This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Here are four of the most common audit preparation obstacles and practical ways to overcome them, based on client experience supporting finance teams through efficient and streamlined audits. Ensure that impairment analyses are completed according to audit priorities, with asset groupings and forecast data that align with GAAP standards.

Finance organizations regularly face the challenges of meeting strict deadlines and satisfying data quality requirements for closing the books and delivering accurate financial statements. It enables finance teams to automate and accelerate the financial close with minimal IT support. DOWNLOAD NOW.

In a survey conducted by the Institute of Management Accountants (IMA), and sponsored by Blackline, titled “Process Automation in Accounting and Finance,” examining the attitudes and concerns of 750 financial professionals surrounding accounting and month-end closing processes, manual activities remain prevalent — at the cost of time and money.

It’s essential to engage with various stakeholders—including finance teams, auditors, and even IT professionals—to identify the specific needs that your system must address. A user-friendly interface can significantly reduce the learning curve and increase the system’s adoption rate among your finance team.

Using CLM, global companies are better able to manage lease classification such as sales type leases and operating leases, as well as to meet lessor accounting requirements of US GAAP and other country GAAP requirements, or IFRS mandates. Multiple Regulatory Compliance Mandates: Meeting regulatory requirements (e.g.,

individual and corporation connections), history, donor intent, or soft credits Accounting software tracks financial transactions with strict adherence to GAAP Integrating two systems with fundamentally different data priorities can risk data inconsistencies, inaccuracies, and loss of information.

Here are four of the most common audit preparation obstacles and practical ways to overcome them, based on client experience supporting finance teams through efficient and streamlined audits. Ensure that impairment analyses are completed according to audit priorities, with asset groupings and forecast data that align with GAAP standards.

Here are four of the most common audit preparation obstacles and practical ways to overcome them, based on client experience supporting finance teams through efficient and streamlined audits. Ensure that impairment analyses are completed according to audit priorities, with asset groupings and forecast data that align with GAAP standards.

In the United States, these Generally Accepted Accounting Principles (or GAAP) are set by the Financial Accounting Standards Board (FASB). First, nonprofits must follow GAAP, the Generally Accepted Accounting Principles. NPOs must adhere to these accounting policies to remain compliant with the law and maintain their tax-exempt status.

With the right tools and processes in place, the year-end close and reporting process can be less stressful and painful for the Finance team, maybe – dare I say it – even something you look forward to. Intercompany reconciliations were a nightmare, with many phone calls to the foreign subs. Watch the Webinar Replay. Ah, the memories!

FASB's role and functions include: Standard-Setting: The primary responsibility of the FASB is to develop and update Generally Accepted Accounting Principles (GAAP), which serve as the foundation for financial reporting by public and private companies, non-profit organizations, and government entities in the U.S.

Sure, your mission should be a priority, but managing finances can’t be neglected either. Without a good grasp of your finances, your nonprofit risks: Exposure to fraud. When creating your fiscal policy, ensure that it complies with the Generally Accepted Accounting Principles (GAAP). Bring GAAP compliance.

Bookkeepers, accountants, and Chief Financial Officers (CFOs) all serve critical roles in managing an organization’s finances. An accountant generally holds a bachelor’s degree in accounting or finance. But did you know there are a variety of financial professionals that are essential to the financial well-being of an organization?

If the latter is the case, Planful recently held a webinar focused on how you can automate and accelerate the financial close, consolidation, and reporting process and free up more Finance time for value-added analysis. Many Finance professionals may think that only large enterprises need a formal financial consolidation process and system.

From the collection and consolidation of financial results, to the creation of year-end financial statements, to audits and regulatory filings – finance teams are often distraught throughout the process. These results then require consolidation following US GAAP or IFRS guidelines. Attend to Reconciliations Early.

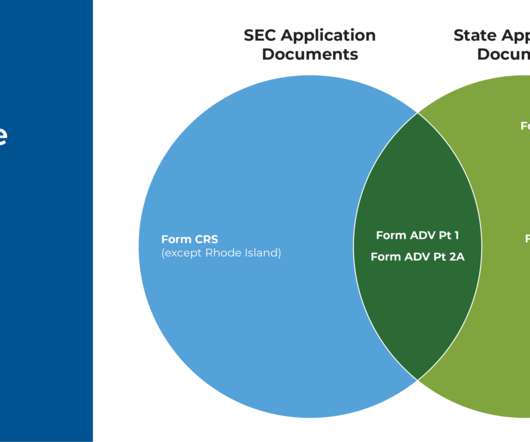

Along with renewing their registration annually (for both SEC- and state-registered firms), firms face a variety of requirements related to their internal finances, fees, marketing activities, and advisor agreements depending on whether they are SEC- or state-registered. RIA Fee Itemization And Surprise Custody Audits.

Not being compliant with US GAAP or IFRS. Streamline adjustments and intercompany reconciliations by 50 – 80%. Finance time shifts to value-added analysis, reduce hiring needs. Challenges in consolidating multiple spreadsheets and correcting errors. Limited reporting and analysis capabilities, and too much manual effort.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content