invest in them are profound.

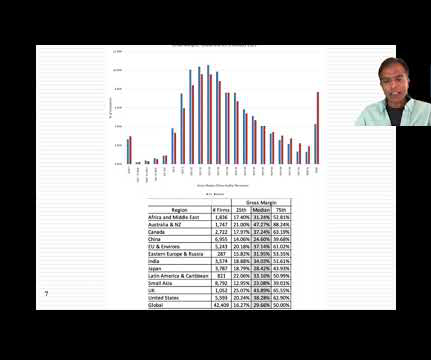

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

That said, to use mean reversion in analysis or investing, you need to know what these averages are, either over time or across companies, and data can help in that pursuit. . Check rules of thumb : Investing and corporate finance are full of rules of thumb, many of long standing.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a risk free investment?

In the first few weeks of 2022, we have had repeated reminders from the market that risk never goes away for good, even in the most buoyant markets, and that when it returns, investors still seem to be surprised that it is there. Let me use two illustrations to bring this home.

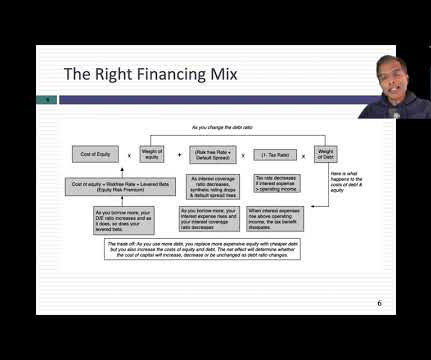

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income. The numbers yield interesting insights.

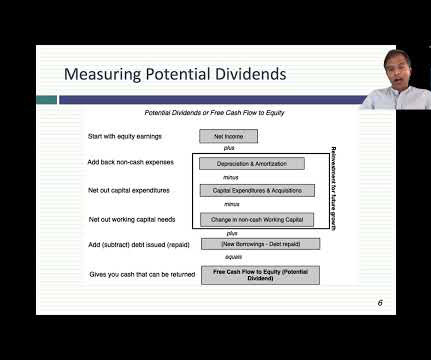

After reporting on the total cash returned during the year, by public companies, in the form of dividends and buybacks, I scale the cash returned to earnings (payout ratios) and to market cap (yield) and present the cross sectional distribution of both statistics across global companies.

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

It also boosts adaptability and maintains stability in challenging markets. According to a report published by market research and consulting firm IMARC Group, the global SCF market reached $7.5 According to a report published by market research and consulting firm IMARC Group, the global SCF market reached $7.5

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He co-chairs a number of the asset management investment committees. I thought this was an absolutely fascinating way to see the world of investment management. Investment banks were not really a known concept in the area where I grew up.

In pursuit of an answer to that question, I used company-specific data from Value Line, one of the earliest entrants into the investment data business, to compute an industry average. In January 1993, I was valuing a retail company, and I found myself wondering what a reasonable margin was for a firm operating in the retail business.

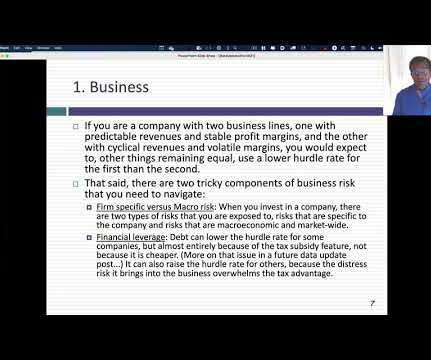

Thus, you and I can disagree about whether beta is a good measure of risk, but not on the principle that no matter what definition of risk you ultimately choose, riskier investments need higher hurdles than safer investments. That tells me three things.

And I love business, I love the markets, I want to go there. What sort of challenges — BUCKLEY: A couple of bear markets. BUCKLEY: We’ve had, let’s see, inflation at a 40-year high, tightest labor market of our lifetimes. We have lowered the cost of investing, and we have improved the quality of those funds.

