This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Until last year, revenue recognition had been the most common GAAP violation alleged since Cornerstone first began tracking the class action suits in 2019.

Strong public market valuations in key sectorsespecially technology and healthcareare attracting growth-driven businesses. Non-GAAP Measures and Key Performance Indicators (KPIs) Non-GAAP financial measures and KPIs play a crucial role in shaping investor perceptions and demonstrating a companys value proposition.

Their initial response was to increase their human intervention in 2008: They changed their inventory valuation assumption, their revenue recognition assumptions, and a few other things. Horton: If they have an IPO, theyll be big firms, and theyll follow International Financial Reporting Standards or US GAAP. Horton: Heres one.

So now is the perfect time to make sure you report in kind gift donations in compliance with GAAP standards in 2022. The changes to in kind donation reporting are specifically for organizations that follow generally accepted accounting principles (GAAP) in preparing their financial statements.

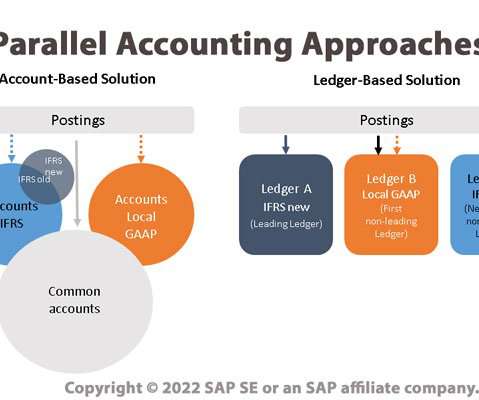

For example, a company with branches doing business in the United States and the European Union will need to comply with both GAAP and IFRS accounting principles. The account-based approach uses account logic identifiers to assign accounting principles, such as using unique prefixes to determine which accounts use IFRS vs GAAP principles.

The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies.

Stock prices opened at $15 but popped pretty immediately thereafter, shooting up 56 percent by the end of the first day — and locking Lending Club’s valuation in at $8.5 Lending Club’s valuation never got much higher than that $10 billion mark, but it did manage to keep its share price above its IPO value for the first half of 2014.

EBITDA is often used in financial analysis and business valuation because it provides a more standardized and consistent measure of a company's operating performance, especially when comparing companies with different capital structures or when assessing their ability to generate cash from operations.

If your organization falls into the $50,000-$200,000 range but must complete an annual audit for funding or GAAP purposes, it is wise to skip Form 990-EZ and head straight to the full form. . Full Form 990. For nonprofits earning over $200,000.

Analysts attributed this less to the performance of Coupa, and more to macro trends, including the overall stock market drop on Tuesday, and an inflated stock valuation for Coupa to begin with, The Motley Fool said. Despite the positive news, reports noted that Coupa shares slumped following the release of its earnings data.

Pro forma financial statements and GAAP It's important to note that, since pro forma statements are based on hypothetical or projected data, they are not compliant with generally accepted accounting principles—GAAP statements must be based on actual financial results. A pro forma invoice is not a type of pro forma financial statement.

Valuations are a classic example of hole-filled financial reporting. History is riddled with companies that went public based on inflated valuations and false narratives. WeWork expected to offer shares to the public at a $47 billion valuation. If you want to build shareholder trust, start with the data.

Conduct Comprehensive Account Reconciliations Transitioning from a Cash basis to US GAAP accrual basis accounting is essential, providing a more accurate representation of an organization’s financial position. Standards like revenue recognition and lease accounting stand out, demanding rigorous attention.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. IFRS and GAAP now treat as leases as debt, but that is still not the case in many other markets that are not covered by either standard). The numbers yield interesting insights. .

Goodwill = P− (A − L ) where: P=Purchase price A=Fair market value of assets L=Fair market value of liabilities T-Mobile/Sprint Merger: A Real Life Goodwill Valuation In 2018, T-Mobile acquired Sprint to the tune of $35.85 At the time of the acquisition, the fair market value for the Sprint corporation was determined to be $78.34

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. IFRS and GAAP now treat as leases as debt, but that is still not the case in many other markets that are not covered by either standard). The numbers yield interesting insights.

This measure is a direct product of fair value reporting, a principle insisting that assets be reported at their market value, which forms the bedrock of financial reporting standards under US GAAP.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. It is very likely that these rules of thumb were developed from data and observation, but at a different point in time.

Are your books organized and GAAP compliant? Your CFO can help you set goals for your business in terms of sales, assets, and growth to target a particular valuation. What do you want the transition to look like? What are the key value drivers of your business? What are your plans for managing your debt?

IFRS, US GAAP). Valuation and Reporting: Properly recognizing and valuing intangible assets impacts financial statements, investor relations, and the company’s market valuation. Is there a significant difference between US GAAP and IFRS , or are we just being a bit too conservative here in South Africa?

The numbers are non-GAAP, which would indicate a somewhat clearer-eyed picture of what consensus expects, but still, again, we are in uncharted territory as we have only the second decline in the bottom line coming in recent memory. So, valuations are enough to start people thinking or sweating … and possibly, selling.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content