This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

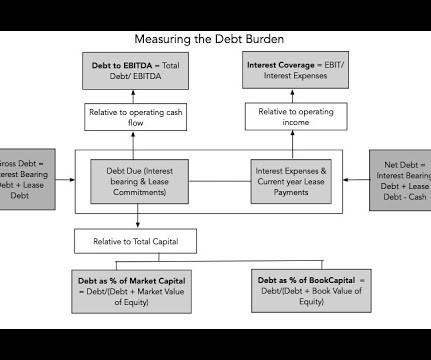

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporate finance, this takes the form of a hurdlerate , a minimum acceptable return on an investment, for it to be funded.

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporate finance, this takes the form of a hurdlerate , a minimum acceptable return on an investment, for it to be funded.

The last few years have been eventful for all companies, with the COVID crisis and ensuing economic shut down causing pain for companies, with recovery coming in 2021, as the global economy opened up again. Costs grow at a slower rate than revenues. Superior unit economics. Economies of scale. High gross margins. YouTube Video.

The last few years have been eventful for all companies, with the COVID crisis and ensuing economic shut down causing pain for companies, with recovery coming in 2021, as the global economy opened up again. I will use this data to draw three broad conclusions: Low HurdleRate ?

As the risk-free rate rises, expected returns on equities will be pushed up, and holding all else constant, stock prices will go down., and the reverse will occur, when risk-free rates drop. Ultimately, a government that chooses to default is making a political choice, as much as it is an economic one.

By providing immediate cash flow, SCF helps suppliers avoid the pitfalls of traditional loans that can be challenging to secure during economic downturns. billion by 2033 as economic and geopolitical pressures reshape how businesses approach working capital and financing. billion in 2024 and is expected to reach $15.2

Much of my focus, when it comes to data, is on company-specific variables, rather than macro economic data, for two reasons. Federal Reserve Economic Data (FRED) : This is hands down, in my view, the best site for macroeconomic data in the world.

. “ Global Corporate Banking 2016: The Next-Generation Corporate Bank ” found that less than a third of corporate banking divisions across North America and Asia, and less than half in Europe, experienced “positive and growing economic profit” between 2013 and 2015. ” Positive Developments, New Opportunities.

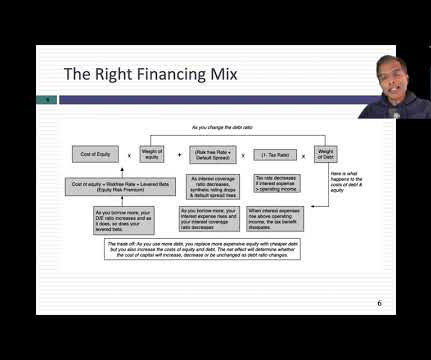

With more mature companies, as investment opportunities become scarcer, at least relative to available capital, the focus not surprisingly shifts to financing mix, with a lower hurdlerate being the pay off.

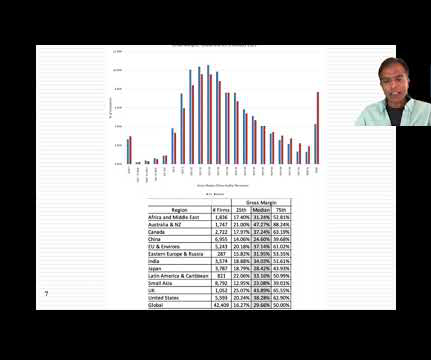

Some of that variation can be attributed to different mixes of businesses in different regions, since unit economics will result in higher gross margins for technology companies and commodity companies, in years when commodity prices are high, and lower gross margins for heavy manufacturing and retail businesses.

Risk free rates over time : While it is generally not a good idea to play interest rate forecaster, we are in unusual times, with rates close to all time lows. Ultimately though, the judgment you make on the market will be a joint effect of your views on the economy and interest rates in the next few years.

Data Items Much of my focus, when it comes to data, is on company-specific variables, rather than macro economic data, for two reasons. Federal Reserve Economic Data (FRED) : This is hands down, in my view, the best site for macroeconomic data in the world.

During 2020, as I watched companies and investors struggle with the after shocks of the economic shut down created by COVID, I wrote a series of fourteen posts (linked below) on what I was learning, unlearning and relearning about corporate finance and valuation.

