This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Chinas financial sector, from banks to brokerages, is rapidly incorporating DeepSeek, the nations champion in AI, for customer service, data analysis, and email sorting. Customer chatbots running on DeepSeek are the most common financial sector applications.

The majority of leaders at financial institutions say interest rates will drive business model guidance this year but few are leveraging financialdata to support these changes.

marked its third anniversary of adopting its open banking framework, making it the leading market to drive the concept of unlocking customers’ bank account data for integration with third-party solution providers. where there is no open banking regulatory mandate. HashCash Brings Blockchain Tech To Unnamed Bank.

Not drowning in a lake of data When you think about it, treasury data, in general, is not unstructured terabytes. They comprise cash balances, bank statements and financial transactions, internal and external. They are relatively centralized, organized, and available.

In banking, collaboration — between the traditional players like banks and the tech savvy FinTechs bringing a slew of new apps to market — is key. Increasingly, open banking will underpin that collaboration. Access for the consumer though means access to that far-flung data is paramount for the banks and third parties.

The approach to financial services for consumers and businesses is quite vast, but across the spectrum, access to and management of financialdata is a critical component. Finicity , a company built for financialdata aggregation, is jumping into the conversation.

Financialdata is one of the most valuable commodities in the world, and consumers have the right to control who gets access to it. Through customer-permissioned data sharing, central interfaces and the emergence of the consumer data right, consumers are the main beneficiaries of Open Banking.

The announcement by the Consumer Financial Protection Bureau ( CFPB ) comes on the heels of a symposium it held in February which included experts from consumer groups, financial technology (FinTech) companies, trade groups, banks and data aggregators.

The pandemic is reshaping banking. The conversation came against a backdrop where, as noted in a recent PYMNTS Tracker , a majority of Americans did their banking online last year. As more banking has shifted online, an increasing amount of that online activity is occurring across mobile conduits. Convenience matters, too.

Earlier this year, the European digital bank had taken on Ireland, France and Italy. In a press release, Revolut said the latest expansion would bring open banking to its users in Germany. Revolut said its new open banking offer was developed with TrueLayer , a London-based financial technology (FinTech) company.

As banks look to streamline access to finance or make it easier to safely share financial information with apps, Barclays Business Banking and Wells Fargo are joining forces with FinTechs on digital initiatives. PYMNTS rounds up the latest partnerships and initiatives below. Barclays & Propel.

When Stripe announced earlier this month that it was collaborating with the likes of Citigroup, Goldman Sachs and Barclays to embed a range of financial services within its Stripe Treasury offering, it was a big step forward for the Banking-as-a-Service (BaaS) landscape. A Phased Approach. The Corporate Use Case.

The Saudi Arabian Monetary Authority (SAMA) is introducing an open banking policy to advance digital innovation in the financial services sector. Saudi Arabia’s central bank said the plan is for open banking to go live in the first half of 2022.

financial institutions as they scrambled to apply for Paycheck Protection Program (PPP) loans under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. Bank of America received criticism for initially only allowing existing small and medium-sized businesses (SMBs) to apply. Small businesses overwhelmed U.S. Funding Circle.

Open banking is one of the most significant emerging trends in the financial industry, allowing banks and FinTechs to share financialdata in a quick, easy and secure manner across a network of platforms. Security Risks Facing Open Banking.

One of the major trends in this space is the ability to connect bank accounts seamlessly, providing real-time visibility into your financial status. Known for its advanced features, Datarails offers a seamless experience by connecting directly with your existing bank accounts, providing real-time visibility into your finances.

Open banking’s impact on small- to medium-sized businesses (SMBs) continues to proliferate as traditional financial institutions (FIs) embrace the opportunity to unlock data for third-party platforms. ’s experience is quickly influencing the way SMB lenders approach open banking in other markets like the U.S. .’s

Small businesses are a growing target for bank-FinTech collaborations and data integration initiatives as financial service providers explore new use cases for open banking. Based in Silicon Valley, Plaid said it has so far enabled integrations with 15,000 banks across the U.S. and Canada.

Every interaction tells banks what customers actually want, meaning FIs just need the right tools to interpret this data. One of the most powerful tools in the financial sector is data analytics. Big Data analytics reached a market valuation of $29.87 What is Data Analytics? Data Analytics Behind the Scenes.

million in annual turnover — had been approached by its bank repeatedly in both January and February for a loan, but the company hadn’t needed the capital. A lot of banks and lending institutions are turning companies down for a loan or funding, yet they’re never given an explanation as to why,” said Keller. Open Banking in the U.K.

We have deep dives on faster worker pay as well as cloud banking and news on WhatsApp’s payment functionality in Brazil. The Bank of China is one of over 12 commercial banks that lent to the German payment through a facility, and the move could present a mortal danger to Wirecard. Top News . Mastercard Inc.

As Open Banking spreads further into the small business (SMB) financial services market, accounting and lending platforms are taking advantage. bank sets its data sharing rules for FinTech firms. JPMorgan Sets FinTech Data Deadline. Simply Completes First Open Banking Funding. Plus, a major U.S. As the U.S.

Businesses and consumers alike are increasingly tapping new digital offerings for their financial needs as the ongoing COVID-19 pandemic shifts banking practices. Moving to cloud-supported infrastructure is one way these banks could shore up their products and keep customer interactions seamless. Around The Cloud Banking World.

Whether driven by regulation or market competition, the financial services sector in several jurisdictions is progressing toward open banking, interconnectivity and a freer flow of data between customer accounts and third parties. and multinational banks.

