This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

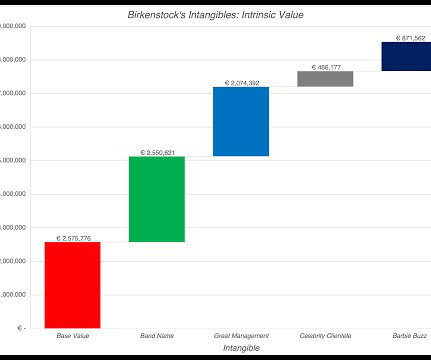

The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies.

Consequently, I will concentrate this post on how this crisis is playing out in markets, and the effects it has had, so far, on businesses and investments, and whether these effects are likely to be transient or permanent. I revisited my valuation of the index, with the updated values: Spreadsheet to value the S&P 500.

Consequently, I will concentrate this post on how this crisis is playing out in markets, and the effects it has had, so far, on businesses and investments, and whether these effects are likely to be transient or permanent. In the last few days, every company on the list has dipped in price by enough to be at least fairly valued or even cheap.

Low price stock has historically had some very large concentrated positions. And those concentrated positions happen because they have high conviction that they’re in that group where it’s not stupid to think about where earnings will be 10 years out. This is what’s wrong with concentrating in the wrong stocks.

Because going back to our thematic investing, our portfolio is 80 percent concentrated in warehouses, rental housing, lab office space and hospitality asset. Like, if you think about — when I was growing up, all of the big pharmaceutical companies had these corporate campuses that were highly securitized, deep in suburbs.

I was particularly, I was in, I was working in, on the East coast and, you know, any, everything from like pharmaceutical to automotive to, to what a, what a distribution network looked like. Doesn’t it deserve a, a richer valuation? That that’s a fairly concentrated portfolio, isn’t it? I 100% agree.

However, attempts at disruption, whether it be from Mark Cubans pharmaceutical start-up or from Google and Amazons health care endeavors, have largely left the system intact. There is another way in which you can reframe how the shifts in politics and economics will play out in valuation.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content