This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

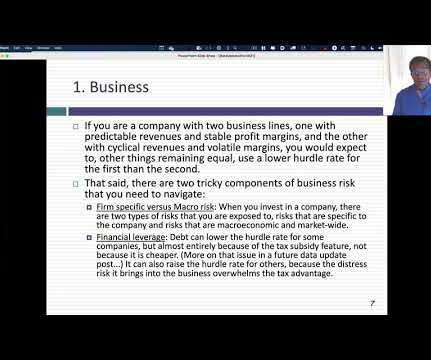

I spend most of my time in the far less rarefied air of corporate finance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

What is a hurdlerate for a business? There are multiple definitions that you will see offered, from it being the cost of raising capital for that business to an opportunity cost , i.e., a return that you can make investing elsewhere, to a required return for investors in that business. What is a hurdlerate?

In corporate finance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Return on (invested) capital 2. Tax rates 4.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

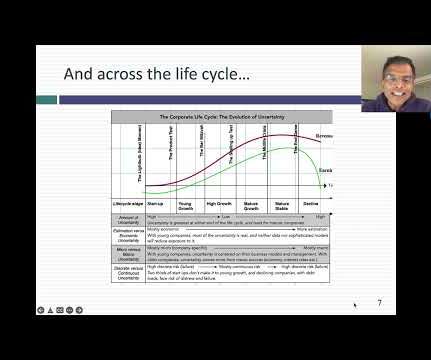

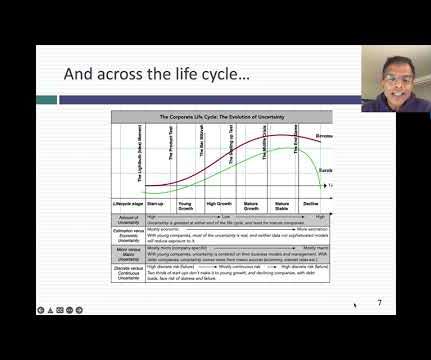

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Tech companies age in dog years, and the consequences for how we manage, value and invest in them are profound.

In fact, almost every investment scam in history, from the South Sea Bubble to Bernie Madoff, has offered investors the alluring combination of great opportunities with no or low danger, and induced by sweet talk, but made blind by greed, thousands have fallen prey. Let me use two illustrations to bring this home.

In fact, almost every investment scam in history, from the South Sea Bubble to Bernie Madoff, has offered investors the alluring combination of great opportunities with no or low danger, and induced by sweet talk, but made blind by greed, thousands have fallen prey. Let me use two illustrations to bring this home.

That said, to use mean reversion in analysis or investing, you need to know what these averages are, either over time or across companies, and data can help in that pursuit. . Check rules of thumb : Investing and corporate finance are full of rules of thumb, many of long standing.

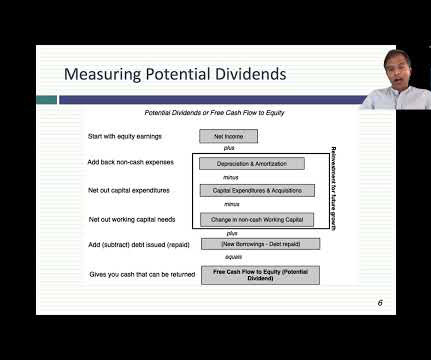

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

Financial institutions can better understand the risk profiles of small suppliers by leveraging alternative data and machine learning, thus expanding access to financing. It requires accurate data, robust technology, and thorough risk assessment, crucial to ensuring the creditworthiness of suppliers at all levels.

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He co-chairs a number of the asset management investment committees. I thought this was an absolutely fascinating way to see the world of investment management. Investment banks were not really a known concept in the area where I grew up.

That said, to use mean reversion in analysis or investing, you need to know what these averages are, either over time or across companies, and data can help in that pursuit. Check rules of thumb : Investing and corporate finance are full of rules of thumb, many of long standing. EV/EBIT and EV/EBITDA 4. High-Low Price Risk Measure 5.

We have lowered the cost of investing, and we have improved the quality of those funds. It forced us to make some tough choices in that time in some big investments, whether we were building out our advice capabilities and building virtual teams to do it, or you know, tough choices in our retirement business. BUCKLEY: Yeah.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. You can imagine, you give a bearish message at a bullish investment conference, and no one listens to you.

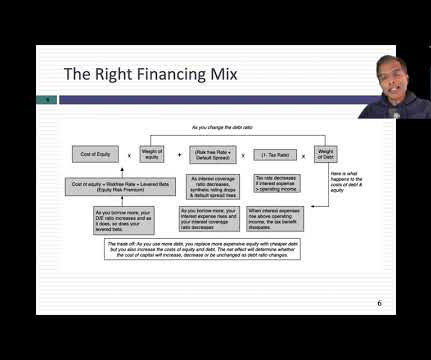

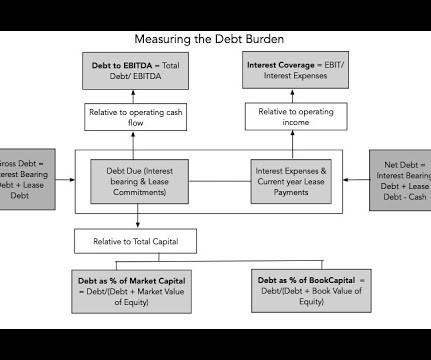

Debt's place in business To understand debt's role in a business, I will start with a big picture perspective, where you break a business down into assets-in-place, i.e., the value of investments it has already made and growth assets, the value of investments you expect it to make in the future. Do companies optimize financing mix?

You do the math and you’re like, “Okay, well, an advisor can handle about 100 clients, an associate advisor can help with some of those clients, you can leverage maybe an associate advisor with a couple of advisors, but there’s a capacity limit for each of the roles.” And I’d been there just over two years.

The first part of the statement, i.e., that borrowing money increases the expected return on equity in an investment, is true, for the most part, since you have to contribute less equity to get the deal done, and the net income you generate, even after interest payments, will be a higher percentage of the equity invested.

I, if you are at all interested in concepts of things like portable alpha or return stacking, or just want to know how a quant looks at the world of investing and tries to decide where there are opportunities. Quantitative investing was, was that the plan from the beginning? Let’s talk a little bit about your background.

You work at Capital Growth Financial and in former global markets before you join investing Giant Merrill Lynch in 2007, what was that transition like from smaller shops to a really, really big one? 00:26:19 [Speaker Changed] It, it’s, it’s usually it is aggressive shorts from leveraged funds on s and p futures.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content