This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I taught six different classes ranging from a corporatefinance class to undergraduates to a central banking for executive MBAs, and while I spent almost all of my time struggling to stay ahead of my students, with the material, it set me on a pathway to being a generalist.

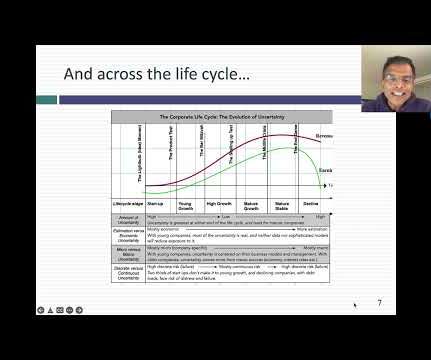

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. With declining businesses, facing shrinking revenues and margins, it is cash return or dividend policy that moves into the front seat.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Corporate Governance & Descriptive 1.

This week, we speak with Aswath Damodaran, who holds the Kerschner Family Chair in Finance Education at New York University’s Stern School of Business. A nine-time “Professor of the Year” winner at NYU, Damodaran teaches classes in corporatefinance and valuation to MBA students.

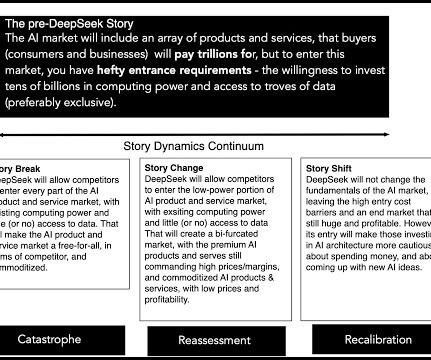

As the number of potential applications of AI proliferated, thus increasing the market for AI products and services, another part of the story was also being put into play. The AI Story, after DeepSeek I teach valuation, and have done so for close to forty years.

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. A few years ago, I wrote a paper for practitioners on the cost of capital , where I described the cost of capital as the Swiss Army knife of finance, because of its many uses.

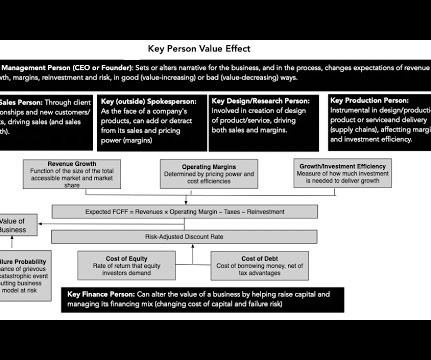

Of course, and with small businesses, especially those built around personal services (a doctor or plumber’s practice), it is part of the valuation process, where the key person is valued or at least priced and incorporated into valuation. To estimate key person value, there are three general approaches: 1.

If we think about it, a managerif facing pressure to beat an analyst forecast, or beat last years earnings, or wanting a particular bonushas enough flexibility in the accounting rules to manage those numbers while staying within the rules. You manage your numbers. So, how are we going to track the slippery slope? Horton: Heres one.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023. The class starts with a question of what the end game should be for a business (profitability, value, social good?)

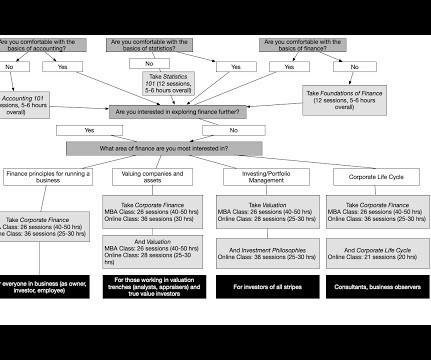

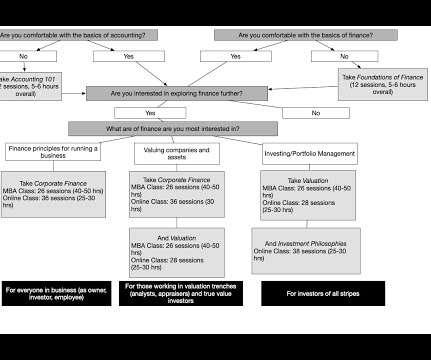

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online.

