This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Financing Flows 5. Beta & Risk 1.

That expected devaluation in the high-inflation currency is not risk, though, since it can and should be incorporated into your forecasts. If a firm is badly managed, and you expect it to remain badly managed, you can and should build in that expectation into your forecasts of that company’s earnings and value.

That expected devaluation in the high-inflation currency is not risk, though, since it can and should be incorporated into your forecasts. If a firm is badly managed, and you expect it to remain badly managed, you can and should build in that expectation into your forecasts of that company's earnings and value.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporatefinance and valuation practice, in particular, and this post is my attempt to answer them all with one post. Why does the risk-free rate matter? What is a risk free investment?

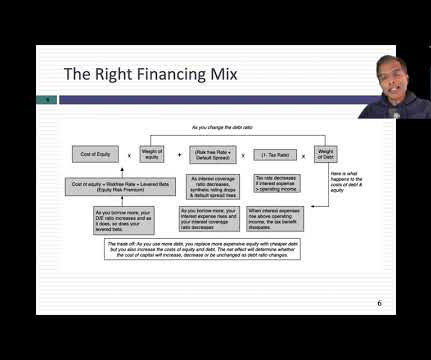

If you have taken a corporatefinance class sometime in your past life are probably wondering how this approach reconciles with the Miller-Modigliani theorem, a key component of most corporatefinance classes, which posits that there is no optimal debt ratio, and that the debt mix does not affect the value of a business.

The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporatefinance or valuation issues. I also report estimates of the default spreads based upon current yields on bonds in different ratings classes and the current riskfree rate.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content