This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For example, while South African companies follow International FinancialReporting Standards (IFRS), the US requires compliance with its Generally Accepted Accounting Principles (GAAP). IFRS is principles-based and allows for some judgment in financialreporting, while GAAP is more rigid, rules-based, and less forgiving.

The consolidation process typically includes aggregating financial results, eliminating intercompany transactions, handling currency conversions, and ensuring compliance with accounting standards like the International FinancialReporting Standards (IFRS) or Generally Accepted Accounting Principles GAAP.

Despite these favorable conditions, successful IPOs require meticulous preparation, robust financialreporting, and a governance framework that instills investor confidence. Companies must ensure they are operationally, financially, and strategically ready for the transition to public markets.

Take a critical look at areas prone to audit issues—such as revenue recognition, procurement, impairment, and financialreporting—ensuring that controls in these high-risk areas meet compliance standards.

Here in the UK, the FinancialReporting Council looked into audit papers of the FTSE 100 and basically gave them a good health score. Horton: If they have an IPO, theyll be big firms, and theyll follow International FinancialReporting Standards or US GAAP. GF: Why is so much fraud connected with IPOs?

How a CFO Ensures Compliance in FinancialReporting Reliable financial statements are crucial for business management, but ensuring compliance may feel like a luxury in the resource-constrained world of small business. How can a small business ensure compliance in reporting without overspending on accounting staff and audits?

The difference between cost of goods sold and ordinary business expenses is well defined in Generally Accepted Accounting Principles (GAAP) but routinely ignored by small business bookkeeping services. Even worse, an IRS income tax return does not follow the same rules as GAAP. Interest expense. R&D expenses. state income tax).

But the deadline for making the changes has passed, and the FINAL deadline (for interim reporting periods) is coming up next month. So now is the perfect time to make sure you report in kind gift donations in compliance with GAAP standards in 2022. When do the changes to in kind gift reporting go into effect?

Financial Management Moving from basic bookkeeping to GAAP-compliant accounting became necessary as the organization grew. Blackwell is now focused on developing more sophisticated financial management skills. Do You Struggle to Make Sense of Your Financial Statements? Book a FREE consultation here. Get the free guide!

Assurance is an opinion given by a CPA on the accuracy of an organization’s financial statements. It shows whether or not your accounting records are accurate per generally accepted accounting principles (GAAP), in the auditor’s professional judgment. Nonprofit Audit Alternative #1: Financial Review .

The way revenue and expenses are recorded can differ for GAAP purposes and tax purposes ( Form 990 ). For tax, this excess amount is reported as a contribution, and for GAAP, it can be reported as either a contribution or special event revenue. It will not be reported on Form 990. Get the free guide!

When choosing the best financialreporting software solution, it's important to consider factors such as ease of use, scalability, integration with existing systems, compliance with accounting standards, cost, customer support, and any unique requirements your organization might have. What is financialreporting software?

Periodic financialreporting is a great example. Most organizations put a great deal of manual effort into their periodic reporting. Our customers love to tell us how many inefficiencies they had in their reporting process before they started using the Planful Platform for financialreporting.

As you might already know, US GAAP doesn't have an awful lot to say about carve-outs or carve-out financial statements. Well, the SEC has provided a few scant crumbs here and there but, for the most part, financial organizations are on their own. And by awful lot , we mean nothing. Not a peep.

Their responsibilities already entail ensuring that the financialreport is accurate, complete and verifiable, according to GAAP accounting standards and disclosures. CFOs are the logical candidate to lead the ESG initiative.

In an ideal world, financialreports should build shareholder trust by offering accurate data about the performance of the company. In reality, a company’s financialreport can be more flimsy—involving estimates and judgment from leadership that’s far from the truth. at its peak to $0.26

Your core financialreports, which we’ll look at below, exist to answer this one simple question– how much value has your organization created ? It shows as a liability on your financialreports, so it reduces your net assets. It’s easier for simple tax filings and less susceptible to financial misconduct.

individual and corporation connections), history, donor intent, or soft credits Accounting software tracks financial transactions with strict adherence to GAAP Integrating two systems with fundamentally different data priorities can risk data inconsistencies, inaccuracies, and loss of information. Contact us today to learn more!

Whether it’s streamlining financialreporting, enhancing data accuracy, or ensuring compliance with South African regulatory standards, clearly defining these objectives will guide the entire design process. Choosing the Right Software and Technology Selecting the appropriate financial software is a critical decision.

Both Generally Accepted Accounting Principles (GAAP) and Financial Accounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit. And the more transparent your accounting system is, the more accountable you’ll be with the public and GAAP.

Cash accounting does not comply with Generally Accepted Accounting Principles (GAAP) for nonprofit organizations. Financial statement audit or review – if you are required to undergo a financial statement audit or assessment, using the accrual method to be in accordance with GAAP will make the process much smoother and less expensive.

Its primary role is to oversee and regulate the auditing of public companies to protect investors' interests and ensure the integrity of financialreporting. Standard-Setting: It plays a role in setting and updating auditing standards to enhance the quality of audits and financialreporting. Why Should You Care?

For that reason, your account numbering, category names, and structure should follow standard guidelines and numbering conventions established by Generally Accepted Accounting Principles (GAAP). . Your financialreports will be organized according to the accounts in your Chart of Accounts. Assets-1000s. Liabilities-2000s.

