This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I spend most of my time in the far less rarefied air of corporate finance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

For the segment of my data that is macroeconomic, my primary source is FRED, the data set maintained by the Federal Reserve Bank , but I supplement with other data that I found online, including NAIC for bond spread data and Political Risk Services (PRS) for country risk scores. Insider, CEO & Institutional holdings 2. Beta & Risk 1.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post. and the reverse will occur, when risk-free rates drop.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. Data Update 4 for 2021: The HurdleRate Question. Data Update 2 for 2021: The Price of Risk!

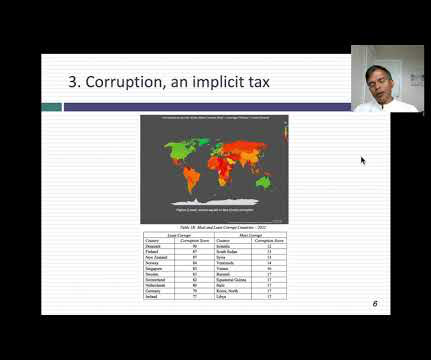

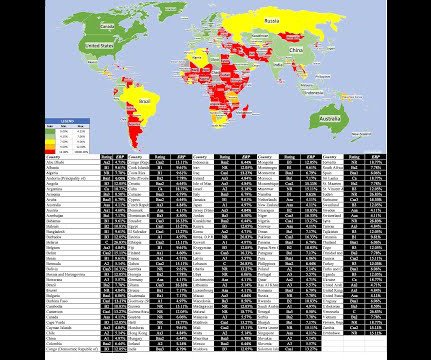

There are many services, including the World Bank and the Economist, who offer comprehensive country risk scores, and the map below includes composite country risk scores from Political Risk Services in June 2023: The pluses and minuses of comprehensive risk scores are visible in this table.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. And Jeremy said, “Well, at least there’s enough structural redundancy in the banking system.”

Investment banks were not really a known concept in the area where I grew up. I lined up a bunch of job interviews with a variety of banks. So I got to know banks a little bit. So I interviewed with a bunch of banks, got a number of job offers by the end of the week, and joined Goldman Sachs in October 1998.

That said, I have tried other country risk scoring services (the Economist, The World Bank) and I find myself disagreeing with individual country scoring there as well. As I will argue in this section, currency choice affects your growth, cash flow and discount rate estimates, but ultimately should have no effect on intrinsic value.

The transcript from this week’s, MiB: Savita Subramanian, US Equity & Quantitative Strategy, Bank of America , is below. They got bought by Bank America. And I think you will also, with no further ado, my discussion with Bank of America’s Savita. What can I say? Savita Sub Romanian, formerly of Merrill Lynch.

This was the era, 2005, 2006, all of my friends were looking to get banking roles. And so we, we get this contract written and I go off to grad school assuming I would go work at a big bank doing sales and trading in some quant role. A lot of them went to big banks. And I just sort of grew and evolved from there.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content