This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I spend most of my time in the far less rarefied air of corporate finance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Tech companies age in dog years, and the consequences for how we manage, value and invest in them are profound.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income. Returns on Invested Capital (or Equity).

SCF also helps buyers and sellers mitigate the impact of high interest ratesproviding welcome relief from the rising cost of manufacturing goods. Best Sustainable Supply Chain Finance Program Santander In August 2024, Danish wind turbine manufacturer Vestas mandated Santander Brazil to deploy a 50 million Brazilian real ($8.3

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income.

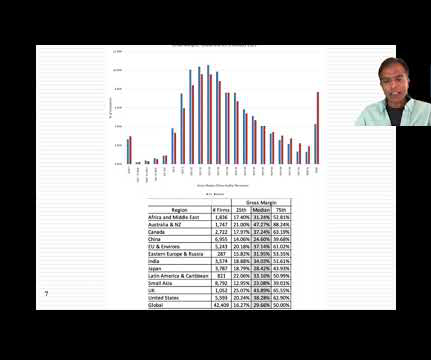

Some of that variation can be attributed to different mixes of businesses in different regions, since unit economics will result in higher gross margins for technology companies and commodity companies, in years when commodity prices are high, and lower gross margins for heavy manufacturing and retail businesses.

Thus, you and I can disagree about whether beta is a good measure of risk, but not on the principle that no matter what definition of risk you ultimately choose, riskier investments need higher hurdles than safer investments. That tells me three things.

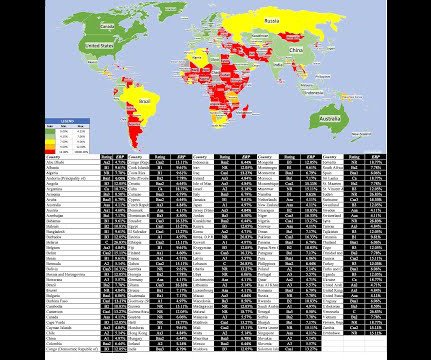

Country Risk: Determinants At the risk of stating the obvious, investing and operating in some countries is much riskier than investing and operating in others, with variations in risk on multiple dimensions. Political Structure Would you rather invest/operate in a democracy than in an autocracy?

The first part of the statement, i.e., that borrowing money increases the expected return on equity in an investment, is true, for the most part, since you have to contribute less equity to get the deal done, and the net income you generate, even after interest payments, will be a higher percentage of the equity invested.

She is one of the few people who combine quantitative investing with behavioral finance. No, I think that that’s the part of it that I find the most interesting is the idea that, you know, a stock price doesn’t really have a, you know, the fair value of an an investment instrument is somewhat arbitrary. Right, right.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content