Using CLM, global companies are better able to manage lease classification such as sales type leases and operating leases, as well as to meet lessor accounting requirements of US GAAP and other country GAAP requirements, or IFRS mandates. Multiple Regulatory Compliance Mandates: Meeting regulatory requirements (e.g.,

A key part of business life is getting the books closed on time, with clean financialreporting that allows a high-level and granular view of what needs to be done next. This is especially true when multinationals must reconcile data across different accounting standards, such as GAAP and IFRS.

In the United States, these Generally Accepted Accounting Principles (or GAAP) are set by the Financial Accounting Standards Board (FASB). First, nonprofits must follow GAAP, the Generally Accepted Accounting Principles. Do You Struggle to Make Sense of Your Financial Statements? 117 (FASB 117). Get the free guide!

Click on the link to download to discover in detail a list of the benefits that IBM Cognos Controller provide for finance teams: Data collection and validation Reconciliations Workflow and tasks to improve the close cycle Currency conversion Minority interest calculations Inter-company eliminations Group closing adjustments Management adjustments Allocations (..)

launched its FinancialReporting Analytics solution, which will be sold as an SAP Solution Extension under the name SAP Account Substantiation and Automation by BlackLine, financial review option. BlackLine, Inc.

All these sources must be carefully managed to ensure compliance with Generally Accepted Accounting Principles (GAAP) and guidelines. This accounting principle outlines specific criteria that must be met before revenue can be recorded in financial statements. Undergo annual financial audits. Receive grants. Employ paid staff.

Reports in The Block Crypto late last week said a group of California CPAs has sent a letter to the Financial Accounting Standards Board, a federal board that sets Generally Accepted Accounting Principles (GAAP), requesting that it consider establishing a task force to address a lack of clarity in cryptocurrency accounting standards.

Nonprofit bookkeeping is the process of entering, classifying, and organizing financial data for the purpose of creating accurate financial records for your organization. They organize the data and ensure accuracy so the accountant can create reliable and timely financialreports.

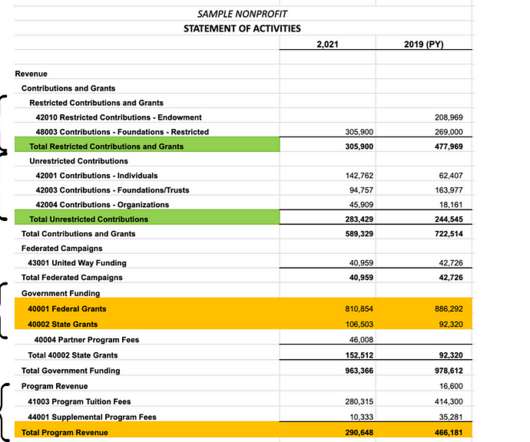

To comply with Generally Accepted Accounting Principles (GAAP), you must separate your revenue into at least 2 categories: Restricted Revenue shows funds with donor-placed restrictions on how or when you can spend the money. At The Charity CFO, we help 150+ nonprofits get audit-ready financialreports monthly, like clockwork.

They also pitch in on major financial moves like mergers and fundraising. They double-check financialreports for accuracy and offer advice to the company leaders and the board. The CFO plays a key role in ensuring these statements are accurate and in line with standard accounting principles (GAAP).

Want to see it in action? Check out our video here. To learn more about the Planning Maestro App for QuickBooks Online Advanced or Planning Maestro and how you can modernize your FP&A process to tackle what lies ahead, view our product demonstration video or call 800.366.5111.

For example, “salary” is a straightforward line-item on a for-profit financialreport. . To complete your IRS 990, you’ll need to report your expenses based on how they fall within 3 categories, they are: . That means you’ll need to present a Functional Expense Report to pass an audit. To build public trust.

Maintaining healthy financial management is critical for the organization’s sustainability, stability, and flexibility, now and in the future. Poor financialreporting. They provide a framework for the oversight and governance of financial operations and activities. Ease the tax reporting. Interdependence.

As a result, the organization might not adhere to Generally Accepted Accounting Principles (GAAP), which can trip them up come tax time or during an audit. When you have a clear financial picture, it builds donor confidence and trust in your organization. . Generates accurate financialreports.

This financialreport contains three segments: 1. GAAP requires that you separate revenue as either: Restricted: This includes all donations that the donor has given directions on how and when you can spend the funds. It helps you comply with GAAP standards and IRS regulations. How much money did you bring in?

Pro forma financial statements and GAAP It's important to note that, since pro forma statements are based on hypothetical or projected data, they are not compliant with generally accepted accounting principles—GAAP statements must be based on actual financial results.

Assessing Accounting For entities preparing GAAP compliant financial statements, adoption of Revenue Recognition Standard (ASC 606) and Lease Accounting Standard (ASC 842) is now mandatory. Changing how revenue is reported impacts EBITDA and also balance sheet items such as deferred revenue and deferred expenses.

Improved Financial Transparency Accrual accounting provides stakeholders with a detailed view of your organization’s financial activities, improving trust and confidence. Transparent financialreporting can also improve donor relations. Many regulatory bodies and grantors require accrual-basis financial statements.

Take a critical look at areas prone to audit issues—such as revenue recognition, procurement, impairment, and financialreporting—ensuring that controls in these high-risk areas meet compliance standards.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content