This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

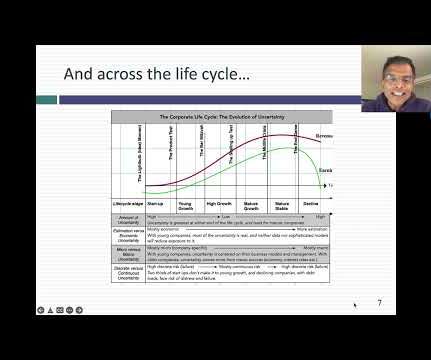

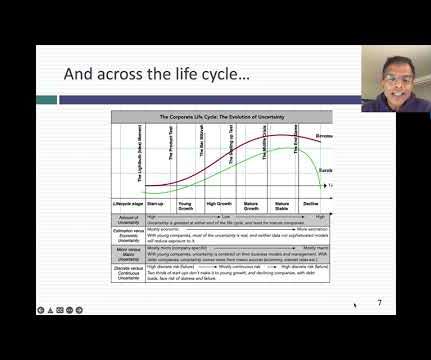

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. With declining businesses, facing shrinking revenues and margins, it is cash return or dividend policy that moves into the front seat.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth.

I spend most of my time in the far less rarefied air of corporatefinance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value.

The key benefit of Benfords law is that it doesnt matter what kind of firm it ispublic, private, what accounting policies it follows, what currency it operates in, whether its loss-making, whether its a growth company, highly leveraged or no leverage at allmakes absolutely no difference. Horton: Heres one.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing.

The growing variety and complexity of tasks within the finance function has resulted in the creation of a discipline that is supposed to become a bridge between the finance and business to support decision-making process by leveraging data and technology. This relates to FP&A which stands for financial planning and analysis.

The year 2024 brings a landscape of unprecedented challenges and opportunities for corporate treasurers. From the ongoing global conflicts to the lingering effects of high inflation, corporatefinance professionals are gearing up to navigate an environment marked by volatility and uncertainty.

Resilience, coupled with some slightly sunnier macroeconomic conditions, suggests that M&As and initial public offerings (IPOs) in 2025 could maintain momentumdespite certain aspects of corporatefinance currently being on the downtrend. The top five IPOs by valuation in 2024 were Lineage on the Nasdaq ($5.1

409A / ValuationsLeveraging our expertise and industry knowledge, we will conduct thorough assessments to determine the fair market value of your company, ensuring compliance with regulations and helping you make informed decisions related to stock options, equity compensation, and financial reporting.

Those that closed a deal often paid way too much, or at least passed the companies along to public markets at inflated valuations. Higher interest rates have cut the global total of initial public offerings nearly in half since 2021, reducing targets’ leverage on valuation. billion “merger” with Churchill Capital Corp.

I am in the third week of the corporatefinance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet.

We discuss how his career has traced the rise of private credit: He began his career in the Mergers & Acquisitions Group at Drexel Burnham Lambert, then founded the high-yield finance business at Chase Securities (now JP Morgan Chase), served as head of LeveragedFinance for RBC. class nine times.

Anglo’s valuation upside no longer looks compelling on a standalone basis,” JP Morgan’s equity research team concluded, suggesting it may still be a takeover target. The decision, which was intended to help Anglo focus on its restructuring, swung the company from a net profit of $1.26 The restructuring itself is a complicated affair.

It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. Thus, without a sense of what comprises a high or low profit margin for a firm, or what the cost of capital is for the typical company, it is easy to create "fairy tale" valuations and analyses.

Risk and Hurdle Rates In investing and corporatefinance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporatefinance, this takes the form of a hurdle rate , a minimum acceptable return on an investment, for it to be funded.

“Monitoring the size and growth of crypto-asset markets is critical to understanding the potential size of wealth effects, should valuations fall,” the FSB said in a statement, reported Reuters.

Risk and Hurdle Rates In investing and corporatefinance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporatefinance, this takes the form of a hurdle rate , a minimum acceptable return on an investment, for it to be funded.

Heather Brilliant : I worked at Bank of America and, and they had a wonderful corporatefinance training program. But there’s always gotta be some element of the valuation really being compelling. But maybe second to valuation as a primary consideration. Barry Ritholtz: Huh, really, really interesting.

Panelist – Jim Briggs, Director, Statesman CorporateFinance | jbriggs@statesmanbiz.com. Unless it is a simple, small business, the valuation of the business can be complicated. Engaging valuation expertise is a good way to pave the path to success. Demonstrating sustainable value to an outsider (i.e.,

I went into what’s called corporatefinance, what people would see now as sort of M&A department. CHANCELLOR: Well, I was actually in a sort of subgroup there, which was called corporate strategy. But I didn’t last very long there because I thought I didn’t like corporatefinance.

By leveraging existing expertise and portfolio assets, investors see opportunities to optimize sponsorship deals and naming rights and create synergies that add value. In January, Texas-based Presidio Investors swooped in to acquire Hellas Verona FC at a reported 130 million valuation.

High interest rates were an issue; steep borrowing costs and lower returns created valuation mismatches, ultimately reducing the size, scope, and appeal of private equity deals. The leverage was quite challenging, Dermarkar notes.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content