This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I taught six different classes ranging from a corporatefinance class to undergraduates to a central banking for executive MBAs, and while I spent almost all of my time struggling to stay ahead of my students, with the material, it set me on a pathway to being a generalist.

I spend most of my time in the far less rarefied air of corporatefinance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023.

The six classes that I prepped for in those two years ranged from banking to investments to corporatefinance, and while I have never worked harder, much of what I teach today came out of those classes. In 1984, I moved on to the University of California at Berkeley, as a visiting lecturer, teaching anything that needed to be taught.

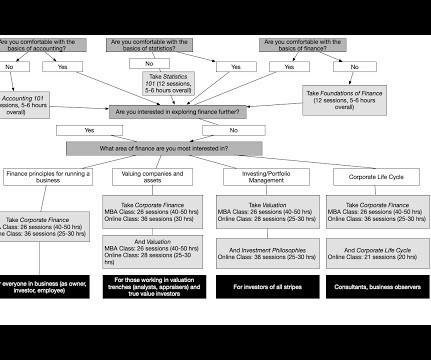

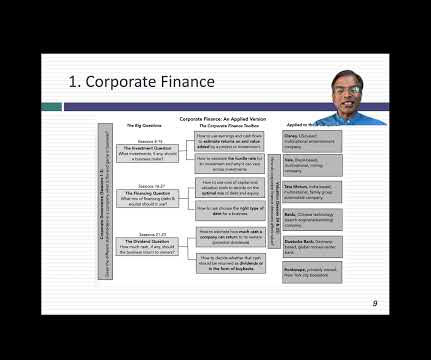

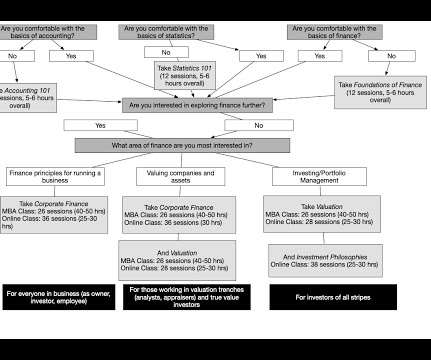

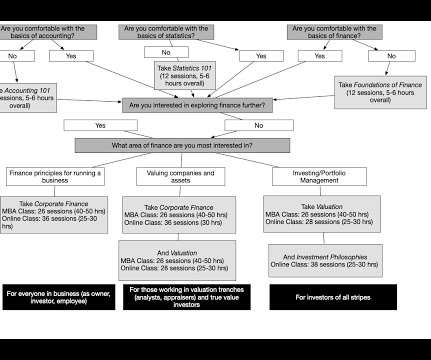

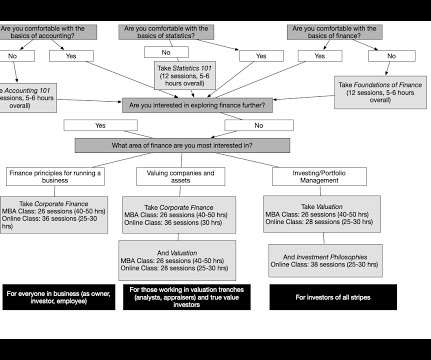

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporatefinancialanalysis or valuation was a chore. Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing.

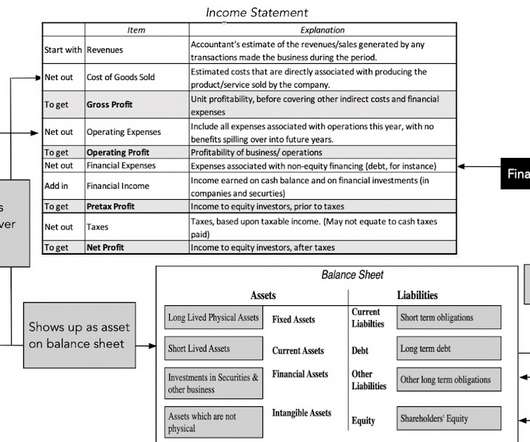

Planning, budgeting and forecasting are linked together forming financial planning processes. Financialanalysis is a type of economic analysis based on the financial data and focused on the assessment of stability and evaluation of profitability of a company, business or project.

A few of these variables are macro variables, but only those that I find useful in corporatefinance and valuation, and not easily accessible in public data bases. Rather than replicate that data, my macroeconomic datasets relate to four key variables that I use in corporatefinance and valuation.

That year, I computed these industry-level statistics for five variables that I found myself using repeatedly in my valuations, and once I had them, I could not think of a good reason to keep them secret. Financing Flows 5. Valuation Pricing Growth & Reinvestment Profitability Risk Multiple s 1.

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online.

A few of these variables are macro variables, but only those that I find useful in corporatefinance and valuation, and not easily accessible in public data bases. Rather than replicate that data, my macroeconomic datasets relate to four key variables that I use in corporatefinance and valuation.

It is perhaps a reflection of my age that I remember when getting data to do corporatefinancialanalysis or valuation was a chore. Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. Data: Trickle to a Flood!

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporatefinance and valuation practice, in particular, and this post is my attempt to answer them all with one post. What is a risk free investment? Why does the risk-free rate matter?

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. It is very likely that these rules of thumb were developed from data and observation, but at a different point in time.

ST: I’m reporting to the CEO and board of directors, providing leadership in all aspects of business and finance, including strategic planning, annual business plan, rolling forecast, financial management, treasury, regulatory reporting, internal controls, taxation, and procurement.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content