This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I like to make a difference : I do not expect my students to agree with all or even much of what I have to say, but I would like to think that I sometimes change the way they think about finance, and perhaps even affect their choice of professions. to the transactional (how much of my business should I give up for a capital infusion?)

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. With declining businesses, facing shrinking revenues and margins, it is cash return or dividend policy that moves into the front seat.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Financing Flows 5. Beta & Risk 1.

This week, we speak with Aswath Damodaran, who holds the Kerschner Family Chair in Finance Education at New York University’s Stern School of Business. A nine-time “Professor of the Year” winner at NYU, Damodaran teaches classes in corporatefinance and valuation to MBA students.

I spend most of my time in the far less rarefied air of corporatefinance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. In this role, the cost of capital is an opportunity cost, measuring returns you can earn on investments on equivalent risk.

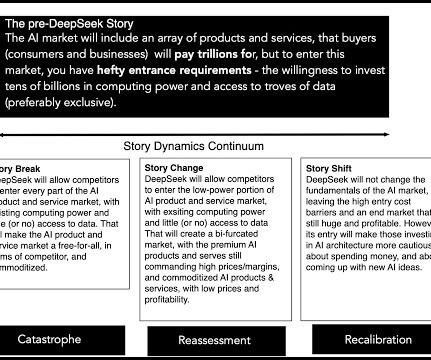

Nvidia market share: In my valuation, I assumed that Nvidia's lead in the AI chip business would give the company a head start, as the business grew, and to the extent that demand is sticky (i.e., The AI Story, after DeepSeek I teach valuation, and have done so for close to forty years.

The six classes that I prepped for in those two years ranged from banking to investments to corporatefinance, and while I have never worked harder, much of what I teach today came out of those classes. In 1984, I moved on to the University of California at Berkeley, as a visiting lecturer, teaching anything that needed to be taught.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023. The class starts with a question of what the end game should be for a business (profitability, value, social good?)

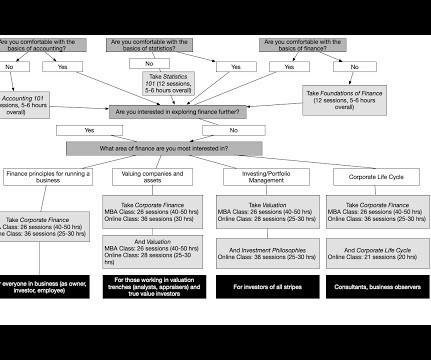

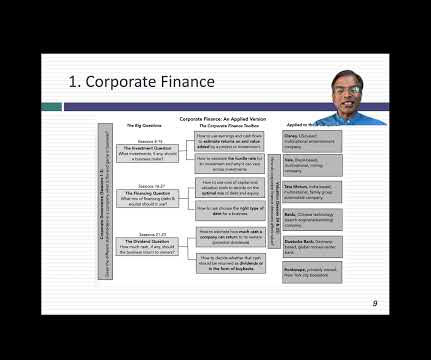

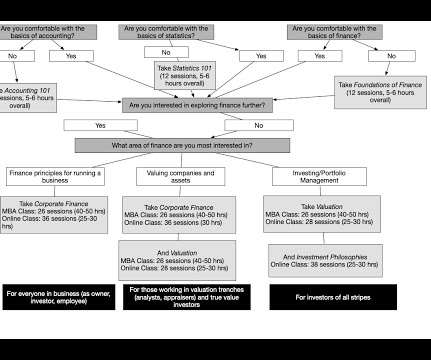

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online.

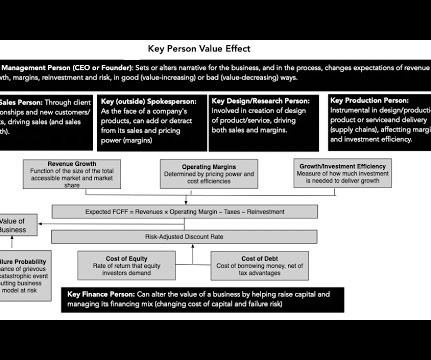

Of course, and with small businesses, especially those built around personal services (a doctor or plumber’s practice), it is part of the valuation process, where the key person is valued or at least priced and incorporated into valuation. To estimate key person value, there are three general approaches: 1.

Corporatefinance experts say going public is cool this summer; that’s not the case for a billionaire hedge fund manager’s overhyped IPO. When valuations shift so drastically, it’s usually due to “a major event” or “a failed deal, or even a market correction,” Carl Niedbala, co-founder of risk management firm Founder Shield, said. “It’s

FCF Fox CorporateFinance GmbH is delighted to publish the new FCF Valuation Monitor Q4 2024. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

What is the Tao of CorporateFinance? As McKinsey senior partner and Valuation author Tim Koller tells us, it is a formula that represents everything there is to know about finance. If you remember it, you can bring to mind the key drivers to consider when thinking about the valuation of a company.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporatefinance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023. The class starts with a question of what the end game should be for a business (profitability, value, social good?)

One industry that tends to be recession-resistant is finance. And while the finance industry has seen its share of ups and downs over the years, it generally bounces back fairly quickly after a downturn. If you’re considering a career in finance, you’re probably wondering what the best-paying jobs are. Chief Financial Officer.

Global Finance: Can you briefly describe what your model does? Their initial response was to increase their human intervention in 2008: They changed their inventory valuation assumption, their revenue recognition assumptions, and a few other things. Joanne Horton: Yes. Whats the likelihood that fraud will take place in the future?

