This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Despite these favorable conditions, successful IPOs require meticulous preparation, robust financialreporting, and a governance framework that instills investor confidence. Companies must ensure they are operationally, financially, and strategically ready for the transition to public markets.

Global Finance: Can you briefly describe what your model does? Here in the UK, the FinancialReporting Council looked into audit papers of the FTSE 100 and basically gave them a good health score. Horton: If they have an IPO, theyll be big firms, and theyll follow International FinancialReporting Standards or US GAAP.

In response, 82% of CFOs report that investments in digital are accelerating faster than in other areas, including talent, supply chain, business services or fixed assets. What does this mean to the finance and accounting team of 2022? The next stages of digital transformation will drive this growing demand for multi-skilled talent.

Take a critical look at areas prone to audit issues—such as revenue recognition, procurement, impairment, and financialreporting—ensuring that controls in these high-risk areas meet compliance standards.

How a CFO Ensures Compliance in FinancialReporting Reliable financial statements are crucial for business management, but ensuring compliance may feel like a luxury in the resource-constrained world of small business. How can a small business ensure compliance in reporting without overspending on accounting staff and audits?

AI coupled with The Digitization of the Finance Function create powerful levers for today’s CFO. AI in the “Real World” While these powerful tools seem to have a near mastery of natural language communication, they are not necessarily designed to possess many of the skills required by finance and accounting professionals.

Financial Management Moving from basic bookkeeping to GAAP-compliant accounting became necessary as the organization grew. Blackwell is now focused on developing more sophisticated financial management skills. Do You Struggle to Make Sense of Your Financial Statements? Book a FREE consultation here. Get the free guide!

Assessing Accounting For entities preparing GAAP compliant financial statements, adoption of Revenue Recognition Standard (ASC 606) and Lease Accounting Standard (ASC 842) is now mandatory. Changing how revenue is reported impacts EBITDA and also balance sheet items such as deferred revenue and deferred expenses.

But the deadline for making the changes has passed, and the FINAL deadline (for interim reporting periods) is coming up next month. So now is the perfect time to make sure you report in kind gift donations in compliance with GAAP standards in 2022. When do the changes to in kind gift reporting go into effect?

Finance organizations regularly face the challenges of meeting strict deadlines and satisfying data quality requirements for closing the books and delivering accurate financial statements. IBM Cognos Controller supports the close, consolidation and reporting process with the agility and affordability of a cloud-based solution.

The way revenue and expenses are recorded can differ for GAAP purposes and tax purposes ( Form 990 ). For tax, this excess amount is reported as a contribution, and for GAAP, it can be reported as either a contribution or special event revenue. It will not be reported on Form 990. Get the free guide!

You need to get a better grasp of your organization’s finances now. So you can understand what’s happening in your business and communicate effectively with your board members, donors, and financial team. It shows as a liability on your financialreports, so it reduces your net assets. It’s a necessity.

It’s essential to engage with various stakeholders—including finance teams, auditors, and even IT professionals—to identify the specific needs that your system must address. A user-friendly interface can significantly reduce the learning curve and increase the system’s adoption rate among your finance team.

Periodic financialreporting is a great example. Most organizations put a great deal of manual effort into their periodic reporting. They throw finance bodies at the task of requesting, gathering, collating, and organizing the required data. That is, until the offending task pops up again. That’s just one simple example.

(GOOGL) stock worth over $20 million, his financial portfolio is quite diversified. Anthony Noto Anthony Noto, a famous finance executive and former NFL exec, now wears the CEO and CFO hats at a fintech company named SoFi. Ianniello is well-known in finance circles. They're all about keeping the company's finances in good shape.

In an ideal world, financialreports should build shareholder trust by offering accurate data about the performance of the company. In reality, a company’s financialreport can be more flimsy—involving estimates and judgment from leadership that’s far from the truth. at its peak to $0.26

Both Generally Accepted Accounting Principles (GAAP) and Financial Accounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit. And the more transparent your accounting system is, the more accountable you’ll be with the public and GAAP.

