This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I am in the third week of the corporate finance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet.

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporate finance, this takes the form of a hurdlerate , a minimum acceptable return on an investment, for it to be funded.

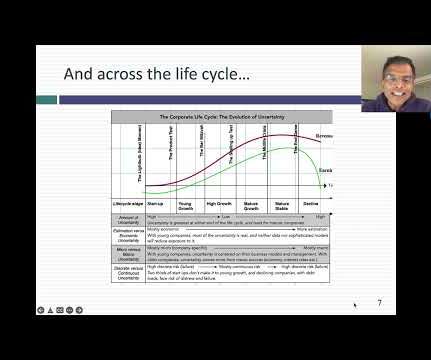

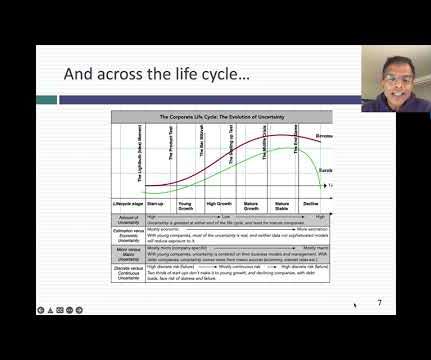

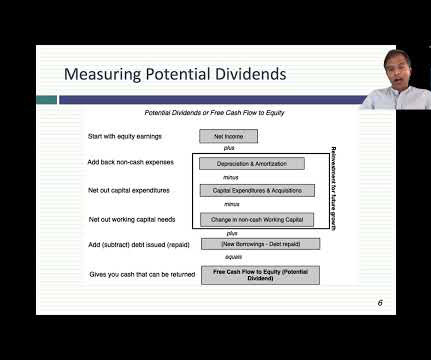

The question of whether a company is making or losing money should be a simple one to answer, especially in an age where accounting statements are governed by a myriad of rules, and a legion of number-crunchers follow these rules to report profits generated by a firm. The numbers yield interesting insights. .

Measuring Profitability The question of whether a company is making or losing money should be a simple one to answer, especially in an age where accounting statements are governed by a myriad of rules, and a legion of number-crunchers follow these rules to report profits generated by a firm. The numbers yield interesting insights.

By providing immediate cash flow, SCF helps suppliers avoid the pitfalls of traditional loans that can be challenging to secure during economic downturns. billion by 2033 as economic and geopolitical pressures reshape how businesses approach working capital and financing. billion in 2024 and is expected to reach $15.2

With more mature companies, as investment opportunities become scarcer, at least relative to available capital, the focus not surprisingly shifts to financing mix, with a lower hurdlerate being the pay off. That portfolio will have the benefit of stability, but expecting it to contain ten-baggers and hundred-baggers is a reach.

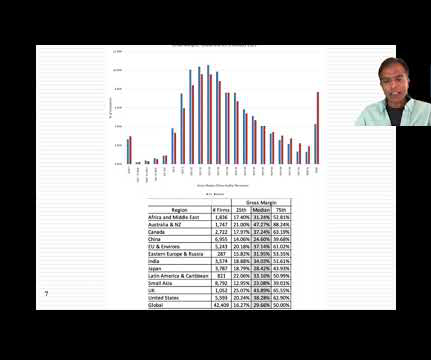

Starting with gross margins, and computing the number for all non-financial service firms, we report the distribution of gross margins across publicly traded companies at the start of 2023, again based upon gross income and sales in the most recent twelve months: While the median gross margin across all publicly traded global firms is about 30%.,

Last week, was my data week, where I download and analyze data on all publicly traded companies, listed anywhere in the world, and I will post extensively on what the numbers look like after a most tumultuous year. As we approach the turn of the calendar year, I have my own set of rituals that prepare me for the new year.

In my last post , I described the wild ride that the price of risk took in 2020, with equity risk premiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year. between US large cap and small cap, 0.70

In the picture below, I use this process to estimate an equity risk premium of 4.72% for the S&P 500 on January 1, 2021: Download spreadsheet to compute ERP It is true that my estimates of earnings and cash flows in the future are driving my premium, and that the premium will be lower (higher) if I have under (over) estimated those numbers.

Because the economics of profitability start showing up particularly when you’re starting to hire other advisors and staff and team. ” look at the Monte Carlo simulations, look at what is the hurdlerate. And so, that can move the numbers, as well. And so, that can move the numbers, as well.

In the second, Warren Buffet used some heated language to describe those who opposed buybacks, calling them “economic illiterates” and “silver tongued demagogues “. Going back in time to last year’s inflation reduction act, buybacks were explicitly targeted for taxes, with the perspective that they were damaging US companies.

As the risk-free rate rises, expected returns on equities will be pushed up, and holding all else constant, stock prices will go down., and the reverse will occur, when risk-free rates drop. Ultimately, a government that chooses to default is making a political choice, as much as it is an economic one.

