This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Managing creditrisk used to be a reactive process. Waiting until account holders fall behind to take action not only meant that customers’ credit scores would take a hit before their banks were alerted to a problem, but also that banks would lose the revenue from the scheduled payment.

Also, what’s a simple and legitimate matter of creditrisk ? Criminals have learned how to exploit situations in which fraud might — initially, but for a meaningful period of time — look like an issue of creditrisk, which can make so much of fraud prevention reactive, not proactive. Here’s a test: What’s fraud?

However, to get down to his concerns, the analyst said — per news reports such as CNBC — that the recently debuted “Square Installments” (which, as the name implies, offers payment plans) may expose the company in a way that makes it vulnerable to credit markets. Those are headline numbers. percent and personal loans by 13.2

Could tax liens and judgments soon be excluded from creditrisk calculations? Both have an impact on people’s credit scores, making it harder for some people to access credit. VantageScore removed all tax liens and civil judgments from a random sample of credit files from 4 million consumers in an analysis.

AI Also Helps Manage CreditRisk. For instance, Mastercard has been using AI to help its banking partners with creditrisk management, aiming to provide the right amount of credit to customers — and the smartest collections efforts — in today’s uncertain economic climate.

And in banking, financial institutions can incorporate artificial intelligence into their consumer credit strategies at a time when a retroactive approach to creditrisk management has become less feasible amid COVID-19. 12 : Number of months in advance AI systems can detect potentially fraudulent activity.

Those are the kind of numbers that explain why Zest received a $15 million investment last week from software developer Insight Partners. “On average, our customers will see a 20 percent lift in approvals and a 30 percent reduction in charge-offs just by deploying better math,” de Vere said. 15M In New Funding .

New data from insolvency firm Begbies Traynor may set off alarm bells: The number of U.K. A report released from the company this week found a 25 percent year-over-year increase in the number of companies categorized as being in significant financial distress in Q2, the largest yearly increase the firm has seen in three years, it said.

Some common market risks include: Interest rate risk Foreign exchange risk Raw materials cost risk (copper, steel, etc.) CreditRisksCreditrisk arises when customers or partners fail to meet their financial obligations.

With the rules, regulators are requiring Swiss banks to “[assign] a flat risk weight of 800 percent to cover market and creditrisks, regardless of whether the positions are held in the banking or trading book.” In addition, only 210 of the watches will be made, as only 21 million bitcoins will come to fruition.

The issues that have kept millennials out of the mortgage market tend to fall into three categories: lack of sufficient credit, lack of sufficient funds for a down payment or lack of a sufficiently long employment record to get lenders comfortable with them as a creditrisk.

The common perception has been that a “thin file or no file means poor creditrisk or subprime, when, in fact, it just means ‘no file,’” said Meloche. The common perception has been that a “thin file or no file means poor creditrisk or subprime, when, in fact, it just means ‘no file,’” said Meloche.

This episode underscores that data for targeted customer offerings can come from anywhere and is not necessarily the result of meticulous number crunching. When number crunching is needed, however, data analytics can help. “If the husband buys a truck, the wife’s going to want a new Volvo.”. Data Analytics Behind the Scenes.

Credit Key offers businesses an alternative payment solution intended to give financing for purchases at the point of sale. The company takes on the creditrisk and loan servicing, offering buyers a "transparent" experience with competitive interest rates, the report writes. The booming B2B market in the U.S. While only $1.3

The tie-up is an extension of a current relationship that will have Satago’s offering smoothly linked with Sage Accounting, which will offer clients automated invoice chasing, invoice finance and creditrisk analysis in a single system.

First-party fraud seems difficult to perpetrate because loan applications typically require identity verification with Social Security numbers, which enable banks to track down loan applicants who go off the grid. The bad actors then cut off all contact with the bank, preventing it from recouping its losses.

Buxton previously worked for cloud application monitoring platform Datadog as VP of finance, where he led the company to a $9 billion valuation and a current market capitalization of upwards of $25 billion, with the number of employees growing from 100 to 2,000 during his tenure, the release says.

Businesses face a tremendous number of uncertainties. It is a tall ask, considering that today’s macroeconomic risks can come from unexpected directions. "I Moody’s, he noted, is well known for its counterparty creditrisk analysis. And this list is only getting longer daily, with many uncertainties remaining persistent.

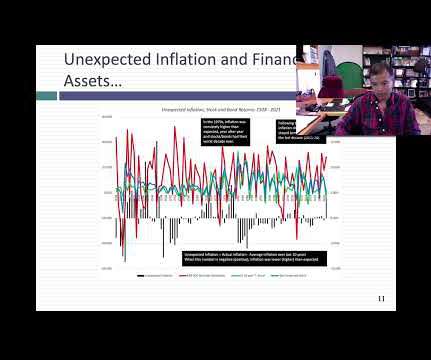

Inflation numbers have been coming in high now, for more than a year, but for much of the early part of 2021, bankers, investors and politicians seemed to be either in denial or casually dismissive of its potential for damage. 1.01)-1).

Instead, I’d like to get you thinking about the implications for payments, commerce and retail for a generation of 70 million that may be strong in number but weak in spending power. Besides that, they’re the ideal creditrisk and perfect target to stake the future of FinTech, payments and retail. MORE QUESTIONS THAN ANSWERS.

What happens when a good creditrisk goes bad? Think of management changes (or ousters), location changes, and even changes to telephone numbers – enough of these can add up to signal a business that is in flux, and is becoming, in fact, unstable or transient.