Building and managing an effective budget and plan can be daunting no matter what industry, but financial planning for nonprofits can be particularly difficult. It’s all automated and GAAP compliant. But understanding the financial impact of decisions is just the tip of the iceberg. No programming. No formulas.

But that’s not quite true—nonprofits face a decision between 2 different accounting methods for tracking their financial activity: cash accounting vs. accrual accounting. Though both systems use the same numbers, looking at those numbers differently can give you a very different perspective on the state of your finances.

individual and corporation connections), history, donor intent, or soft credits Accounting software tracks financial transactions with strict adherence to GAAP Integrating two systems with fundamentally different data priorities can risk data inconsistencies, inaccuracies, and loss of information. Contact us today to learn more!

A key part of business life is getting the books closed on time, with clean financialreporting that allows a high-level and granular view of what needs to be done next. This is especially true when multinationals must reconcile data across different accounting standards, such as GAAP and IFRS.

Using CLM, global companies are better able to manage lease classification such as sales type leases and operating leases, as well as to meet lessor accounting requirements of US GAAP and other country GAAP requirements, or IFRS mandates. Multiple Regulatory Compliance Mandates: Meeting regulatory requirements (e.g.,

All these sources must be carefully managed to ensure compliance with Generally Accepted Accounting Principles (GAAP) and guidelines. Understanding how and when to recognize different revenue is perhaps one of the most important but difficult aspects of managing a nonprofit’s finances. Undergo annual financial audits.

It’s during times like this where it’s important for finance teams to evaluate their budgeting, planning, and forecasting processes, evolve priorities and implement best practices to ensure they have insight and confidence needed to navigate the year ahead and beyond. Key Priorities & Requirements for Finance in 2023.

Episode 243 Becoming a Treasurer Series, Part 24: Languages of Finance: FP&A As we jump back into the Becoming a Treasurer series, we are launching a new sub-series where we will look at the “language of finance.” What are some of the different ways we look at it in finance, accounting as a view of it?

Its primary role is to oversee and regulate the auditing of public companies to protect investors' interests and ensure the integrity of financialreporting. Standard-Setting: It plays a role in setting and updating auditing standards to enhance the quality of audits and financialreporting. Why Should You Care?

In the United States, these Generally Accepted Accounting Principles (or GAAP) are set by the Financial Accounting Standards Board (FASB). First, nonprofits must follow GAAP, the Generally Accepted Accounting Principles. Do You Struggle to Make Sense of Your Financial Statements? 117 (FASB 117). Get the free guide!

AI coupled with The Digitization of the Finance Function create powerful levers for today’s CFO. AI in the “Real World” While these powerful tools seem to have a near mastery of natural language communication, they are not necessarily designed to possess many of the skills required by finance and accounting professionals.

For example, “salary” is a straightforward line-item on a for-profit financialreport. . To complete your IRS 990, you’ll need to report your expenses based on how they fall within 3 categories, they are: . That means you’ll need to present a Functional Expense Report to pass an audit. To build public trust.

Whether you are an educational, charitable, religious, sports, or other public-benefit organization, you need to have a good handle on your finances in order to make the most impact. Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting.

In the detail-oriented world of finance, where precision and foresight are paramount, financial professionals often grapple with the daunting task of consolidating multiple Profit & Loss statements (P&Ls). This not only hampers efficiency but also poses a significant risk to the accuracy of financialreporting.

Many nonprofit organizations tend to let their financial management slip on the backburner as they get busy fulfilling their mission. Sure, your mission should be a priority, but managing finances can’t be neglected either. Without a good grasp of your finances, your nonprofit risks: Exposure to fraud. A Nonprofit Budget.

This financialreport contains three segments: 1. GAAP requires that you separate revenue as either: Restricted: This includes all donations that the donor has given directions on how and when you can spend the funds. It helps you comply with GAAP standards and IRS regulations. How much money did you bring in?

Take a critical look at areas prone to audit issues—such as revenue recognition, procurement, impairment, and financialreporting—ensuring that controls in these high-risk areas meet compliance standards.