It is to remedy this defect that analysts scale profits to invested capital, with equity and capital variants: In the equity version, you divide net income by book equity to estimate a return on equity, a measure of what equity investors are generating on the capital they have invested in a company.

Investors are constantly in search of a single metric that will tell them whether a market is under or over valued, and consequently whether they should buying or selling holdings in that market. Note that this price is set by demand and supply and will reflect everything that investors collectively believe, hope for, and fear.

As stock and bond markets went through these gyrations, it should come as no surprise that the same forces were playing out in other markets as well. While most investments fall into one of these buckets, there are some that can span two or more, and you have to decide which one dominates.

That said, to use mean reversion in analysis or investing, you need to know what these averages are, either over time or across companies, and data can help in that pursuit. Check rules of thumb : Investing and corporate finance are full of rules of thumb, many of long standing.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms. So, why bother?

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. You can imagine, you give a bearish message at a bullish investment conference, and no one listens to you.

directly via email: Resources Featured In This Episode: Looking for sample client service calendars, marketing plans, and more? And we’re going to talk about what’s going on in the markets, briefly talk about the portfolio. ” look at the Monte Carlo simulations, look at what is the hurdlerate.

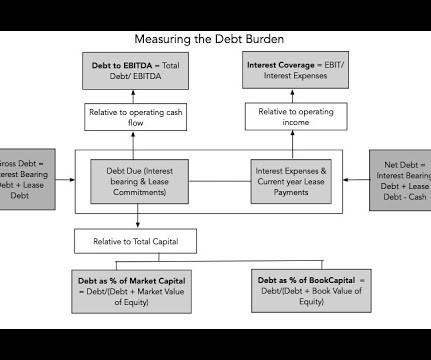

Debt's place in business To understand debt's role in a business, I will start with a big picture perspective, where you break a business down into assets-in-place, i.e., the value of investments it has already made and growth assets, the value of investments you expect it to make in the future.

In my last data updates for this year, I looked first at how equity markets rebounded in 2023 , driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound.

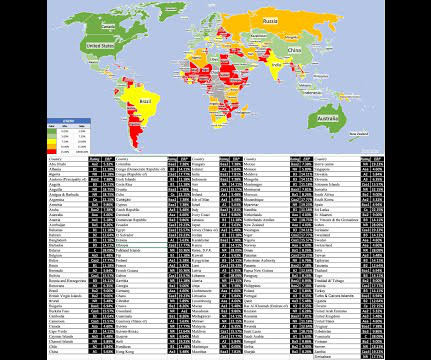

The other is pragmatic , since it is almost impossible to value a company or business, without a clear sense of how risk exposure varies across the world, since for many companies, either the inputs to or their production processes are in foreign markets or the output is outside domestic markets.

The first part of the statement, i.e., that borrowing money increases the expected return on equity in an investment, is true, for the most part, since you have to contribute less equity to get the deal done, and the net income you generate, even after interest payments, will be a higher percentage of the equity invested.

She is one of the few people who combine quantitative investing with behavioral finance. No, I think that that’s the part of it that I find the most interesting is the idea that, you know, a stock price doesn’t really have a, you know, the fair value of an an investment instrument is somewhat arbitrary. Right, right.

He, he does some really, really interesting research and gets deep into the weeds on things like market structure, liquidity cascades, what really drives returns, how much should you be focused on alpha versus beta. Quantitative investing was, was that the plan from the beginning? Let’s talk a little bit about your background.

You work at Capital Growth Financial and in former global markets before you join investing Giant Merrill Lynch in 2007, what was that transition like from smaller shops to a really, really big one? You go on the road, you see offices, they ask you questions about markets, stocks, things like that. That’s right.

After the 2008 market crisis, I resolved that I would be far more organized in my assessments and updating of equity risk premiums, in the United States and abroad, as I looked at the damage that can be inflicted on intrinsic value by significant shifts in risk premiums, i.e., my definition of a crisis.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content