In my last post , I described the wild ride that the price of risk took in 2020, with equity risk premiums and default spreads initially sky rocketing, as the virus led to global economic shutdowns, and then just as abruptly dropping back to pre-crisis levels over the course of the year. Data Update 4 for 2021: The HurdleRate Question.

The second is that there are great (and free) sources for macro economic data, ranging from the Federal Reserve (FRED) to the World Bank and I don’t see the point of replicating something that they already do well. Data Update 4 for 2021: The HurdleRate Question. Data Update 2 for 2021: The Price of Risk!

In particular, there are wide variations in how risk is measured, and once measured, across companies and countries, and those variations can lead to differences in expected returns and hurdlerates, central to both corporate finance and investing judgments. What's coming?

In the second, Warren Buffet used some heated language to describe those who opposed buybacks, calling them “economic illiterates” and “silver tongued demagogues “. Going back in time to last year’s inflation reduction act, buybacks were explicitly targeted for taxes, with the perspective that they were damaging US companies.

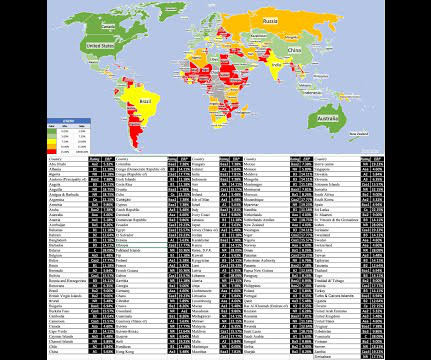

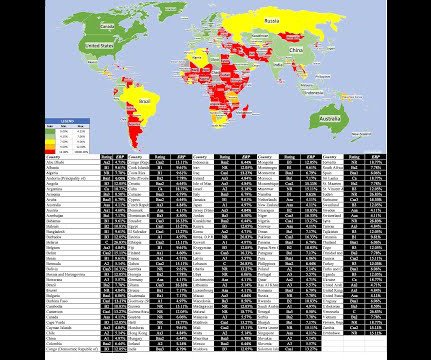

One is curiosity , as political and economic crises roll through regions of the world, roiling long-held beliefs about safe and risky countries. My suggestion is that for countries where recent political or economic events would lead you to believe that sovereign rating is dated, you should switch to using sovereign CDS spreads.

Furthermore, do they optimize they debt ratios to deliver the lowest hurdlerates. In the late 1990s, it was an economic recession that was the precipitating factor, but the last three increases in delinquencies have had their origins in other forces. Do companies optimize financing mix?

CHANCELLOR: And I actually — one of my last projects at GMO was to do a sort of — to look at what was going on from economic sentiment perspective, looking at various different measures in a bull bear ratio, amount of margin loans in system. Essentially, that’s what interest rates allow. back in sort of 2012.

Because the economics of profitability start showing up particularly when you’re starting to hire other advisors and staff and team. ” look at the Monte Carlo simulations, look at what is the hurdlerate. You really have to start crystalizing an org chart and who does what, and clarifying roles and responsibilities.

In the section below, I highlight the differences on four major dimensions - political structure, exposure to war/violence, extent of corruption and protections for legal and property rights, with the focus firmly on the economic risks rather than on social consequences. That is easier said than done, for two reasons.

The cost of debt is lower than the cost of equity : If you review my sixth data update on hurdlerates , and go through my cost of capital calculation, there is one inescapable conclusion. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks! Data Update 6 for 2025: From Macro to Micro - The HurdleRate Question!

But now we’re back to a more normal hurdlerate. 5% interest rates is not super high. I know you like to discuss there are different phases of the, of the, both the market and the economic cycle. I mean, we had a global pandemic, a complete shutdown of global economic activity. 00:50:03 Not anymore.

There’s very few, I would argue probably no consistent predictors of, of any sort of economic or market cyclicality. So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. I think ity economics would argue you have to protect your capital to survive.

And economic indicators, like the unemployment rate or the claims data, and you know, we actually did some scenario analysis around that recently, just talking about, Hey, what happens if the employment rate rises versus falls? I mean, I, I haven’t done that much work. I think, I think it’s probably more useful.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content