Corporatefinance experts say going public is cool this summer; that’s not the case for a billionaire hedge fund manager’s overhyped IPO. When valuations shift so drastically, it’s usually due to “a major event” or “a failed deal, or even a market correction,” Carl Niedbala, co-founder of risk management firm Founder Shield, said. “It’s

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023. The class starts with a question of what the end game should be for a business (profitability, value, social good?)

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online. The place to start is with accounting.

Another important aspect to consider within the discussed topic is how exactly FP&A is different from other finance disciplines, namely accounting, corporatefinance and financial control.

That skewing can affect valuation and pricing judgments about these firms, and correcting accounting inconsistencies is a key step towards leveling the playing field. Financing Expenses treated as Operating Expenses. When a financing expense is treated as an operating expense, that mistake plays out across the financial statements.

Last week, was my data week, where I download and analyze data on all publicly traded companies, listed anywhere in the world, and I will post extensively on what the numbers look like after a most tumultuous year. CorporateFinance : Corporatefinance is the development of the first financial principles that govern how to run a business.

US investors look toward European soccer and say, “There’s this amazing asset that has global appeal across Asia, the Middle East, South America … but how come their valuations don’t match that of an NFL team? Barlow: A number of portfolio companies are asked by their owners to move into exit mode at a rapid speed.

I am in the third week of the corporatefinance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet.

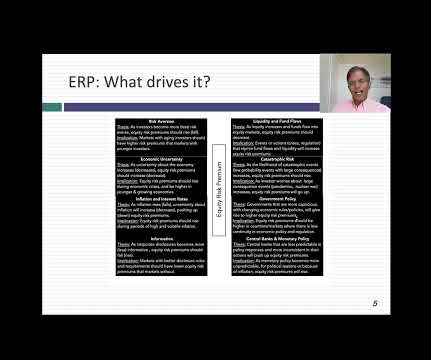

Adding to the confusion are the proliferation of very different numbers that you may have seen attached to the current equity risk premium, each usually quoting an expert in the field, but providing little context.

That skewing can affect valuation and pricing judgments about these firms, and correcting accounting inconsistencies is a key step towards leveling the playing field. Accounting 101 I am not an accountant, and have no desire to be one, but I have used their output (accounting statements) as raw material in valuation and corporatefinance.

Risk and Hurdle Rates In investing and corporatefinance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions.

Anglo’s valuation upside no longer looks compelling on a standalone basis,” JP Morgan’s equity research team concluded, suggesting it may still be a takeover target. The decision, which was intended to help Anglo focus on its restructuring, swung the company from a net profit of $1.26 The restructuring itself is a complicated affair.

Out of all the finance jobs available to college graduates, financial managers are some of the highest-paying, with high demand for workers in this field. Bureau of Labor Statistics, employment numbers for Financial Managers are expected to rise by 17% over the next decade , faster than the average for all occupations.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. The numbers yield interesting insights. . The proverbial bottom line for success in business is the capacity to deliver profits, at least in the long term.

Corporatefinance is breaking records with its M&A activity this year, thanks, in part, to rising cash reserves. And these are big numbers.”. According to reports, Apple has secured a valuation of about $800 billion, due in part to its cash reserves and other investments. You don’t know what the credit ratings are.

Risk and Hurdle Rates In investing and corporatefinance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporatefinance, this takes the form of a hurdle rate , a minimum acceptable return on an investment, for it to be funded.

The team led by Dolf Campman brought us a number of interesting opportunities, and in the case of XVR Simulation this resulted in the completion of an attractive acquisition. Their contribution to the execution of the transaction was also very helpful.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. The numbers yield interesting insights. The proverbial bottom line for success in business is the capacity to deliver profits, at least in the long term.