In this week's roundup of bank-FinTech collaboration and open banking initiatives, Citi embraces the unlocking of account data to third-party FinTechs, while WEX weighs in on opportunity for banks to take advantage of partnerships. Plus, one FinTech offers a new spin on the open banking model to drive financial inclusion.

With over 200 integrations (think ERP and CRM systems), its built to streamline financialdata management, budgeting, forecasting, and more. Ideal for financial institutions, this tool offers finance AI chatbots capable of handling everything from account management to personalized financial advice.

An application program interface (API) ecosystem is growing to transform the financial services (FinServ) sector, and small business (SMB) banking won’t be left out of the shift. APIs offer third-party FinTech firms new opportunities to make use of valuable data stored within traditional bank accounts. In the U.S.,

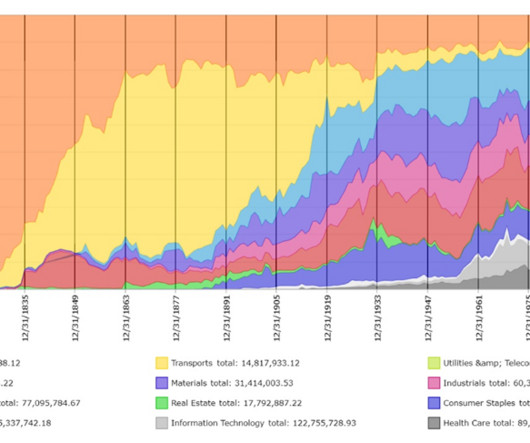

A quick break from book authorship to share a fascinating set of data and charts, via Sam Ro. In his weekly missive, Sam points to some amazing charts from Global FinancialData. They are based on historical data that looks at 200 Years of Market Concentration. You might be surprised at the findings.

The CFPB notes in its release on the upcoming inquiry that between deposits, card use, saving and tapping into a host of other common financial services — consumers create a detailed log of their financial activity — the records of which are generally kept by account issuers like banks and credit unions.

Use of alternative finance (AltFin) sources among small business (SMB) owners is on the rise, but still has a long way to go before it poses a legitimate threat to traditional banks’ market dominance. Mercator Advisory Group data released earlier this year found that 27 percent of small businesses in the U.S.

In France, Treezor , a banking as a service platform, said this week that has deployed the Thales SafeNet Data Protection On Demand solution for what is being billed as “safety across the entire payment chain, from tier one banks and neo banks to crowdfunding organizations,” as noted in a release. In the United Kingdom.

We’re being a bit tongue in cheek, but the fact remains that digital-only banking is getting a wider embrace – especially in Europe, as the pandemic surges yet again. Open banking, of course, allows financialdata to be shared and synthesized across everyday financial life, making banking by app far less of a novelty than it once was.

Treasury functions are no longer isolated; they require seamless communication between ERP systems, banks, and financialdata providers. This interconnectedness ensures accurate, real-time financial insights. Connectivity goes beyond data aggregation.

Open Banking, the U.K. bank-funded entity that was mandated by the Competition and Markets Authority to provide new ways for customers to share their financialdata with non-bank providers, has released an API specification for accounts and transaction information and payments initiation.

Open banking platform Tink continues to set a strong pace for growth with the acquisition of U.K.-based based OpenWrks , a provider of open banking applications. Tink enables FinTechs to access customers’ financialdata. Build the future of financial services,” Tink’s website urges. and Ireland country manager.

Open Banking could be expanded soon to allow for data sharing between a much larger range of finance companies, according to the Financial Conduct Authority (FCA). Open Banking allows bank customers to share their financialdata with other people and companies. In the U.K.,

Today in B2B payments, European banks grow wary of small business loans, and Xero collaborates on API bank connectivity. SMB Loans Pose Potential Big Risk for European Banks. Euro area banks have cut back on lending, as the pandemic continues to threaten the economy. Xero, Nedbank Team on API-Enabled Bank Feed for SMBs.

What we’re trying to do is leverage open banking to replicate a FedEx or Amazon experience where businesses know where their payment is at any given point of time, so they have real-time cash flow positioning.”. And the world of financial services is built on trust. That is a powerful offering.

The API seems to be on everybody’s lips, a catchphrase or buzzword for a sea change in banking that has the potential to upend the way we do business across any type of interaction. APIs are most readily recognizable as having been codified in the Open Banking concept that debuted in the U.K. About Time For Real Time?

But there’s a new data revolution underway and this one is on the consumer side, as financialdata aggregators are very much in the news. Last week, the Department of Justice gave the green light to Mastercard’s $825 million acquisition of data aggregator Finicity. bank accounts.

For proponents of open banking , the regulatory initiative seen in the U.K. While policymakers target protection and customer ownership of data, one of the most prominent selling points for open banking is the ability for data to move seamlessly between once-siloed platforms. But in jurisdictions like the U.S.

The problem can be traced back to data: as organizations scale, either through organic growth or M&A, they’re taking on more financial management platforms and opening more bank accounts, leading to fragmented storage of financialdata. Open banking is not a regulatory requirement in the U.S.,

digital ID system is now available at five Canadian banks in a mobile app, according to a report by Bloomberg. The move will help the banks take a big step forward in identity verification, using blockchain technology to give customers the ability to prove their identity digitally so they can confidently access their accounts.

Late last week, the Consumer Financial Protection Bureau (CFPB) said it will look to issue advance notice of proposed rulemaking on “open banking” by the end of this year. The path ahead for open banking, at least here in the U.S., In other words, there may be a range of potential new rules coming into play in the U.S.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content