This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I spend most of my time in the far less rarefied air of corporatefinance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. In this role, the cost of capital is an opportunity cost, measuring returns you can earn on investments on equivalent risk.

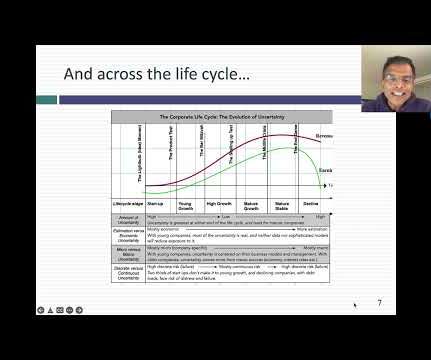

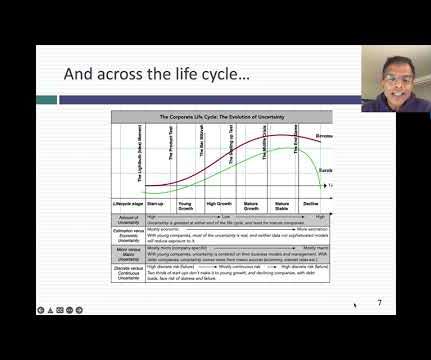

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Tech companies age in dog years, and the consequences for how we manage, value and invest in them are profound.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Return on (invested) capital 2.

In fact, almost every investment scam in history, from the South Sea Bubble to Bernie Madoff, has offered investors the alluring combination of great opportunities with no or low danger, and induced by sweet talk, but made blind by greed, thousands have fallen prey. Let me use two illustrations to bring this home.

I am in the third week of the corporatefinance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. What is a risk free investment?

In fact, almost every investment scam in history, from the South Sea Bubble to Bernie Madoff, has offered investors the alluring combination of great opportunities with no or low danger, and induced by sweet talk, but made blind by greed, thousands have fallen prey. Let me use two illustrations to bring this home.

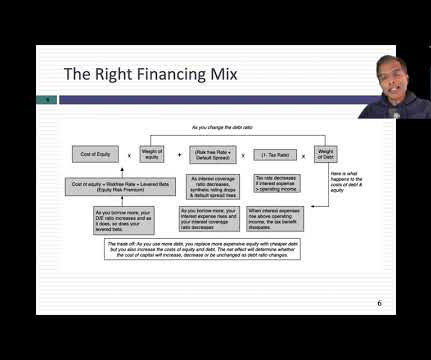

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income. Returns on Invested Capital (or Equity).

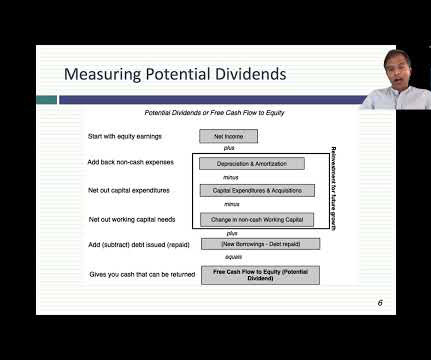

It also follows that the investment, financing, and dividend decisions , at most firms, are interconnected, since for any given set of investments, borrowing more money will free up more cash flows to return to shareholders, and for any given financing, investing more back into the business will leave less in returnable cash flows.

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporatefinance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

That said, to use mean reversion in analysis or investing, you need to know what these averages are, either over time or across companies, and data can help in that pursuit. . Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing.

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income.

In pursuit of an answer to that question, I used company-specific data from Value Line, one of the earliest entrants into the investment data business, to compute an industry average. Return on (invested) capital 2. Ratings & Spreads 2. Tax rates 4. Excess Returns on investments 4. Financing Flows 5.

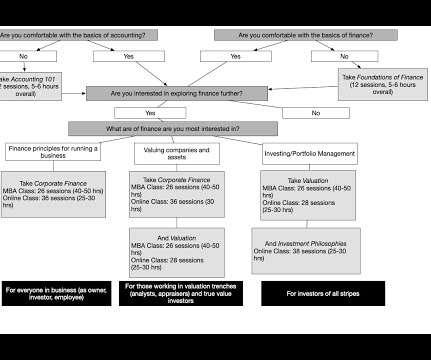

CorporateFinance : Corporatefinance is the development of the first financial principles that govern how to run a business. It is that mission that makes corporatefinance the ultimate big picture class, one that everyone (entrepreneurs, investors, analysts, business observers) should take.

That said, to use mean reversion in analysis or investing, you need to know what these averages are, either over time or across companies, and data can help in that pursuit. Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. Return on Invested Capital 2.

. “ Global Corporate Banking 2016: The Next-Generation Corporate Bank ” found that less than a third of corporate banking divisions across North America and Asia, and less than half in Europe, experienced “positive and growing economic profit” between 2013 and 2015. ”

Put simply, I possess no exclusivity here, and staying consistent with my thesis, I don't expect to expect to make money by investing based upon this data. The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporatefinance or valuation issues. So, why bother?

Debt's place in business To understand debt's role in a business, I will start with a big picture perspective, where you break a business down into assets-in-place, i.e., the value of investments it has already made and growth assets, the value of investments you expect it to make in the future.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. According to Chancellor, interest is the single most important feature of finance, both ancient and modern.

In this post, I look at risk, a central theme in finance and investing, but one that is surprisingly misunderstood and misconstrued. Risk Measures There is almost no conversation or discussion that you can have about business or investing, where risk is not a part of that discussion. What is risk?

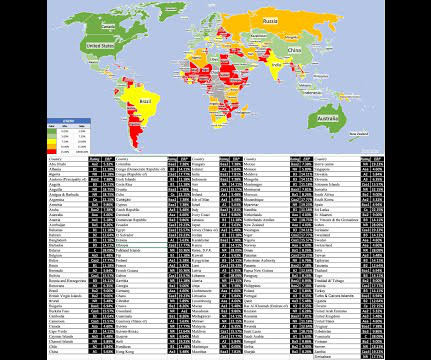

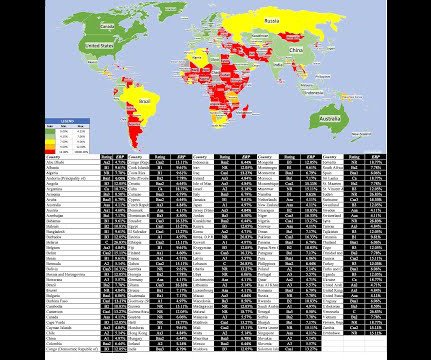

Country Risk: Determinants At the risk of stating the obvious, investing and operating in some countries is much riskier than investing and operating in others, with variations in risk on multiple dimensions. Political Structure Would you rather invest/operate in a democracy than in an autocracy?

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content