“The problem with that approach is that it misses the risk of customers who are financially able to pay but still do not,” she noted. But it’s not an impossible task for finance leaders, and the benefits to understanding their company’s cash flow can be considerable,” she said.

In an interview with Karen Webster, Chuck Fagan , president and CEO of PSCU , said the very model of the credit union can help members navigate the seismic shifts of a historic economic downturn spurred by the coronavirus. But these were isolated in terms of geography and the number of FIs that they hit.”.

Thin-file credit applicants could go through a fairly painstaking process to build credit with low-value cards, but that wasn’t a good answer for him. To date, Aire has aided in the underwriting of $10 billion of credit across various consumer credit categories.

Their combined impact will greatly influence actual insolvency numbers and trade creditrisk in 2021 and 2022, the firm added. The post Bankruptcies expected to increase 26% globally appeared first on FutureCFO.

Starting with one or two pieces of real information (a Social Security number is always one of them, sometimes paired with a real name), fraudsters take their time to slowly nurture a fake credit profile until it has a good enough record to make a big strike.

In fact, Srinivasan added, the parameters of risk itself are changing. He noted that, with real-time payments , creditrisk is largely negated, as transactions require immediate posting of debits and confirmation of sufficient funds — and it can be immediately ascertained whether or not user accounts are in good standing.

DSO as an accounting metric measures the average number of days a businesses receives payment for goods and services purchased on credit, while DIO is a working capital management ratio that measures the average number of days a company holds inventory before it’s turned into sales.

Inflation numbers have been coming in high now, for more than a year, but for much of the early part of 2021, bankers, investors and politicians seemed to be either in denial or casually dismissive of its potential for damage. 1.01)-1).

“Our partnership with the AICPA will enable the SBA Office of the National Ombudsman to further expand our reach to, and impact upon, an even greater number of CPAs who could benefit from our assistance,” added SBA Deputy National Ombudsman Mina Wales. The SBA and AICPA have been working together since 2008, the entities noted.

That tactic — cutting corners and pennies — shows a glaring disconnect in risk management, according to Taylor. He said banks pay a lot of attention to financial risk, spanning liquidity risk, creditrisk and overall exposure to different markets. Looking Ahead. They’ve also found cryptos a good place to hide.

Consumers are used to having any number of payment options on offer when they’re ready to push a buy button onscreen, at any time of day. For those firms seeking access to credit, lenders will often start with the SMB principal’s FICO score or tax returns from the past few years, which can be an inefficient barometer of creditrisk.

Doing that meant that Circle had to build out an AI-powered risk engine that allows it to make 90 percent of its risk and compliance decisions with machines rather than relying on compliance people. This allows Circle to take on the creditrisk of transactions to make money move instantly. Despite Venmo’s lead in the U.S.

have brought attention to the nation’s plight against late supplier payments, but a new report from Euler Hermes warns this is a global issue — one that is worsening and raising the insolvency risk. Regulators and analysts in the U.K.

The Asian Liquidity Stress Indicator (ALSI) climbed to its second weakest level, and the number of companies rated B3 and below continued to increase in the first quarter of 2020 following a surge of downgrades in Q1, said Moody's Investors Service. . The ALSI climbed to 38.7% in March from 32.9%

Only about half of small businesses, he said, have a credit profile or have a credit report on that business, with half of those, in turn, he noted, classified as “thin file” reports. In other words, there exists information on transactions that have been successfully hurdled to start operations, yet are not related to credit.

Whether it’s decisioning models used for fraud, creditrisk, customer operations or marketing, AaaS can be a powerful tool in helping a company address whatever it is trying to solve. Whether that decision flow is around marketing, creditrisk, customer operations and retention, etc., The “Buy Vs. Build” Decision.

The invoiced order payment process is in effect starting today, August 8, 2018, although it may take longer to receive your first invoiced order due to the limited number of Amazon Business buyers qualified for Pay by Invoice,” the company wrote in a letter to sellers, according to eCommerce Bytes. percent of the total invoiced amount.

Credit sales waned a bit this year, at least on the B2B side, as that activity was 37.4 Within that headline number, credit sales were off in Ireland by 7.2 All this points to deterioration of the worldwide outlook for trade creditrisk on the horizon. percent in the most recent reading, down from 38.8

Treasury’s Office of the Comptroller of the Currency found that underwriting standards have eased thanks to an increased appetite for creditrisk, increased competition and an overall perception of improved economic circumstances. Commercial real estate (CRE) loans, however, continued to strengthen. Amid these fluctuations, the U.S.

The three credit reporting agencies (Equifax, Experian and Equifax), under a program called the National Consumer Assistance Plan (NCAP) are looking for ways to improve their methods of collecting, reporting and updating data related to public records. consumers have both on their record.

They are a very low creditrisk — if a developer has an invoice from them, Qwil can be confident it is going to get paid. Our number one goal was offering something super simple with fees that are transparent and interest that is non-accruing,” Reinsch said.

A credit score, on the other hand, can and often will affect any and all of those things — plus a whole bunch of others, like whether one will be able to finance a car or rent an apartment. With the possible exception of a social security number, a credit score is really one of the more impactful set of digits in a consumer’s life.

The standard for removing that data will be failing to completely list important identifying information like a person’s name, address, social security number or date of birth. The change will apply to new tax lien and civil judgment data that are added to credit reports as well as existing data on the reports. “It’s

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content