This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Advice on concentrating your portfolio and having a margin of safety, both value investing nostrums, may work with the former but not with the latter.

Those that closed a deal often paid way too much, or at least passed the companies along to public markets at inflated valuations. Higher interest rates have cut the global total of initial public offerings nearly in half since 2021, reducing targets’ leverage on valuation. billion “merger” with Churchill Capital Corp.

As a result, the ‘traditional’ valuation of an advisory firm wasn’t really 2X revenue; it was 6-8X profits, and when advisory firms can run 25% to 30% profit margins, 7X profits at 28% margins came out to almost exactly 2X revenue. (In When it comes to technology firms, revenue valuation multiples are often much higher.

And so I kind of leveraged that when I went to Morningstar because they’re very focused on quality, the whole concept of economic moats, but also about buying companies when they’re trading at a discount to intrinsic value. But there’s always gotta be some element of the valuation really being compelling.

And I think that’s reflective of employee having a lot of leverage over employers. TROPIN: I mean, you know, there were equity hedge funds that were pretty levered, that had pretty highly concentrated, you know, growth bets, and a lot of technology companies and so on. RITHOLTZ: Right. And free lunch. But we’re not there.

And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. 00:21:47 [Speaker Changed] And a lot of funds that have found success seem to have run some pretty concentrated portfolios. You don’t take that approach.

So if it’s, for example, a strategy tracking a Nasdaq Index, or an S&P, or a MSCI, typically, you leverage an index that is already available through the index providers. I mean, I do think there is a market for leverage and inverse ETFs out there. Tell us a little bit about what that process is like. RITHOLTZ: Yeah.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. That’s amazing leverage. It’s, it’s double concentrated risk.

While private valuations have soared in recent years, public markets continue to be less kind to RIAs. Altogether, Morningstar appears to be seeking to leverage the depth of its investment research and data as well as its existing investment management platform to offer a competitive direct indexing alternative for advisors.

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. Second part of our framework is valuation fundamental work. Well, that means valuations are probably too high.

Just like the original notion of giving idle black car drivers an opportunity to fill in the gaps between appointments with a few gigs, those drivers now powered a local fleet that could leverage its logistics expertise to expand the Uber ecosystem and power new services. Uber Eats users concentrate 53.6 Closing The Loop.

You do the math and you’re like, “Okay, well, an advisor can handle about 100 clients, an associate advisor can help with some of those clients, you can leverage maybe an associate advisor with a couple of advisors, but there’s a capacity limit for each of the roles.” Is it at 1.5%? And then we have the 0% cap.

The exposure you get in investment banking, I was a leveraged finance banker by background. And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from asset valuation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium.

Because going back to our thematic investing, our portfolio is 80 percent concentrated in warehouses, rental housing, lab office space and hospitality asset. MCCARTHY: — and really concentrated the business in those best markets, and then helped to grow. RITHOLTZ: Lab — so we’ll get to hospitality. Cambridge U.K.,

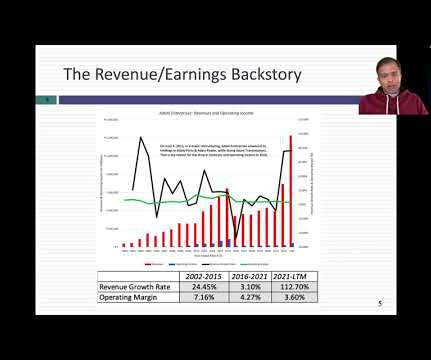

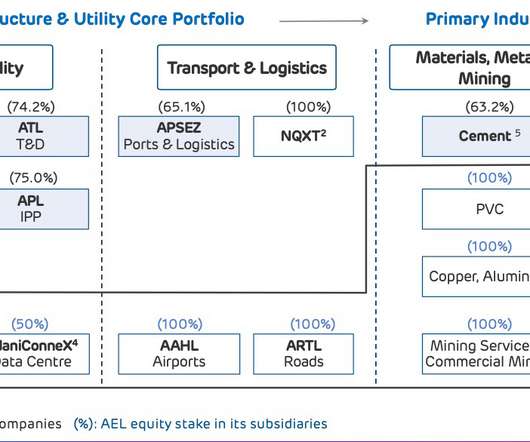

In fact, the infrastructure business is full of companies that borrow heavily, with little or no earnings buffer, and I am not sure that many of them will withstand the Hindenburg test for over leverage. YouTube Video Datasets Adani Enterprises- Historical Financial Data Spreadsheets Valuation of Adani Enterprises on February 4, 2023

In fact, the infrastructure business is full of companies that borrow heavily, with little or no earnings buffer, and I am not sure that many of them will withstand the Hindenburg test for over leverage.

One, two, there was a theory that these businesses had volatile cash flows and therefore couldn’t be leveraged, which was the, you know, the whole point of leveraged buyouts. These 10% are what’s driving the entire valuation. The parallels are that there is a concentration of interest.

But I think the reality is right now, we just have an overhang from, I certainly in my world, I can speak to healthcare and FinTech, a number of companies going public and then disappointing or valuation just being excessive compared to the maturity of the businesses. Like that was an area you could just tell the tailwinds were there.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content