This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: A survey indicates that nearly 71% of new financial advisors drop out in the first 5 years, with firms offering better training and mentorship opportunities (as well as entry-level positions that don't come with business development targets) seeing higher employee retention rates How broker-dealer self-regulatory organization (..)

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

How Quality of Earnings Reports Impact Valuation Securing a Quality of Earnings (QoE) report is often a routine step in the due diligence process for acquisitions. It entails a deep dive into many facets of operations including the status of contracts, customer concentration risk, the ability to deliver services, and other expense drivers.

The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies. So, how far has accounting come in bringing intangible assets on to balance sheets?

Dividends come from earnings, and so those are sort of anchors to valuation. Jeremy Schwartz : And basically said that there’s huge Tech stocks, triple-digit PEs, you can never justify the valuations no matter what the growth rates are. They had great numbers, not great enough. And Stocks, those cash flows are dividends.

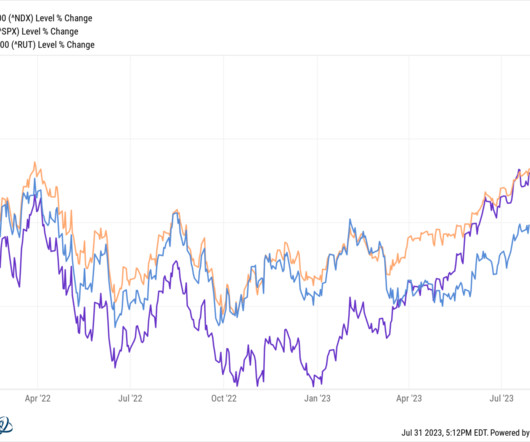

The NASDAQ also gave back gains in the third quarter, but is up 27.27% for the year, but those gaudy numbers obscure a sobering reality. In spite of losing 3.65% of their value in the third quarter of 2023, large cap stocks are still ahead 12.13% for the year, but small cap stocks are now back to where they were at the start of 2023.

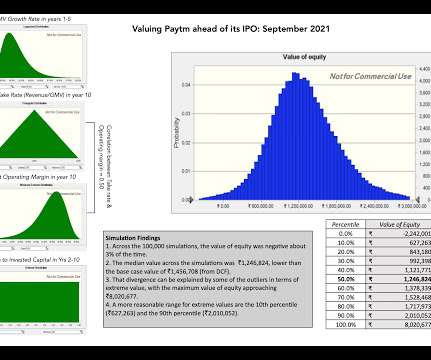

In this post, I will look at the levers that drive Paytm's value, and you can make your judgments on where you think this offering will lead in terms of valuation and pricing. As Paytm's product suite has expanded, its numbers reflect both its strengths and weaknesses, with four key statistics tracking its expansion.

Tech Concentration : Yes, a handful of giant tech stocks are driving market gains. But we won’t know how big a losing trade it might be until early 2024, when we see the updated valuations. Some folks who are more familiar with the numbers than I have suggested it will not be pretty. Never forget: Forecasts are marketing.

Wish’s filing follows a number of startups, including Snowflake, Palantir Technologies and Asana, seeking opportunities amid a crush of investors, Reuters reported. Led by General Atlantic, a New York growth equity firm, the round boosted Wish’s valuation to $11.2

Wish’s filing follows a number of startups, including Snowflake, Palantir Technologies and Asana, seeking opportunities amid a crush of investors, Reuters reported. Led by General Atlantic, a New York growth equity firm, the round boosted Wish’s valuation to $11.2

Last week, was my data week, where I download and analyze data on all publicly traded companies, listed anywhere in the world, and I will post extensively on what the numbers look like after a most tumultuous year. As we approach the turn of the calendar year, I have my own set of rituals that prepare me for the new year.

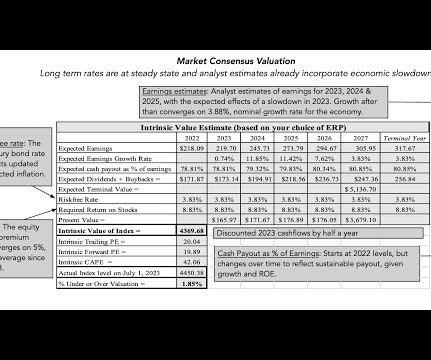

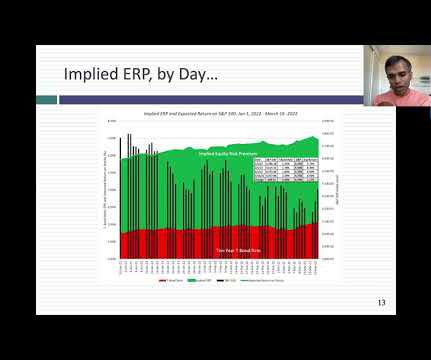

That has not happened either, as employment numbers have stayed strong, housing prices have (at least up till now) absorbed the blows from higher mortgage rates and the economy has continued to grow. In the process, the implied equity risk premium, which peaked at 5.94% on January 1, 2023, is back down to 5% at the start of July 2023.

