This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Advice on concentrating your portfolio and having a margin of safety, both value investing nostrums, may work with the former but not with the latter.

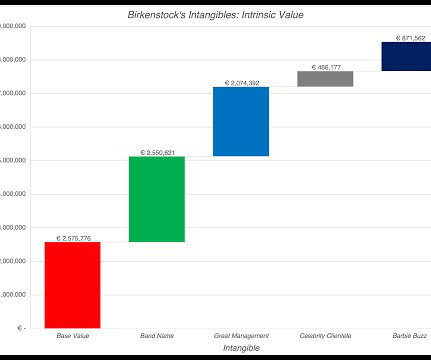

The Value of Intangible Assets Accounting has historically done a poor job dealing with intangible assets, and as the economy has transitioned away from a manufacturing-dominated twentieth century to the technology and services focused economy of the twenty first century, that failure has become more apparent.

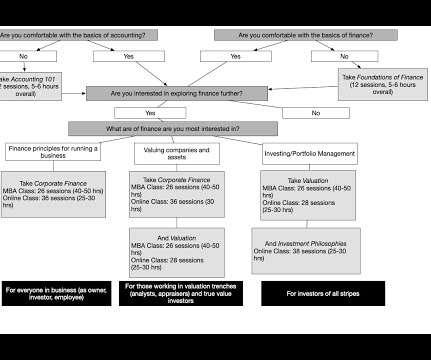

I end the class with a corporate finance version of valuation, where I tie inputs into value (cash flows, growth and risk) to investment, financing and dividend decisions. Valuation : It is unfortunate, but for most people, the vision that comes to mind when I say that I teach valuation is excel spreadsheets and high profile company names.

perhaps not surprisingly, given the two transactions just mentioned — represented the bulk of concentration, to the tune of 86 percent of all investment activity. A large manufacturer in the U.S. Another company reduced equipment failures between scheduled maintenance by 50 percent, lowering costs and downtime.

And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. 00:21:47 [Speaker Changed] And a lot of funds that have found success seem to have run some pretty concentrated portfolios. You don’t take that approach.

And we’re having very good conversations with clients that I think, at current valuation levels, they remain, you know, very interested in the market and they see some opportunities. So I think many of these car manufacturers can see the writing on the wall. RITHOLTZ: Yeah.

In parallel, I also noted that investors have to change the way they value and price companies, to reflect where they are in the life cycle, and how different investment philosophies lead you to concentrated picks in different phases of the life cycle.

Note that the rise has not been all happenstance, and China deserves credit for taking advantage of the opportunities offered by globalization, making itself first the hub for global manufacturing and then using its increasing wealth to build its infrastructure and institutions. The clearest loser from disruption is the status quo.

You still get these, you know, cap driven concentration problems in the market like last year. But we subsequently went into recession like conditions for many of those goods oriented categories like manufacturing and housing, housing related, a lot of consumer oriented products and goods that were big beneficiaries of the lockdown phase.

And they essentially take companies as varied as tire manufacturers and industrial producers and retailers, and find intelligent ways to use technology to make these companies more efficient, more productive, more profitable. These 10% are what’s driving the entire valuation. Much more involved than a consulting firm.

It really, it was the first entree into a company, not only a company a, this was a automation company that’s often known for, works with many industries, but helping automate, we were help, I was working on projects to automate manufacturing. Doesn’t it deserve a, a richer valuation? I’m shocked it’s only 29%.

In the Chinese workforce over the next decade, meaning a hundred million people, fewer working in the service sector, in the manufacturing sector, a hundred million people, fewer paying taxes, a hundred million people, fewer demanding housing and at different housing needs. That means that we are removing a hundred million people.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content