This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

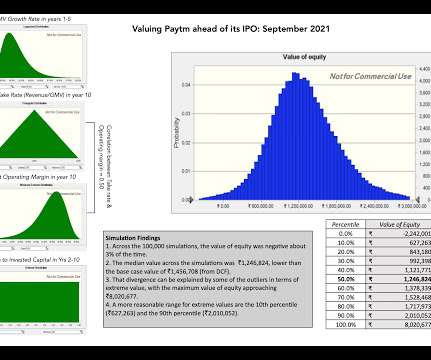

In this post, I will look at the levers that drive Paytm's value, and you can make your judgments on where you think this offering will lead in terms of valuation and pricing. I know that there are many on both sides of the value divide who will disagree with me on my story and valuation, and that is par for the course.

I think actually if you go public, there tends to be a more of a concentration in owners holding founder 00:17:41 [Speaker Changed] Stock. But there’s always gotta be some element of the valuation really being compelling. But maybe second to valuation as a primary consideration. It’s about 80%.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. And so it is important that at least you’re able to entertain that.

And speaking of the.com implosion, like Microsoft via a case study where we, in previous strategies, we held Microsoft for a very long time, that’s where the valuation could help us in the.com bus. As long as the growth rate is there and the the value is reasonable, there’s an opportunity. 00:18:41 [Speaker Changed] Yep.

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. Second part of our framework is valuation fundamental work. Well, that means valuations are probably too high.

And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. 00:21:47 [Speaker Changed] And a lot of funds that have found success seem to have run some pretty concentrated portfolios. You don’t take that approach.

And how do we think about them from a valuation perspective? And actually, that sweet, that collection of strategies, which is in the Morningstar alternatives fund is where a lot of our portfolio managers were turning to at the end of last year when, you know, fixed income is so poor on a prospective basis, equity, valuations are really high.

And we’re having very good conversations with clients that I think, at current valuation levels, they remain, you know, very interested in the market and they see some opportunities. I think I mentioned earlier, I have like a four-and-a-half-year-old that keeps me really entertain. What were you watching or listening to?

What’s the valuation? So that comes out in position sizing and conviction and just making sure that you’re thinking about all the things that could go wrong if you’re taking a more concentrated position in something. It’s just entertainment. What’s keeping you entertained during lockdown?

And so we go back to the basics of what our job should be, risk underwriting, risk assessment, asset prices are different from asset valuation. I mean the valuation is the future cash flow discounted at a risk-free rate plus a risk premium. RITHOLTZ: So let’s talk a little bit about valuations relative to risk and reward.

Low price stock has historically had some very large concentrated positions. And those concentrated positions happen because they have high conviction that they’re in that group where it’s not stupid to think about where earnings will be 10 years out. This is what’s wrong with concentrating in the wrong stocks.

Because going back to our thematic investing, our portfolio is 80 percent concentrated in warehouses, rental housing, lab office space and hospitality asset. MCCARTHY: — and really concentrated the business in those best markets, and then helped to grow. RITHOLTZ: Lab — so we’ll get to hospitality. Cambridge U.K.,

TROPIN: I mean, you know, there were equity hedge funds that were pretty levered, that had pretty highly concentrated, you know, growth bets, and a lot of technology companies and so on. And last market question, so we’ve seen equity valuations come down. TROPIN: Well, I wouldn’t go so far as to say much cheaper valuation.

You still get these, you know, cap driven concentration problems in the market like last year. The weakness that led to the first half of 2022, having no real growth in the economy was concentrated. It was concentrated on the good side of the economy manufacturing. It is represented a, a reconnection of fundamentals to prices.

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

Doesn’t it deserve a, a richer valuation? One is just generally on the valuation question with technology and similarly, the market concentration of the magnificent seven. That that’s a fairly concentrated portfolio, isn’t it? I’m shocked it’s only 29%. 00:18:34 [Speaker Changed] 100% agree.

These 10% are what’s driving the entire valuation. 00:16:27 [Speaker Changed] How much of what’s been going on in the 2020s has been a focus on that same top 10% of tech companies as being overly concentrated and wildly expensive. The parallels are that there is a concentration of interest.

And since we’re looking for narratives as opposed, and then do valuation work second as opposed to cheap, we don’t screen. You’re outperforming, you’re, you’re putting up good numbers that’s on a concentrated portfolio and it’s 10, 15, 20 stocks are the drivers. Real really interesting.

I think there are definitely commercial banks that are gonna have trouble due to their concentrated commercial office building portfolio. Starting with what’s keeping you entertained these days? You know, Lee Child’s entertaining. 01:17:31 [Speaker Changed] Le Lee Child is entertaining. All right.

How do you think about valuations for both equities and fixed income here in the beginning of 2025? And the answer to that is that the Sheila cyclically adjusted PE ratio, which is an attempt to try to correct the stock market valuations for the business cycle, is currently at a very elevated 37. What are you watching or listening to?

But I think the reality is right now, we just have an overhang from, I certainly in my world, I can speak to healthcare and FinTech, a number of companies going public and then disappointing or valuation just being excessive compared to the maturity of the businesses. What’s keeping you entertained?

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content