This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The key benefit of Benfords law is that it doesnt matter what kind of firm it ispublic, private, what accounting policies it follows, what currency it operates in, whether its loss-making, whether its a growth company, highly leveraged or no leverage at allmakes absolutely no difference. Horton: Heres one. And its incredibly difficult.

Business Valuation - Determining the value of assets or entire companies. If the income statement shows a profit, it boosts the equity on the balance sheet. A loss decreases equity. Next, use an appropriate valuation method for each division to estimate their individual worth.

Macro news : While macroeconomic news (about the economy, inflation or currency exchange rates) cuts across the market, in terms of impact, some companies are more exposed to macroeconomic factors than others, and analysts will have to revisit earnings estimates in light of new information.

That year, I computed these industry-level statistics for five variables that I found myself using repeatedly in my valuations, and once I had them, I could not think of a good reason to keep them secret. Valuation Pricing Growth & Reinvestment Profitability Risk Multiple s 1. Profit Margins 1. Earnings Multiples 2.

I was reminded of that paper a few weeks ago, when Fitch downgraded the US, from AAA to AA+, a relatively minor shift, but one with significant psychological consequences for investors in the largest economy in the world, whose currency still dominates global transactions.

In US dollar terms, Latin America was flat in the first half of 2023, though there were a couple of Latin American markets that delivered stellar returns in local currency terms, albeit with high inflation eating away at these returns. US Equities in 2023: Into the Weeds! trillion in the first six months of 2023, 97.2%

If you’re all interested in macro investing, trend following, commodities, currencies, fixed income, various types of quantitative strategies, and most important of all, risk management, you’re going to find this conversation to be absolutely fascinating. But on a relative basis, it was easier. RITHOLTZ: Right. TROPIN: Yeah.

Another year, another bumper crop of profits. In the first quarter of this year, the combined profits of 57 listed banks jumped 10.5% In the first quarter of this year, the combined profits of 57 listed banks jumped 10.5% surge in quarter-on-quarter profits. Quarterly performance was similarly robust, with an 11.8%

The problem with large investments – the type that run into the billions of dollars – is that just as gains can be astronomical, the losses can be devastating. billion rescue, and also said it had taken its valuation of the beleaguered workspace company down by 80 percent, to around $5 billion at the end of the most recent quarter.

The third is currency, with hurdle rates, for any given project, varying across currencies. Currency I have studiously avoided dealing with currencies so far, by denominating all of my illustrations in US dollars, but that may strike some of you as avoidance. Cost of equity in US $ for German project = 1% + 1.1

billion valuation and shares trading at $14-16 a share. At its post-IPO valuation and share price, Etsy was roughly 52 times its adjusted earnings. A pretty impressive feat, considering at the time of its IPO Etsy wasn’t actually profitable yet. A little over a year ago, Etsy IPOed, mostly to a round of applause.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. It is true that the Turkish company will face more risk because of its location, but that is an issue separate from currency.

But on the upside, with the various scandals, higher than expected default rates, and a loss of stock market investor confidence that neatly mirrors the diminishing confidence of platform investors, the various online lenders of the nation have likely gotten good at bracing themselves. Probably not what they were hoping for today.

Turns out that investors get nervous when profits prove elusive. Thus, a possible tech stock market fizzle, should this indeed be a harbinger, where the $2 billion valuation is the same as implied by a Blue Apron funding round two years ago. The ascendant tech IPO that, well, snapped when it reported results?

Neither index is particularly representative, and currency effects contaminate both, but they tell the story of devastation in the two markets. I revisited my valuation of the index, with the updated values: Spreadsheet to value the S&P 500. There are two things to note in this valuation. Flight to Safety and Collectibles.

While the value crowd, bereft of victories for a long time, may be inclined to do a victory dance, it is worth noting that the same phenomenon occurred between February and March of 2020, at the start of the COVID crisis, but that growth companies quickly recouped their losses and finished ahead of mature companies by the end of 2020.