The number of European insurance deals increased from 106 in H1 2022 to 131 in H1 2023, accompanied by a fall in total deal value: from £7bn in H1 2022 to £4.2bn in H1 2023. European wealth and asset management deal numbers rose from 92 in H1 2022 to 126 in H1 2023.

Of course, we have the quarterly numbers, too, including insight into how American Express’ commercial card business is holding up. According to analysts, adjustments in Amex’s Global Commercial Services (GCS) strategy — including new small business services, FX tools and other corporatefinance products — helped bump up the numbers.

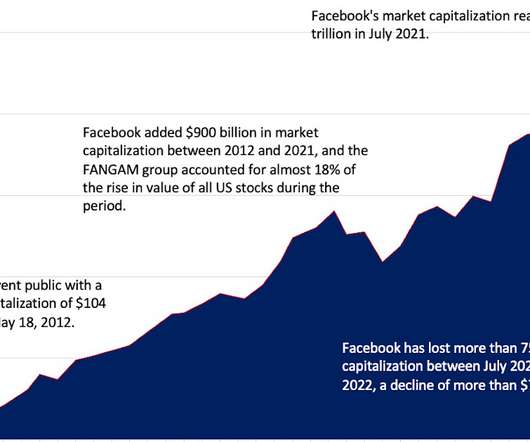

In the third and final post, I will argue that Facebook’s troubles with the market have as much to do with a failure of narrative, as they are about disappointing numbers, and present a template for what the company needs to do, to reclaim the high ground.

The tallies are in: Innovate Finance has calculated the state of investment in FinTech for 2015, and we have the numbers. Innovate Finance released The 2015 FinTech Investment Landscape this month, a report that offers a snapshot at how investors are placing their money among financial innovators.

In the third and final post, I will argue that Facebook's troubles with the market have as much to do with a failure of narrative, as they are about disappointing numbers, and present a template for what the company needs to do, to reclaim the high ground.

Read More “I just went down this rabbit hole where I was working weekends as a musician and doing studio work in the evenings,” explains Parsons, who adds that his weekend music tours would often book-end 70-hour workweeks in corporatefinance. “I I have not necessarily built my career by trying to fill niches and gaps on my c.v.,

Heather comes from with a fascinating background, having previously been in a number of other places, most notably Morningstar, and, and she has a very specific approach to investment management and thinking about stock selection. They do a number of things at Diamond Hill that many other investment shops don’t.

From a heightened use of mobile banking solutions, to more evidence of paper check abandonment, to the potential fiscal impact of the blockchain for banks, this week’s data was all about FIs and their corporate clients shaping the way money moves between firms. We break down all the numbers below. $1

ST: I’m reporting to the CEO and board of directors, providing leadership in all aspects of business and finance, including strategic planning, annual business plan, rolling forecast, financial management, treasury, regulatory reporting, internal controls, taxation, and procurement.

In my last post, I looked at equities in 2023, and argued that while they did well during 2023, the bounce back were uneven, with a few big winning companies and sectors, and a significant number of companies not partaking in the recovery.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. Mean reversion : I am not a knee-jerk believer in mean reversion, but the tendency for numbers to move back towards averages is a strong one.

It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporatefinance and valuation practice, in particular, and this post is my attempt to answer them all with one post. What is a risk free investment? Why does the risk-free rate matter?

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. In closing, I also want to dispense with the notion that data is objective and that numbers-focused people have no bias.

I went into what’s called corporatefinance, what people would see now as sort of M&A department. CHANCELLOR: Well, I was actually in a sort of subgroup there, which was called corporate strategy. But I didn’t last very long there because I thought I didn’t like corporatefinance.

RPA is igniting chatter in the corporatefinance community as professionals explore next-level analytics and automation functionality to enhance processes like accounts payable, accounts receivable, cash flow management and more. While Automation Anywhere’s funding was the largest of the week, its valuation is not the biggest.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content