This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

EBITDA is often used in financialanalysis and business valuation because it provides a more standardized and consistent measure of a company's operating performance, especially when comparing companies with different capital structures or when assessing their ability to generate cash from operations.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporate financialanalysis or valuation was a chore. Much of my focus, when it comes to data, is on company-specific variables, rather than macro economic data, for two reasons.

His approach involves working backward from desired outcomes, such as an EBITDA goal or exit valuation, and breaking these down into actionable steps and KPIs. He also stressed the importance of monitoring leading indicators, such as sales leads and inventory levels, to address issues before they impact financial performance.

FP&A analyst, in turn, is a promising yet developing profession that can be interesting to graduates with finance, statistics, economics or business degrees as well as to finance professionals from adjacent disciplines. Planning, budgeting and forecasting are linked together forming financial planning processes.

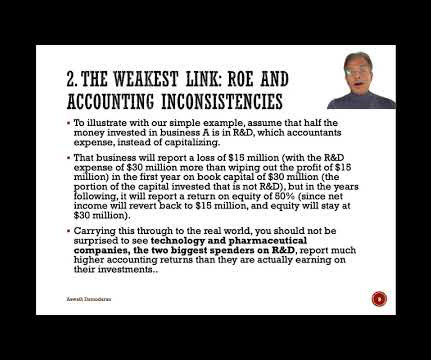

The other is accounting depreciation , which often has little to do with economic depreciation (value lost from aging), and subject to gaming. Extrapolating, projects and companies with older assets will tend to have overstated accounting returns, as inflation and depreciation lay waste to book values.

It is perhaps a reflection of my age that I remember when getting data to do corporate financialanalysis or valuation was a chore. Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. It is very likely that these rules of thumb were developed from data and observation, but at a different point in time.

That said, it is my experience with markets that has also made me skeptical about the over selling of both notions, since we have an entire branch of finance (behavioral finance/economics) that has developed to explain how more data does not always lead to better decisions and why crowds can often be collectively wrong.

That said, it is my experience with markets that has also made me skeptical about the over selling of both notions, since we have an entire branch of finance (behavioral finance/economics) that has developed to explain how more data does not always lead to better decisions and why crowds can often be collectively wrong.

One is curiosity , as political and economic crises roll through regions of the world, roiling long-held beliefs about safe and risky countries. My suggestion is that for countries where recent political or economic events would lead you to believe that sovereign rating is dated, you should switch to using sovereign CDS spreads.

And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from asset valuation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium. RITHOLTZ: So let’s talk a little bit about valuations relative to risk and reward.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content