Mean reversion : I am not a knee-jerk believer in mean reversion, but the tendency for numbers to move back towards averages is a strong one. Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all.

Mean reversion : I am not a knee-jerk believer in mean reversion, but the tendency for numbers to move back towards averages is a strong one. Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all.

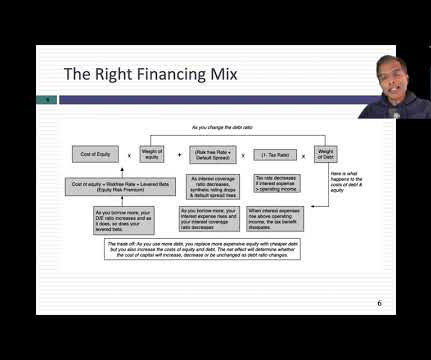

Furthermore, do they optimize they debt ratios to deliver the lowest hurdlerates. In the late 1990s, it was an economic recession that was the precipitating factor, but the last three increases in delinquencies have had their origins in other forces. Do companies optimize financing mix?

In closing, I also want to dispense with the notion that data is objective and that numbers-focused people have no bias. Finally, it is worth noting that, notwithstanding the travails of last year, the number of firms in the data universe increased from 44,394 firms at the start of 2020 to 46,579 firms, a 4.9%

CHANCELLOR: And I actually — one of my last projects at GMO was to do a sort of — to look at what was going on from economic sentiment perspective, looking at various different measures in a bull bear ratio, amount of margin loans in system. Essentially, that’s what interest rates allow. back in sort of 2012.

In particular, there are wide variations in how risk is measured, and once measured, across companies and countries, and those variations can lead to differences in expected returns and hurdlerates, central to both corporate finance and investing judgments.

The cost of debt is lower than the cost of equity : If you review my sixth data update on hurdlerates , and go through my cost of capital calculation, there is one inescapable conclusion. At every level of debt, the cost of equity is generally much higher than the cost of debt for a simple reason. to3.5%) during the year.

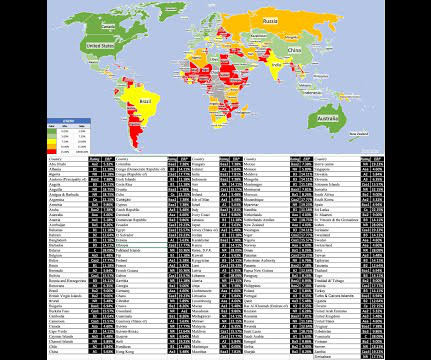

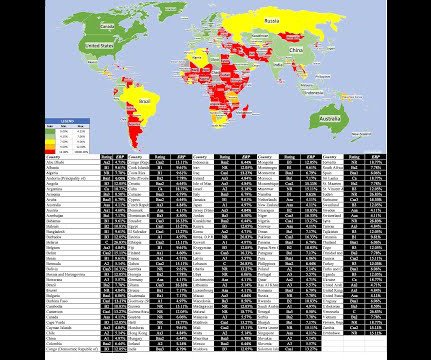

One is curiosity , as political and economic crises roll through regions of the world, roiling long-held beliefs about safe and risky countries. The graph below shows the sovereign CDS levels, by country: Source: Bloomberg ( July 2023 data ) There are three things to note, as you browse these numbers.

So it’s got this math angle where it, you know, it’s all numbers, but then there’s this behavioral angle and psychological angle where, you know, it’s, it’s kind of a fun problem to tackle. It’s kind of a silly number, but people are going to think you’re smart or dumb based on that number.

Honest back testing, really looking at the numbers versus exaggerating returns and, and making up the claim that something’s live when it’s not. There’s very few, I would argue probably no consistent predictors of, of any sort of economic or market cyclicality. 12, 14 even that not a lot of numbers.

And 00:06:38 [Speaker Changed] Door number one was much better than door number three in, in the circumstances. When we talk about breadth, we’re talking about the numbers of advancers versus decliners. So it’s like, yeah. It, it’s, it’s a totally, it’s, it’s very different.

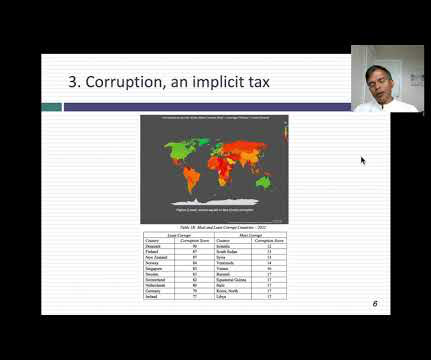

In the section below, I highlight the differences on four major dimensions - political structure, exposure to war/violence, extent of corruption and protections for legal and property rights, with the focus firmly on the economic risks rather than on social consequences. That is easier said than done, for two reasons.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content