This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions. It deepens the acquaintance because you encounter hurdlerates in almost every aspect of finance, and it ruins it, by making these hurdlerates all about equations and models.

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

For the segment of my data that is macroeconomic, my primary source is FRED, the data set maintained by the Federal Reserve Bank , but I supplement with other data that I found online, including NAIC for bond spread data and Political Risk Services (PRS) for country risk scores. Insider, CEO & Institutional holdings 2. Beta & Risk 1.

Financial institutions can better understand the risk profiles of small suppliers by leveraging alternative data and machine learning, thus expanding access to financing. This has also led many banks to participate in third-party platforms focused on micro, small, and midsize enterprise (MSME) finance.

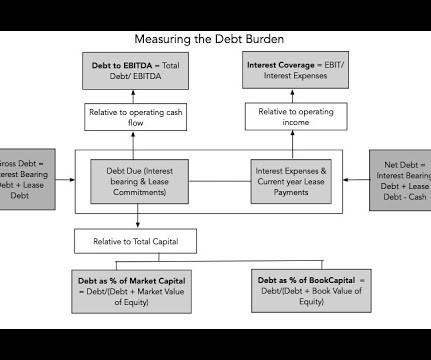

Note that this framework applies for all businesses, from the smallest, privately owned businesses, where debt takes the form of bank loans and even credit card borrowing and equity is owner savings, the largest publicly traded companies, where debt can be in the form of corporate bonds and equity is shares held by public market investors.

Investment banks were not really a known concept in the area where I grew up. I lined up a bunch of job interviews with a variety of banks. So I got to know banks a little bit. So I interviewed with a bunch of banks, got a number of job offers by the end of the week, and joined Goldman Sachs in October 1998.

His latest book could not be more timely, “The Price of Time: The Real Story of Interest,” it’s all about the history of interest rates, money lending, investing speculation, funded by banks and loans and credit. And Jeremy said, “Well, at least there’s enough structural redundancy in the banking system.”

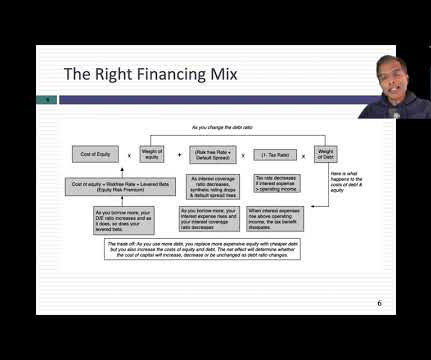

The cost of debt is lower than the cost of equity : If you review my sixth data update on hurdlerates , and go through my cost of capital calculation, there is one inescapable conclusion. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks! Data Update 5 for 2025: It's a small world, after all!

This was the era, 2005, 2006, all of my friends were looking to get banking roles. And so we, we get this contract written and I go off to grad school assuming I would go work at a big bank doing sales and trading in some quant role. A lot of them went to big banks. This is implicitly leverage. That’s amazing.]

00:26:19 [Speaker Changed] It, it’s, it’s usually it is aggressive shorts from leveraged funds on s and p futures. So it’s gonna take a little more confidence, you know, and equities to, because you get your, your hurdlerates higher, you know? You can see it also in futures positioning.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content