This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

But when you look at emerging markets and when you look at value, the opportunity for alpha is much, much greater than it is in traditional large cap growth stocks in the US And a lot of managers in that space actually beat their benchmark. So I decided to become an economics major and a psychology minor. Christine Philpots.

You can learn how you compare to your competitors and best in class by benchmarking your performance to a peer group. For instance, if your benchmarking shows a gross profit margin below the industry, that may signal excessive Cost of Goods Sold or Cost of Sales, suggesting operational or supplier agreement issues.

Forecasts can be short-term or long-term and are usually based on assumptions about factors like market conditions, customer behavior, economic trends, and internal capabilities. This could include factors such as market conditions, industry trends, customer behavior, economic indicators, and regulatory changes.

And so, coming out of school, I studied Economics and Spanish Literature, and I applied to a — a program that actually targeted Liberal Arts majors. You have a background, undergraduate, your economics degree from Notre Dame, but you were dual-major Spanish language and Literature degree, how useful was that in Latin America?

Maria Vassalou has a fascinating history and background, London School of Economics to Columbia School of Business, where she actually was a professor for over a decade, and started consulting to the hedge fund and financial services industry. The hedge fund industry, generally, is outperforming their benchmarks.

So a variety of risk meetings, a variety of economic meetings. They create the benchmark. So when there’s a major turnover like that that happens, you always have the option, “Hey, can you do it exactly on the time that it enters the benchmark? So, our active team has been successful outperforming their benchmarks.

A bachelor’s in economics from Northwestern and then an MBA from University of Chicago. And so I kind of leveraged that when I went to Morningstar because they’re very focused on quality, the whole concept of economic moats, but also about buying companies when they’re trading at a discount to intrinsic value.

So I leave the Bureau of Labor Statistics and I move into economic consulting. NORTON: Concentrated portfolios or willing to stick our necks out and look different than a benchmark. You know, pretending to be active but mimicking the benchmark because of how big, you know, the big six companies in the U.S. NORTON: Right.

So I actually went and worked in economics, I was an econometrician. Interestingly enough, there’s only, you know, a handful of validators actually benchmark themselves to real returns. So you may see portfolios change as a result of, of benchmarking. What kept you entertained during the pandemic?

And in order to graduate from Cook you had to have at least a minor that was related, and I thought — I took an econ class and I kind of liked it, so I minored in environmental economics. I — because obviously, I’m like journalism, economics, I’m in Rutgers. RITHOLTZ: Interesting. But I — I got rejected. So Bogle ….

Its index and its benchmark. There’s also quantitative metrics that we look at Those have evolved, but always within that capa, that cluster of high returns on investment stability across the economic cycle are consistent and strong balance sheets. What’s been keeping you entertained either video or audio?

00:15:29 [Speaker Changed] That’s your benchmark, correct? Starting with what’s keeping you entertained these days? I got, you know, it’s my, it’s my treadmill entertainment, so I’m slowly catching up and, and then the one that I watched recently that I absolutely loved was The Bear. All right.

And they also have a unique approach to feeds when they’re generating alpha, when they’re outperforming their benchmark, they take a performance fee. A degree in mathematics from Oxford, a doctorate in mathematical epidemiology and economics from Cambridge. What made you add economics to your, to your graduate degree?

And because remember, Lehman had the Lehman Agg and that was the benchmark. There is above benchmark returns to be generated by active selection of credit quality duration and specific bonds. RIEDER: And all of a sudden, you change the economic paradigm so darn fast. There is alpha. Can you manage that through downturns?

And the advice that he gave to David Einhorn about it that helped lead Einhorn to start really kicking the benchmark’s butt again for the past couple of years. And so it is important that at least you’re able to entertain that. I found this conversation to be both interesting and surprising.

SEIDES: If the S&P is your benchmark, which it isn’t for these pools of capital. RITHOLTZ: What should be their benchmark? So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in. So what do you use for a benchmark? 14, 15% a year? RITHOLTZ: Right.

economics, correct. RITHOLTZ: Oh, not the control, just the economics. capital problem helps improve our economic sharing …. CONROD: I — I think the — in this low interest rate environment people are looking for yield and income, and how do they — they have a — they have a benchmark. What — what’s keeping you entertained?

