This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Cashmanagement isn’t just about keeping tabs on your cash flow. Effective cashmanagement is a cornerstone of financial health for businesses of all sizes. One of the major trends in this space is the ability to connect bank accounts seamlessly, providing real-time visibility into your financial status.

As banks look to streamline access to finance or make it easier to safely share financial information with apps, Barclays Business Banking and Wells Fargo are joining forces with FinTechs on digital initiatives. PYMNTS rounds up the latest partnerships and initiatives below. Barclays & Propel.

In this week's roundup of bank-FinTech collaboration and open banking initiatives, Citi embraces the unlocking of account data to third-party FinTechs, while WEX weighs in on opportunity for banks to take advantage of partnerships. Plus, one FinTech offers a new spin on the open banking model to drive financial inclusion.

As the corporate treasurer takes on a more strategic role in the enterprise, treasury and cashmanagement technologies can often be stuck in the past, failing to keep up with financial execs’ needs. Despite the data challenge, pressures on CFOs and treasurers continue to mount. Even so, Turner said U.S.

And while the latest tools of the trade—artificial intelligence (AI) and machine learning (ML)—promise to make tasks such as liquidity forecasting, cashmanagement, and risk management easier, they come with their own complications and tie the treasury team even more closely into management’s strategic planning.

Basel III is a set of voluntary rules that impact banks’ risk management and capital requirements, among other things, and could lead to corporate challenges in accessing bank financing. The banking sector is moving away from offering a simple, straightforward view via statements and transaction data, Cashfac noted.

Bank is shifting away from screen scraping in favor of direct data connectivity, but it's not the only financial institution (FI) embracing the data strategy. Bank Nixes Screen Scraping With Akoya. Visa Links With Codat For SMB BankData Sharing. Atom Bank Links With Codat, Too.

While Open Banking initiatives and data integrations between banks and FinTech firms have begun to target corporate and small business (SMB) end users, new research out of the U.K. has warned that small businesses are largely shunning the opportunity to unlock their financialdata. Open Banking Startup Lands $99.9

Nordic financial services firm Nordea is introducing a new solution to provide corporates with a streamlined financial reporting solution powered by Open Banking. Last year Nordea released its Future of Payments report, urging the corporate payments industry to become standardized across banks.

Despite any possible reservations early on, large financial institutions (FIs) now appear to be going all in on Open Banking, with plans to introduce new revenue streams as a a result. The report, “It’s Now Open Banking, Do You Know What Your Commercial Clients Want From It?,” ” published Wednesday (Nov.

Major priorities over the next one to two years: We are not surprised that Cash-Flow Forecasting comes out on top when the COVID crisis has been hitting us for the past year. We all understand that the C-level wants treasury to lake use of huge financialdata they sit on and develop more reporting and dashboards.

Despite its rising popularity, open banking and data sharing frameworks were not necessarily opportunities toward which banks initially jumped. Gradually, however, traditional FIs are increasingly acknowledging the value in open banking. This is a classic build-versus-buy decision,” he told PYMNTS.

Open banking didn’t just kick off via PSD2 regulations across Europe and the U.K. Rather, banks around the globe began to understand the potential value in opening up customer data to third-party players, and with more bank APIs emerging in 2018, the year saw a surge in data sharing.

In B2B payments, that can mean discontent in the way traditional banks and FIs do business or a need for disruptive technologies to come to market faster than banks can offer. For any new FinTech company, securing a deal with a financial giant is good news. But this use case can easily be applied to other industries, too.

And, truth be told, many of them don’t put it on much at all; while some of them hire a part-time accountant or rely on their financial institution to help, that often doesn’t really cut it either. “Banks talk about the importance of the micro/small business category,” he recently told Karen Webster. and she has Wave. .

A professional cashmanagement solution can help to overcome these challenges. In the dark about global cash? Hit hard by their company’s growth, Treasurers often lose sight of their global cash. Get an overview of your company’s bank accounts and centralize bank account administration. You’re not alone!

Financial institutions are investing significantly in embracing online banking and supporting a positive digital experience for their end-users. For corporate treasurers of multinational organizations, this task isn’t merely about logging into each online banking portal, either. Tripping Up CashManagement.

This complicated process can involve everything from accounting and invoicing software to bank accounts. Today’s financial institutions (FIs) no longer need to worry about solely addressing all their clients’ financial-related needs, however. Managing these steps in separate systems can be friction-filled, Haider said.

Being able to transmit this type of data via blockchain would make B2B processes like invoice processing and payments far quicker, the company explained. Real-time payments and reconciliation, the company added, could be a major boost to corporate cashmanagement efforts, too. However, this is changing.

Open banking and its promise of more elasticity in finance is enabled by application program interfaces (APIs) — lines of code that execute everything from simple peer-to-peer (P2P) transfers to industrial-sized B2B real-time payments. As the industry marks two years since open banking’s U.K. Open Banking Opens Up.

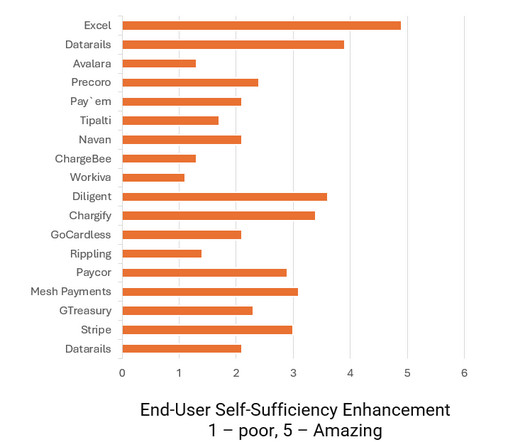

Financial analysis and planning (or FA&P) software is a type of business software that helps companies manage their finances and operational activity by analyzing financialdata and providing tools to plan, forecast and make budgets for efficient business growth.

This often involves replacing outdated ERP systems or implementing new cashmanagement solutions. Question 3: Successful Training and Adoption Which software's training and adoption process was exceptionally well-managed across different teams, facilitating a smooth transition or implementation?

Here’s all the financialdata you need to know from some of the largest B2B finance and tech businesses. Net income improved 4 percent year-over-year, while non-interest expenses declined 3 percent , the bank said. IBM missed the mark, Kyriba boasted its growth, and SAP has its S/4HANA solution to thank for a strong quarter.

Lately, companies have been discussing the role of banks in this pairing-up of old and new; financial institutions provide their capital and consumer base, while alternative FinTech players provide the innovative technology and the underlying infrastructure to connect small businesses with loans. “A

During the Singapore Circuit Breaker , the property industry stakeholders — from banks and suppliers to contractors — digitalized their documentation workflows, streamlined the processes, and adopted digital signatures to reduce the disruptive impact of locking down the human workforce. Data trust or integrity is another rising challenge.

Adam is an Associate Financial Planning Nerd at Kitces.com. He previously worked at a financial planning firm in Bethesda, Maryland, and as a journalist covering the banking and insurance industries. Outside of work, he serves as a volunteer financial planner and class instructor for non-profits in the Northern Virginia area.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content