This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

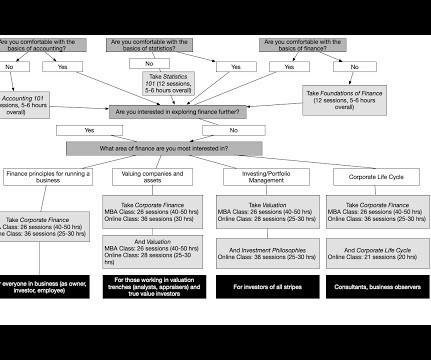

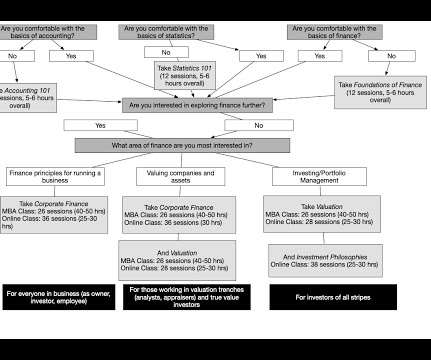

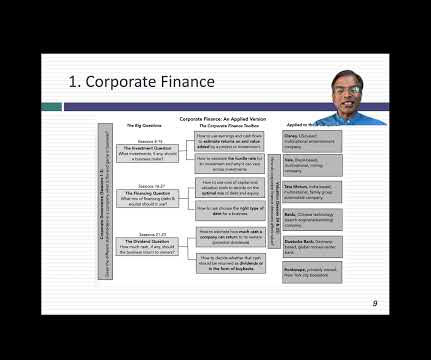

Once I came to NYU in 1986, I continued to teach classes across the finance spectrum, from corporate finance to valuation to investing, and I am glad that I did so. I am a natural dabbler, and I enjoy looking at big financial questions and ideas from multiples perspectives.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporate finance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporate financialanalysis or valuation was a chore. Data universe : In my sample, I include all publicly traded firms with market capitalizations that exceed zero, traded anywhere in the world.

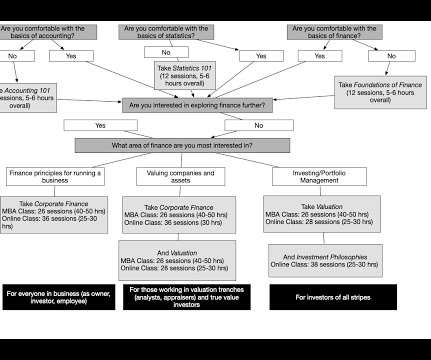

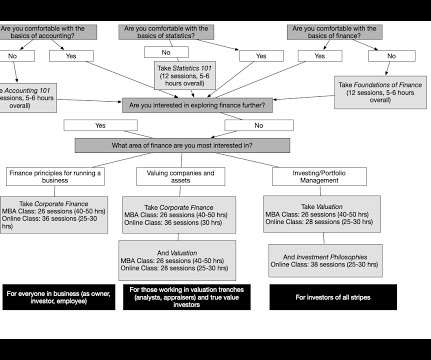

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. The second set of inputs are prices of risk, in both the equity and debt markets, with the former measured by equity risk premiums , and the latter by default spreads.

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings!

The second was a comment that I made on a LinkedIn post that had built on my implied equity premium approach to the Indian market but had run into a roadblock because of an assumption that, in an efficient market, the return on equity would equate to the cost of equity.

I balked at teaching this motley collection of topics and wanted to teach a class on valuation, but I was told that there was not enough stuff in valuation to fill a class. In the fall of 1986, I taught a valuation class in my security analyst slot, and with no cameras in the classroom or complaints from students, no one was any wiser.

Business valuation captures more than just your present position—it’s a mirror to your past efforts and a window to future possibilities. As we journey through this article, we’ll illuminate the core factors that breathe life into the valuation of your business. What factors influence business valuation?

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporate finance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023.

These are the financial and non-financial outcomes a company aims to achieve. Whether its breaking into new markets, attaining cash flow positivity, or preparing for an exit strategy, the vision must be clear and measurable. Achieving Buy-In from Teams A standout point in Rogers advice was the emphasis on team alignment.

That year, I computed these industry-level statistics for five variables that I found myself using repeatedly in my valuations, and once I had them, I could not think of a good reason to keep them secret. After all, I had no plans on becoming a data service, and making them available to others cost me absolutely nothing.

This concept is built on the assumption that the market is not static: existing competitors and new entrants are continuously building capabilities to gain their positions on the market. As for established market players, they demonstrate much higher threshold of proof.

How can you be sure the decisions you are making are taking valuation in the right direction? v360 goes beyond traditional financialanalysis and simple snapshots. Qualitative Factors Your company’s culture, leadership, and operational capability are pivotal in determining its market value. How is v360 Different?

To start the year, I returned to a ritual that I have practiced for thirty years, and that is to take a look at not just market changes over the last year, but also to get measures of the financial standing and practices of companies around the world. Happy New Year, and I hope that 2022 brings you good tidings!

This is true in all possible economic situations: in times of growth FP&A participates in setting business objectives, analyzing options of growth, assessing market opportunities and risks, while in times of recession FP&A can contribute to corrective action plans, cost-cutting and other initiatives to preserve company’s financial health.

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online.

The fundamental disruption caused by the COVID-19 pandemic equates to an opportunity for the industry to remake itself in line with new societal realities and market needs. She explained that these days it is about integrating the experience of governance, valuation, reporting, products, and reinsurance to deliver value for shareholders.

It is perhaps a reflection of my age that I remember when getting data to do corporate financialanalysis or valuation was a chore. Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses.

Macro Investment Market Challenges a Headwind for Private Equity Valuations Private Equity Sponsors are facing their most challenging valuationmarket since the great recession of 2008-09. Heightened inflation and interest rates will continue to be valuation headwinds.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post. The second is that the government be perceived as default-free.

I spent the first week of 2021 in the same way that I have spent the first week of every year since 1995, collecting data on publicly traded companies and analyzing how they navigated the cross currents of the prior year, both in operating and market value terms.

And so late 90s, that’s the emergence of the high yield market in Europe, you would print deals like never before. Now, on the positive and the silver lining was that this whole situation started putting a lot of light on, let’s say, the alternative market. Is it just the size of the US market? I think we learned a lot.

The other is pragmatic , since it is almost impossible to value a company or business, without a clear sense of how risk exposure varies across the world, since for many companies, either the inputs to or their production processes are in foreign markets or the output is outside domestic markets.

And then, then I real, I decided to leave investment banking, which I, or I learned a tremendous amount, especially the, you know, putting, you know, the strategic nature of looking at industries and companies, and of course all of the, the financial acumen, the rigor of, of doing very intensive financialanalysis. I 100% agree.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content