He has absolutely crushed his benchmark over that period. He’s crushed the Russell 2000, whatever benchmark you want to talk about. You’re 34th, you’re retiring after 34 years and you trounce what’s really the more appropriate benchmark, I would assume the Russell 2000. a year since 1989. Much better.

10 years ago you had the top economics, economists, investors in America writing a letter to the Fed in 2010 saying, “Hey, stop QE. In 2015, Bill Gurley at Benchmark was saying Silicon Valley is in a bubble. What’s entertaining the family? So obvious, but I would argue 10 years ago it wasn’t so obvious.

So 00:09:10 [Speaker Changed] I know Orion for many years because from the RIA perspective, from a registered investment advisor perspective, clients want to know how their portfolios are doing, what their performance is, both in absolute terms and relative to benchmarks. And something that Orion’s a big part of. Not too bad then.

RITHOLTZ: And last question about the various teams, does everybody have a different benchmark? How do you contextualize the economic data and the broad stamp recession when you’re thinking about managing risk? How does this impact global trade and other economic factors? How do you track performance? TROPIN: Yeah.

You get a BA in Economics from Hamilton College. So what we did was we figured out the economic rationale, the macroeconomic influences about why growth and value work at any point in time. RITHOLTZ: I mean, you didn’t do great bonds, but you didn’t do as bad as the benchmark — BERNSTEIN: Absolutely. BERNSTEIN: Yes.

You get a BA in economics and poli sci from the University of Delaware. And it had to do with the discipline of the models that he used and how he segmented economic liquidity, investor liquidity, and then technicals and and breath conditions and understood how they melded together. What was the original career plan?

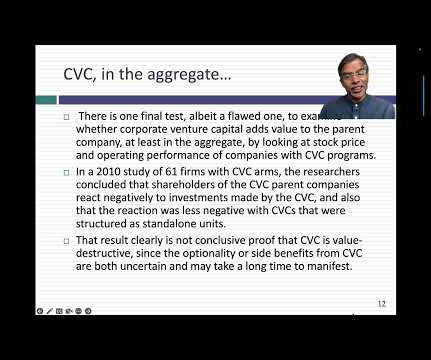

The motivations for the practice vary, and the payoff from CVC is debatable, but it is undeniable that CVC is growing as a segment of venture capital, and that it is not only affecting the pricing of the young companies that are targeted, but also altering the economics of venture capital, in the aggregate.

And I literally just started putting adjectives and nouns on piece of paper, trying to figure out like how do I describe the work that I think I should be doing, and that hopefully, people find at least entertaining, if not valuable? It seems like an easy one, but there’s a lot of missed benchmarking that goes on. NADIG: FRDM.

Let’s just jump right into this undergraduate Vienna University of Economics and Business. 00:01:40 [Speaker Changed] So yeah, I was born and raised in Vienna and went to the Vienna University of Economics, but actually raced in junior formulas at the time and wanted to be a race driver. What keeps you entertained?

You know, I think of like a Mike Spies or at Sutter Hill, you know, a Martine Cado and Andreessen, you know, Gurley when he was at Benchmark. It’s 00:52:47 [Speaker Changed] A tough benchmark to beat. What’s keeping you entertained these days? There are world class partners of ours in Silicon Valley. So terrific.

And it’s gotten ver like the average active fund has gotten closer and closer to the benchmark over the last five years. I know you like to discuss there are different phases of the, of the, both the market and the economic cycle. I mean, we had a global pandemic, a complete shutdown of global economic activity.

You graduate with a bachelor’s in economics. They can’t trade other asset classes, they can’t, you know, utilize any kind of sophisticated investment techniques to try to beat that benchmark portable alpha, get rid of all of those constraints. What’s keeping you entertained?

You get an economics PhD from California, Berkeley in 82, and around the same time you become an economist at the Federal Reserve Board from 81 to 83. And, and since then, you, you’ve gone on to do some work reforming L-I-B-O-R as the benchmark for rates. Let, let’s talk a little bit about your background.

They take a benchmark in that case, the aggregate index is by bar the, the most common one used. Let, let’s allow you to do more and have a wider degree of risk and off benchmark in your sector. The young constraint typically does not have a benchmark. Well, there’s not really that much difference.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content