Take a critical look at areas prone to audit issues—such as revenue recognition, procurement, impairment, and financialreporting—ensuring that controls in these high-risk areas meet compliance standards.

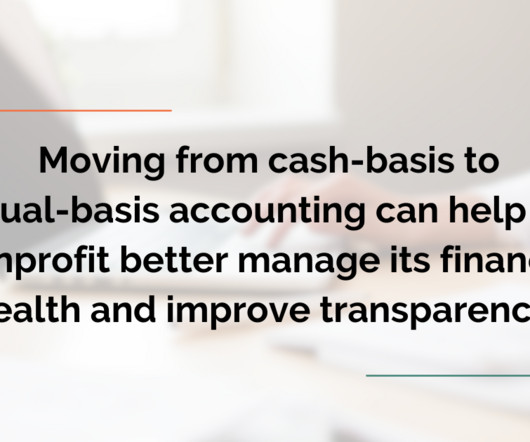

While many nonprofits start with cash-basis accounting due to its simplicity, this method often falls short of providing a comprehensive view of a nonprofit’s financial health. Transitioning to accrual-basis accounting can offer a more accurate representation of finances and enhance long-term planning. Get the free guide!

Pro forma statements are financial projections that ask and attempt to answer "what if" questions. What will our finances look like?" The Securities and Exchange Commission (SEC) requires that discrepancies between pro forma and GAAP-compliant financialreports be explained when released to the public.

But did you know there are a variety of financial professionals that are essential to the financial well-being of an organization? Bookkeepers, accountants, and Chief Financial Officers (CFOs) all serve critical roles in managing an organization’s finances. Do You Struggle to Make Sense of Your Financial Statements?

Building and maintaining an effective budget is daunting no matter what industry you’re in — but financial planning for nonprofits is especially tough. The best financial management software is totally automated and GAAP-compliant, and gets rid of the pain from errors cased by linking complex formulas and macros across spreadsheets.

If the latter is the case, Planful recently held a webinar focused on how you can automate and accelerate the financial close, consolidation, and reporting process and free up more Finance time for value-added analysis. Financial Close, Consolidation, and Reporting – Who Cares? Multi-GAAPreporting (i.e.,

Company founders and CEOs are rarely equipped to handle financing strategies, budgets and dealing with investors. But bringing on a chief financial officer is not cheap. He also stepped outside of his world of finance and dove into other parts of our business. It’s a growing pain that many small businesses have.

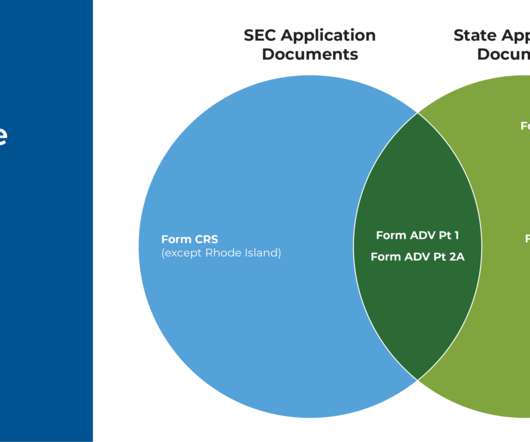

Along with renewing their registration annually (for both SEC- and state-registered firms), firms face a variety of requirements related to their internal finances, fees, marketing activities, and advisor agreements depending on whether they are SEC- or state-registered. RIA Fee Itemization And Surprise Custody Audits.

Limited reporting and analysis capabilities, and too much manual effort. Not being compliant with US GAAP or IFRS. The next logical step is to replace the spreadsheet-based process with purpose-built enterprise performance management (EPM) applications designed to streamline budgeting, planning, and financialreporting.

Accounting Standards In the United States, all organizations must adhere to the Generally Accepted Accounting Principles (GAAP). When understanding how employees affect your financial health, consider: Organizational chart – ensuring that you have the right people in the right positions can make an organization run smoothly.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content