This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Top 2024 macro-creditrisks include tight liquidity and funding conditions, uncertainty about China’s macroeconomic outlook and property sector, and geopolitical event risk, said Fitch Ratin gs recently. The post Top 2024 macro-creditrisks appeared first on FutureCFO.

When it comes to the main creditrisks, inflation and interest rates remain the most significant watch item for global credit, said Fitch Ratings recently. According to Fitch’s base-case forecasts, this will include a shallow recession in the US, limited growth in the eurozone and building risks to China’s recovery.

Notably, the work-from-home movement has resulted in a dramatic drop in office valuations that could lead to a whole host of issues, including lending constraints in the banking sector, which is already sitting on a mountain of unrealized losses on Treasuries and mortgages.

David Snyderman has put together an incredible career in fixed income, alternative credit, and really just an amazing way of looking at risk and trade structure and how to figure out probabilistic potential outcomes rather than playing the usual forecasting and macro tourist game. They have an incredible track record.

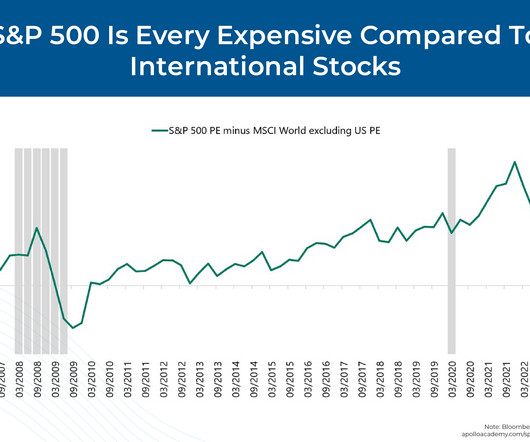

And you had to take on significant duration risk and creditrisk just to earn a couple percentage points. DAVIS: Where international equities, because of valuations, probably 7% to 7.5%. RITHOLTZ: So let’s talk about that, because that gap in valuation has persisted for a long time. RITHOLTZ: Right.

When you look at this present environment, do you think of yourselves more as bottom up credit pickers or, or do you look at the macro environment and say, Hey, we have to figure out what’s going on there? Also, 00:36:15 [Speaker Changed] You know, we’re bottoms up credit pickers. 00:37:26 [Speaker Changed] Huh.

But there are so many tools at your disposal, and let alone how much duration you’re taking, how much interest, how much creditrisk you’re taking, illiquidity, et cetera. And how do you make the decision, I’m not comfortable with this creditrisk relative to the return it’s going to throw off?

And up until that moment in time, we didn’t spend a lot of time on creditrisk in mortgages. We didn’t really have to model creditrisk because that was, that risk was taken by the agencies. But in these private labels, you had the, the market was taking the creditrisk.

And you know, it’s the same thing when valuation gets outta control too. It will come home to roost at some point, but doesn’t mean the valuation can’t get worse. Valuations are tight, they’re tight for a reason. You have to get compensated for each risk. Remember everybody forecasted it, right?

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content