This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

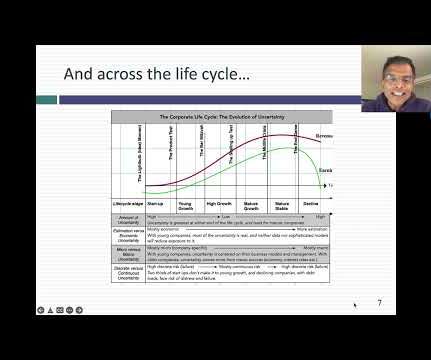

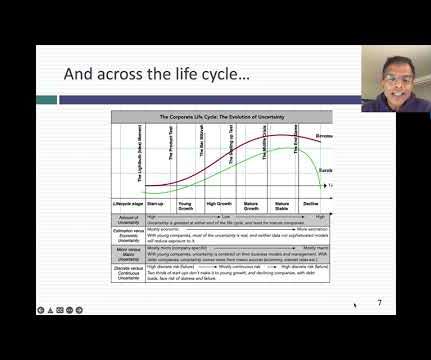

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

In corporatefinance and investing, which are areas that I work in, I find myself doing double takes as I listen to politicians, market experts and economists making statements about company and market behavior that are fairy tales, and data is often my weapon for discerning the truth. Tax rates 4. Financing Flows 5.

In the four decades that I have been teaching finance, I have always started my discussion of risk with a Chinese symbols for crisis, as a combination of danger plus opportunity: Over the decades, though, I have been corrected dozens of times on how the symbols should be written, with each correction being challenged by a new reader.

I am in the third week of the corporatefinance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks!

In the four decades that I have been teaching finance, I have always started my discussion of risk with a Chinese symbols for crisis, as a combination of danger plus opportunity: Over the decades, though, I have been corrected dozens of times on how the symbols should be written, with each correction being challenged by a new reader.

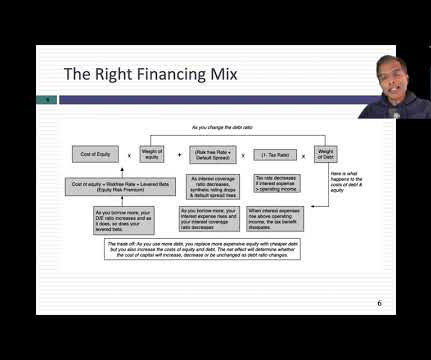

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

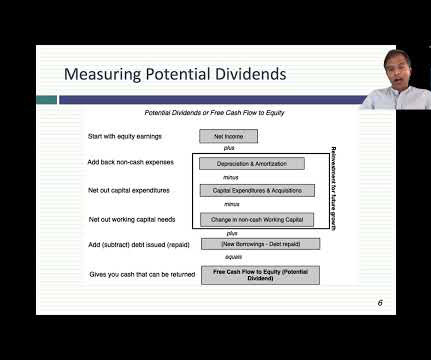

It also follows that the investment, financing, and dividend decisions , at most firms, are interconnected, since for any given set of investments, borrowing more money will free up more cash flows to return to shareholders, and for any given financing, investing more back into the business will leave less in returnable cash flows.

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. Finance but also from a variety of online data services that are affordable and very well done. . Or, do US companies pay far less in taxes than companies incorporated in the rest of the world?

This is the last of my data update posts for 2023, and in this one, I will focus on dividends and buybacks, perhaps the most most misunderstood and misplayed element of corporatefinance. Viewed in that context, dividends as just as integral to a business, as the investing and financing decisions.

In my last post, I noted the decline in costs of capital for firms over time, noting that the median cost of capital at the start of 2022 is only 6.33%, across global firms, and argued that companies that demand double-digit hurdlerates risk being shut out of investments.

In every introductory finance class, you begin with the notion of a risk-free investment, and the rate on that investment becomes the base on which you build, to get to expected returns on risky assets and investments. Why does the risk-free rate matter? and the reverse will occur, when risk-free rates drop.