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q4 2023”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q1 2024”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q3 2023”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q2 2023”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q1 2023”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q4 2022”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q3 2022”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q2 2022”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q1 2022”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – February 2022”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

FCF Fox CorporateFinance GmbH is delighted to publish the new “FCF Valuation Monitor – Q4 2021”. The FCF Valuation Monitor is a comprehensive valuation analysis for the German small / midcap market segment and.

Its valuation has also fluctuated, peaking at $46 billion in 2021 before rapidly declining to $6.7 The post Klarna IPO Could Redefine Payments Market appeared first on Global Finance Magazine. The Stockholm-based firm has applied to list its shares on the NYSE. The price range of the IPO has yet to be finalized. billion two years ago.

( BBC ) Be sure to check out our Masters in Business next week with Aswath Damodaran, Professor of Finance at New York University’s Stern School of Business. His textbook “ Investment Valuation ” is the standard in the field. class nine times.

Data: Trickle to a Flood! It is perhaps a reflection of my age that I remember when getting data to do corporate financial analysis or valuation was a chore. Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing.

The growing variety and complexity of tasks within the finance function has resulted in the creation of a discipline that is supposed to become a bridge between the finance and business to support decision-making process by leveraging data and technology. This relates to FP&A which stands for financial planning and analysis.

That said, it is my experience with markets that has also made me skeptical about the over selling of both notions, since we have an entire branch of finance (behavioral finance/economics) that has developed to explain how more data does not always lead to better decisions and why crowds can often be collectively wrong.

In 2006, Lam relocated to New York to lead KPMG’s global TMT corporatefinance team. Over two decades, he honed his expertise in mergers and acquisitions, valuation, and strategic advisory, collaborating with CFOs on transformative deals.

409A / Valuations Leveraging our expertise and industry knowledge, we will conduct thorough assessments to determine the fair market value of your company, ensuring compliance with regulations and helping you make informed decisions related to stock options, equity compensation, and financial reporting.

Stockholm-based Klarna is believed to have a valuation of about $20 billion in advance of the IPO. Its status as a rising star in Europe’s fintech firmament took it to a valuation of $31 billion in March 2021, increasing to $45.6 The post Klarna Considers Share Sale Ahead Of Listing In US appeared first on Global Finance Magazine.

billion, according to a study by Houlihan Lokey, a leading valuation authority. The post Crickets T20 Gold Rush: Investors Building A Global Sports Empire appeared first on Global Finance Magazine. As of 2024, the IPLs total value is $16.4 With its broadcast rights selling for $6.02

During my teaching lifetime, I have taught a wide swath of classes, ranging from banking to equity instruments, but in the last twenty years, my focus has been on three classes, c orporate finance, valuation and investment philosophies , with the last one taught only online. The place to start is with accounting.

Global Finance: What has been the most challenging time of the 10 years you have been CFO at Groupe Berkem? After that, it was easier to build a financial strategy and to achieve acquisitions and finance the capex. Labrugnas: Today, the financial system is very focused on the topic of corporate social responsibility, or CSR.

That said, it is my experience with markets that has also made me skeptical about the over selling of both notions, since we have an entire branch of finance (behavioral finance/economics) that has developed to explain how more data does not always lead to better decisions and why crowds can often be collectively wrong.

That year, I computed these industry-level statistics for five variables that I found myself using repeatedly in my valuations, and once I had them, I could not think of a good reason to keep them secret. After all, I had no plans on becoming a data service, and making them available to others cost me absolutely nothing. Beta & Risk 1.

Those that closed a deal often paid way too much, or at least passed the companies along to public markets at inflated valuations. Higher interest rates have cut the global total of initial public offerings nearly in half since 2021, reducing targets’ leverage on valuation. Shares in electric vehicle maker Lucid Motors, whose $4.4

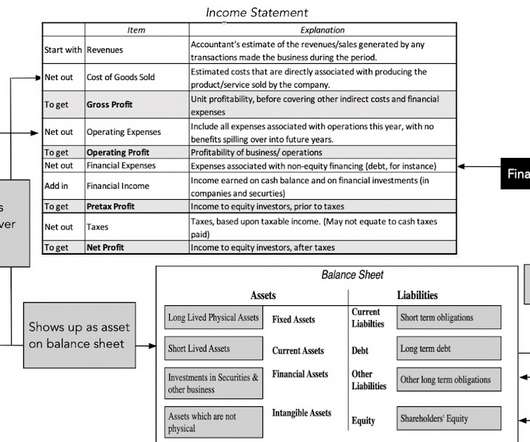

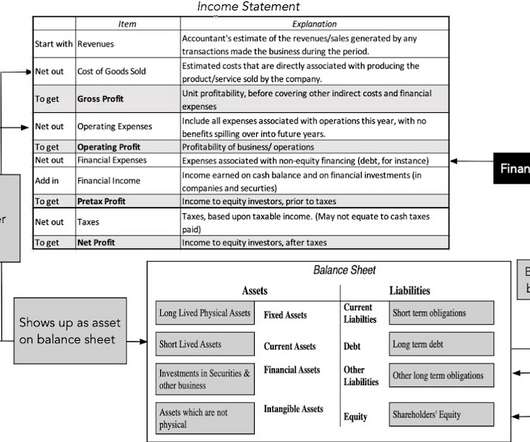

That skewing can affect valuation and pricing judgments about these firms, and correcting accounting inconsistencies is a key step towards leveling the playing field. Financing expenses are expenses associated with the use of non-equity financing, and in most firms, it takes the form of interest expenses on debt, short term and long term. .

Valuations today are more grounded in reality,” said Ritter. The post US IPO Market Picks Up Steam As Election Looms appeared first on Global Finance Magazine. While displaying some green shoots, the IPO market remains selective, and not all companies are finding success. before his title.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content