This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

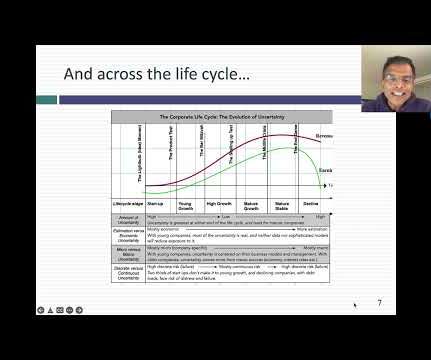

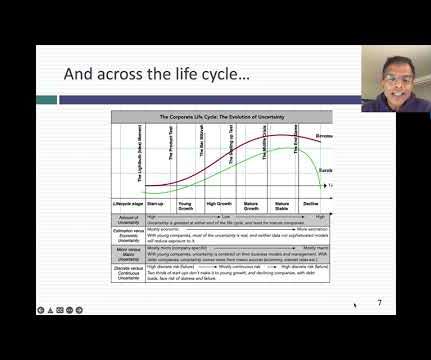

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Financing Flows 5. Beta & Risk 1.

Risk and HurdleRates In investing and corporatefinance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. Not surprisingly, both these forces play a role in how companies and investors set hurdlerates.

Risk and HurdleRates In investing and corporatefinance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. Not surprisingly, both these forces play a role in how companies and investors set hurdlerates.

I am in the third week of the corporatefinance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks!

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. In the three posts that follow, I will look at the shifts in corporatehurdlerates (in post 6), debt loads and worries (in post 7) and dividends/cash returned in post 8.

In my last post, I noted the decline in costs of capital for firms over time, noting that the median cost of capital at the start of 2022 is only 6.33%, across global firms, and argued that companies that demand double-digit hurdlerates risk being shut out of investments.

The Dysfunctional Version In practice, though, there is no other aspect of corporatefinance that is more dysfunctional than the cash return or dividend decision, partly because the latter (dividends) has acquired characteristics that get in the way of adopting a rational policy. Data Update 5 for 2025: It's a small world, after all!

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporatefinance and valuation practice, in particular, and this post is my attempt to answer them all with one post. Why does the risk-free rate matter? What is a risk free investment?

In my last post, I noted the decline in costs of capital for firms over time, noting that the median cost of capital at the start of 2022 is only 6.33%, across global firms, and argued that companies that demand double-digit hurdlerates risk being shut out of investments.

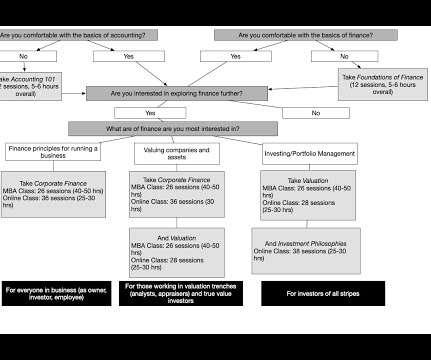

CorporateFinance : Corporatefinance is the development of the first financial principles that govern how to run a business. It is that mission that makes corporatefinance the ultimate big picture class, one that everyone (entrepreneurs, investors, analysts, business observers) should take.

In my corporatefinance class, I describe all decisions that companies make as falling into one of three buckets – investing decisions, financing decision and dividend decisions. Tax rates 4. Financing Flows 5. Insider, CEO & Institutional holdings 2. Aggregate operating numbers 3. Beta & Risk 1.

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. The second is that in my line of work, which is corporatefinance and valuation, the numbers I need lie in micro or company-level data, not in the macro space.

. “ Global Corporate Banking 2016: The Next-Generation Corporate Bank ” found that less than a third of corporate banking divisions across North America and Asia, and less than half in Europe, experienced “positive and growing economic profit” between 2013 and 2015.

The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporatefinance or valuation issues. If you use it at their jobs as corporatefinance or equity analysts, I am glad to take some of that burden off you, and I hope that you find more enjoyable uses for the time you save.

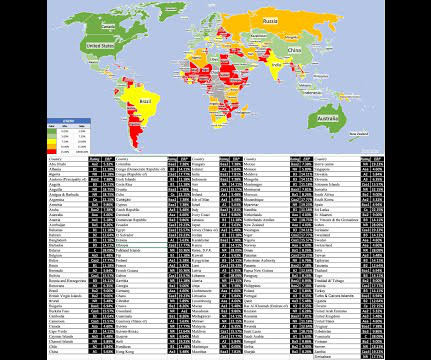

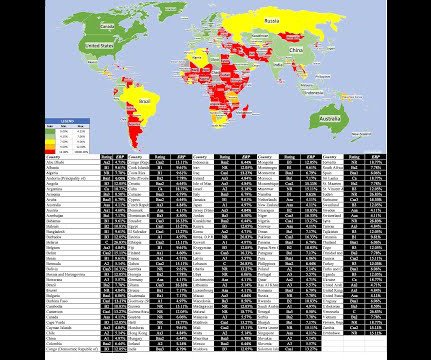

In particular, there are wide variations in how risk is measured, and once measured, across companies and countries, and those variations can lead to differences in expected returns and hurdlerates, central to both corporatefinance and investing judgments. What's coming?

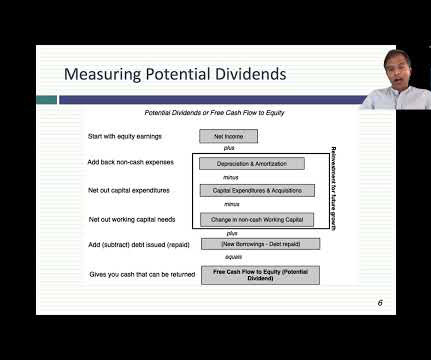

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporatefinance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

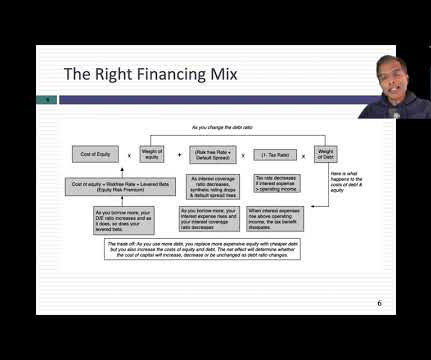

If you have taken a corporatefinance class sometime in your past life are probably wondering how this approach reconciles with the Miller-Modigliani theorem, a key component of most corporatefinance classes, which posits that there is no optimal debt ratio, and that the debt mix does not affect the value of a business.

I went into what’s called corporatefinance, what people would see now as sort of M&A department. CHANCELLOR: Well, I was actually in a sort of subgroup there, which was called corporate strategy. But I didn’t last very long there because I thought I didn’t like corporatefinance.

Country Risk in Business Most corporatefinance classes and textbooks leave students with the proposition that the right hurdlerate to use in assessing business investments is the cost of capital, but create a host of confusion about what exactly that cost of capital measures.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content