The fact remains that venture capital firms are in the midst of raising money at a level not seen in a decade and a half, and yet, as The Wall Street Journal noted this week, the valuations of some of the highest fliers in the land of startups have started to move back toward earth, which brings to mind Icarus and the sun. With hesitation.

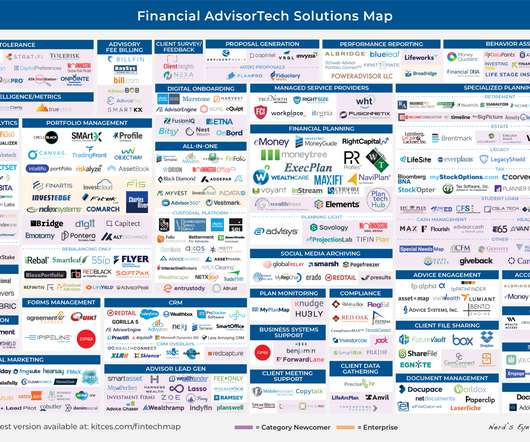

From there, the latest highlights also feature a number of other interesting advisor technology announcements, including: DPL Partners launches a new advisor-matching solution to solve for the inbound demand of consumers increasingly seeking out a new crop of no-commission annuity products. next-generation investors with smaller balances).

Tax cuts and incitements (last month regulators advocated slashing interest rates for small and mid-sized firms) mean that spending activity is concentrated within China’s borders. Valuation is at risk, and valuations are high. Ostensibly, valuation is underpinned by fundamentals.

Sujith Narayanan and Sumit Gwalani, both co-founders of Google Pay India — formerly called Google Tez — said the seed funding brings the neo-bank startup epiFi to a valuation of roughly $50 million. Last year digital payments topped 1 billion transactions in October from over 100 million people and those numbers have been steady ever since.

Heather comes from with a fascinating background, having previously been in a number of other places, most notably Morningstar, and, and she has a very specific approach to investment management and thinking about stock selection. They do a number of things at Diamond Hill that many other investment shops don’t.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. It’s, it’s double concentrated risk. 00:18:19 [Speaker Changed] Right?

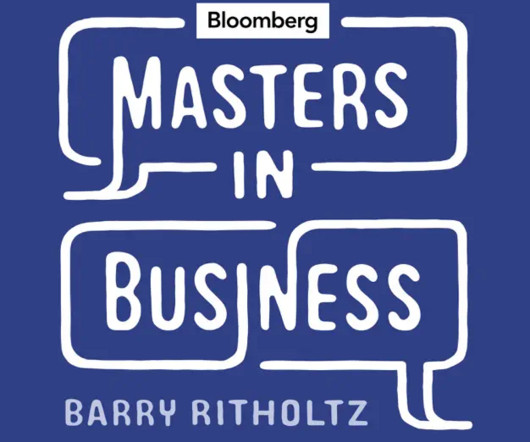

Setting the Table As with any valuation, the first step in valuing Airbnb is trying to understand its history and its business model, including how it has navigated the economic consequences of the COVID. In addition, growth in the experiences business will also push this metric upwards, since Airbnb keeps a 20% share of those revenues.

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. Second part of our framework is valuation fundamental work. So that’s, that’s number one.

They run long short across each of these, and they’ve put up some pretty impressive numbers over the past couple of years. And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. It’s beta neutral, market neutral.

So there are a number of us heading in out of college into the BLS. And how do we think about them from a valuation perspective? NORTON: Within Morningstar Investment Management, we are very much high conviction investors probably — RITHOLTZ: Meaning concentrated portfolio? I was on the Producer Price Index.

So, last year, valuations were high, interest rates were low. And I said, “Look, you’ve got to look at where we are with valuations, and you have to look at where the 10-year Treasury is at. And so, that can move the numbers, as well. And so, that can move the numbers, as well. Is it at 1.5%? Cean: Correct.