I have also developed a practice in the last decade of spending much of January exploring what the data tells us, and does not tell us, about the investing, financing and dividend choices that companies made during the most recent year. Tax rates 4. Financing Flows 5. Insider, CEO & Institutional holdings 2. Debt Details 1.

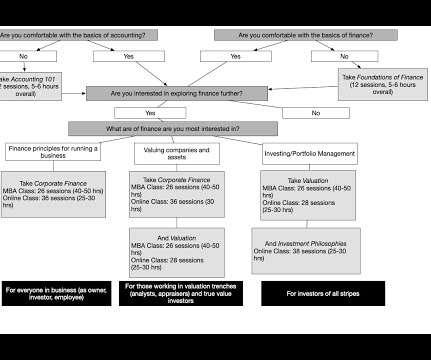

CorporateFinance : Corporatefinance is the development of the first financial principles that govern how to run a business. It is that mission that makes corporatefinance the ultimate big picture class, one that everyone (entrepreneurs, investors, analysts, business observers) should take.

In my last post, I noted the decline in costs of capital for firms over time, noting that the median cost of capital at the start of 2022 is only 6.33%, across global firms, and argued that companies that demand double-digit hurdlerates risk being shut out of investments.

Check rules of thumb : Investing and corporatefinance are full of rules of thumb, many of long standing. The second is that in my line of work, which is corporatefinance and valuation, the numbers I need lie in micro or company-level data, not in the macro space. Cap Ex & Net Cap Ex ((including acquisitons) 2.

. “ Global Corporate Banking 2016: The Next-Generation Corporate Bank ” found that less than a third of corporate banking divisions across North America and Asia, and less than half in Europe, experienced “positive and growing economic profit” between 2013 and 2015.

The second is that borrowing money will increase perceived default risk, and if the company is rated, lower ratings, and that too is true, but borrowing money at a BBB rating, with the tax benefit incorporated, might still yield a lower cost of funding that staying at a AA rating, with no debt in use.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. According to Chancellor, interest is the single most important feature of finance, both ancient and modern.

The first is that I do not have a macro focus, and my interests in macro variables occur only in the context of corporatefinance or valuation issues. If you use it at their jobs as corporatefinance or equity analysts, I am glad to take some of that burden off you, and I hope that you find more enjoyable uses for the time you save.

In this post, I look at risk, a central theme in finance and investing, but one that is surprisingly misunderstood and misconstrued. I do believe that, in finance, we have significant advances in understanding what risk, I also think that as a discipline, finance has missed the mark on risk, in three ways. What is risk?

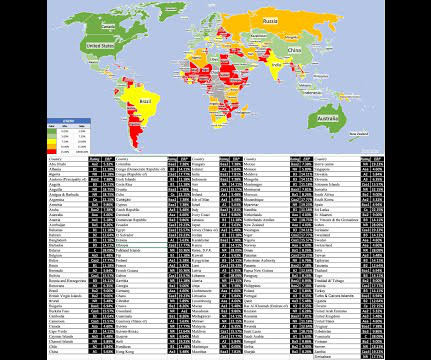

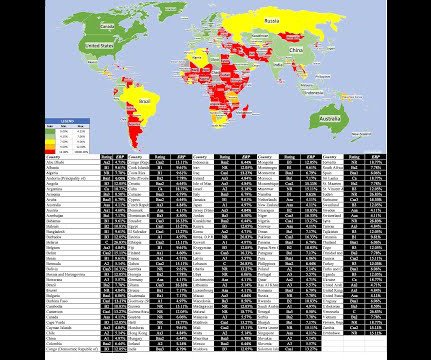

Country Risk in Business Most corporatefinance classes and textbooks leave students with the proposition that the right hurdlerate to use in assessing business investments is the cost of capital, but create a host of confusion about what exactly that cost of capital measures.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content