And I found that subsegment really interesting because we did studies on kind of decision making biases, human biases like loss aversion and other biases that impact otherwise what should be rational decisions and make them less than rational. That is not being reflected in valuations from a top down standpoint. Absolutely.

For others, it can be the portion of their capital with the longest time horizon (pension fund savings or 401Ks, if you are a young investor, for example), where they believe that any losses on risk capital can be made up over time. moving towards zero, increasing the costs of staying on the sidelines.

For others, it can be the portion of their capital with the longest time horizon (pension fund savings or 401Ks, if you are a young investor, for example), where they believe that any losses on risk capital can be made up over time. moving towards zero, increasing the costs of staying on the sidelines.

And they go on longer and longer and obviously more profitable for the states that run the lottery. But it makes a big, big difference to your long-term outcomes if you can just avoid those big losses. Then the volatility and, and the valuation makes an enormous difference. That’s the $2 that the lottery is worth for me.

And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from asset valuation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium. RITHOLTZ: So let’s talk a little bit about valuations relative to risk and reward.

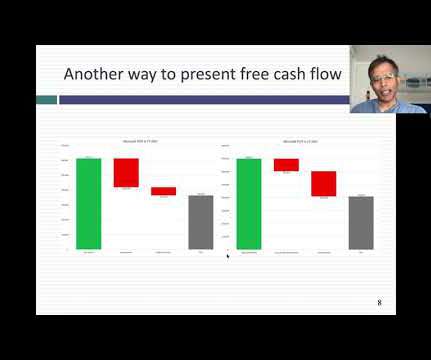

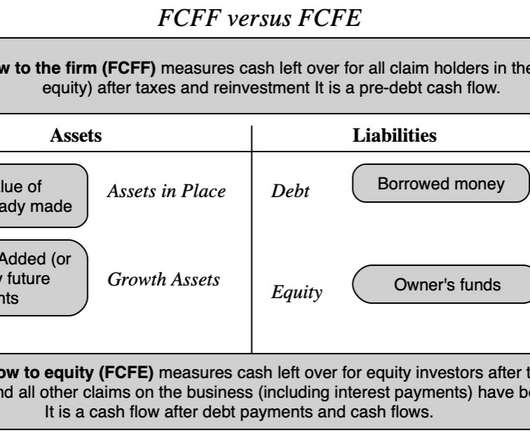

I will use this section to clarify what free cash flows are trying to measure, how they get used in investing and valuation, and the measurement questions that can cause measurement divergences. and which ones to include (cash acquisitions, foreign exchange gains or losses etc.) What is Free cash flow (FCF)?

He sunk all the profits into Bitcoin, he’s levered up and borrowed money and bought Bitcoin. The profits are very small, but Alameda’s cost of capital was very low since they were borrowing all the customer money. They release their profits every quarter. I mean I think his profits overall are, are high.

I will use this section to clarify what free cash flows are trying to measure, how they get used in investing and valuation, and the measurement questions that can cause measurement divergences. and which ones to include (cash acquisitions, foreign exchange gains or losses etc.).

Lately, though, they’re probably tossing and turning over the difficulties with raising capital coupled with the simultaneous descent of their venture’s valuations. And whether, if one and two come true, there’s a business model underneath all of it to profit from. ARE WE SOLVING THE RIGHT PROBLEMS FOR THE RIGHT PEOPLE?

And, you know, therein began, I think the unraveling and, and a little bit of the, the loss of that, you know, cultural juice that had kind of historically made that firm special. And when we experience a loss, right, a 50% loss can happen right? I don’t wanna experience loss. In a very short period of time.

ASNESS: Some of the things like betting against beta, quality or profitability, carry strategies were additions over time. ASNESS: And we had a great almost a decade, because everything else we do work, profitability one; fundamental, momentum one; low risk one. ASNESS: There are a few reasons. RITHOLTZ: Okay. RITHOLTZ: Past decade.

00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. Trades a similar universe of currencies and commodities and, and equities and rates around the world. They took a point and they drew a line. Real really intriguing.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content