This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

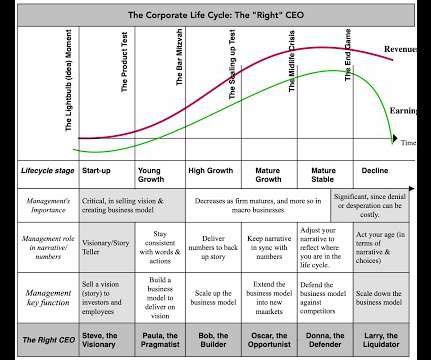

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. With declining businesses, facing shrinking revenues and margins, it is cash return or dividend policy that moves into the front seat.

I spend most of my time in the far less rarefied air of corporatefinance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value.

In 2006, Lam relocated to New York to lead KPMG’s global TMT corporatefinance team. Over two decades, he honed his expertise in mergers and acquisitions, valuation, and strategic advisory, collaborating with CFOs on transformative deals. It transforms how businesses operate, enabling greater productivity.

If you are not strong on ESG [environmental, social, and governance] priorities, it will be very difficult to finance your company in the future. A company’s valuation is now fundamentally connected to its CSR, and not only in terms of profitability.

I am in the third week of the corporatefinance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet. With operating margins, you are getting a handle on economies of scale.

That skewing can affect valuation and pricing judgments about these firms, and correcting accounting inconsistencies is a key step towards leveling the playing field. Financing expenses are expenses associated with the use of non-equity financing, and in most firms, it takes the form of interest expenses on debt, short term and long term. .

This includes the IPO of OYO, India’s most successful hospitality startup that is looking to raise $1 billion and Ola Electric, another venture backed start up manufacturing electric scooters, looking to raise approximately $600 million.

CorporateFinance : Corporatefinance is the development of the first financial principles that govern how to run a business. It is that mission that makes corporatefinance the ultimate big picture class, one that everyone (entrepreneurs, investors, analysts, business observers) should take.

That skewing can affect valuation and pricing judgments about these firms, and correcting accounting inconsistencies is a key step towards leveling the playing field. Accounting 101 I am not an accountant, and have no desire to be one, but I have used their output (accounting statements) as raw material in valuation and corporatefinance.

Manufacturing shows promising signs of recovery while nearshoring and friendshoring in new markets are becoming stronger trends. The agency recorded a decline in international investment project announcements, particularly in project finance (21%) and mergers and acquisitions (16%). At an estimated $1.37

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. The proverbial bottom line for success in business is the capacity to deliver profits, at least in the long term.

I have written about the firm many times, over that period, starting with a valuation that I did of the company in 2012, just ahead of it going public. In these companies, as an outside investor, you have to build that reality into your valuations, leading to discounts to your value that reflect how much you trust management.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. The proverbial bottom line for success in business is the capacity to deliver profits, at least in the long term.

I have written about the firm many times, over that period, starting with a valuation that I did of the company in 2012, just ahead of it going public. In these companies, as an outside investor, you have to build that reality into your valuations, leading to discounts to your value that reflect how much you trust management.

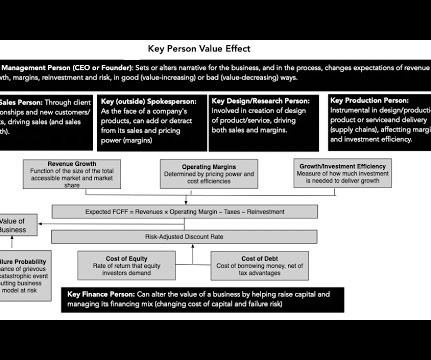

Of course, and with small businesses, especially those built around personal services (a doctor or plumber’s practice), it is part of the valuation process, where the key person is valued or at least priced and incorporated into valuation. To estimate key person value, there are three general approaches: 1.

Country Risk in Business Most corporatefinance classes and textbooks leave students with the proposition that the right hurdle rate to use in assessing business investments is the cost of capital, but create a host of confusion about what exactly that cost of capital measures.

It all gives a very corporatefinance addition to my macroeconomic thinking. And that was and continues to be the main significant attraction that I find so exciting about my job naming that is combining the macro world with the corporatefinance and the deal team world in private credit and private equity.

High interest rates were an issue; steep borrowing costs and lower returns created valuation mismatches, ultimately reducing the size, scope, and appeal of private equity deals. Valuation gaps narrowed and more deals were completed, but it wasnt a full rebound to pre-slowdown levels. The leverage was quite challenging, Dermarkar notes.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content