And I did the math, and I think at that point in time, roughly speaking, assets in ETS were roughly just 10 percent, 12 percent of assets in mutual funds and I was pretty convinced that that number was to increase significantly. I was employee number 10. RITHOLTZ: Which is really a pretty big number. billion dollars in AUM.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post. In a reflection of the times, there have been two developments.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. In closing, I also want to dispense with the notion that data is objective and that numbers-focused people have no bias.

Consequently, I will concentrate this post on how this crisis is playing out in markets, and the effects it has had, so far, on businesses and investments, and whether these effects are likely to be transient or permanent. I revisited my valuation of the index, with the updated values: Spreadsheet to value the S&P 500.

Consequently, I will concentrate this post on how this crisis is playing out in markets, and the effects it has had, so far, on businesses and investments, and whether these effects are likely to be transient or permanent. to 25% for the Eurozone.

And because my mother and grandmother were looking at these trying to figure out what was going on, I was curious about the sea of numbers. And 00:28:03 [Speaker Changed] That’s an amazing number. Low price stock has historically had some very large concentrated positions. If it’s a cyclical low Yeah.

And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from asset valuation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium. RITHOLTZ: So let’s talk a little bit about valuations relative to risk and reward.

Or at least the top, pick a number, 30, 40%. I don’t remember the number. ” 29, 87, 74, just pick any 50 plus percent number and certainly 2000 and ’08, ’09, a major index gets cut in half. So you’re talking about an average of a large number. What’s the valuation? Less, 20, 30%?

And if you’re able to do that in a diverse number of markets and asset classes, while managing risk in the markets that aren’t trending, you know, that’s in general how trend following works. Maybe we’ll get down to 4% or 5%, but that’s the number the Fed doesn’t like. TROPIN: Correct. TROPIN: Yeah.

I was thinking any number of things and mostly that I didn’t really know what I wanted to be when I grew up, but I was not kind of at all informed by, you know, gender norms that people asked me a lot about now, in particular how do you know a woman, how did you think about ending up in this thing? MCCARTHY: Yeah, absolutely.

This ignores the fact that the processing rails for this system — bitcoin — is concentrated in a handful of miners in China and the exchanges used to turn bitcoin into the real money that people can spend are routinely hacked. Uber invested in Lime in July as part of a $335 million capital raise that valued the company at $1.1

There’s Saunders is not spelled with a z There’s no numbers added to it. If 00:34:44 [Speaker Changed] You, so wait, gimme those numbers again. You still get these, you know, cap driven concentration problems in the market like last year. Pretty, pretty good numbers. But, but the big ones he really nailed.

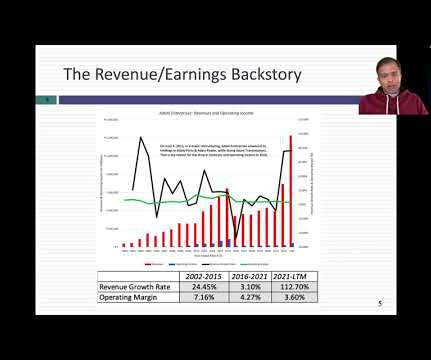

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like market capitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like market capitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago.

That "small cap premium" has found its way into valuation practitioners playbooks, manifesting as an augmentation (of between 3-5%) on the cost of equity of small companies. To get a sense of how market capitalization was related to returns, I classified all publicly traded US companies, by market cap, and looked at their returns in 2024.

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

In addition to being a portfolio manager and running a number of mutual funds and ETFs, he is just a world-class technology investor who understands the sector like few other people do. And you want to get every, every number right? Doesn’t it deserve a, a richer valuation? I’m shocked it’s only 29%.

These 10% are what’s driving the entire valuation. 00:16:27 [Speaker Changed] How much of what’s been going on in the 2020s has been a focus on that same top 10% of tech companies as being overly concentrated and wildly expensive. The parallels are that there is a concentration of interest.

We also have a number of articles on taxes and end-of-year planning: The importance for advisors of understanding current RMD rules to ensure their clients take the proper distributions (and avoid a 50% penalty in the process!). While private valuations have soared in recent years, public markets continue to be less kind to RIAs.

And since that happened, I don’t know, about four or five years ago, the fund has been putting up great numbers, outperforming doing really, really well. And since we’re looking for narratives as opposed, and then do valuation work second as opposed to cheap, we don’t screen. Is that a fair statement?

’cause L-I-B-O-R was probably the most important number, certainly in credit, maybe in all of finance. Number one, the economy’s a lot stronger than they thought it was gonna be. We just had a giant number, a giant upside surprise in payrolls. He said, oh, it’d take at least two or three weeks, really?

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content