This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Today in B2B, Bloomberg broadens its credit risk data pool, and two ERP solutions secure B2B payments integrations. Everlink, FINTAINIUM Team Up To Offer Real-Time B2B, B2C Payments. And with APSPays Vault, companies can store information securely and access reporting tools for reconciliation.

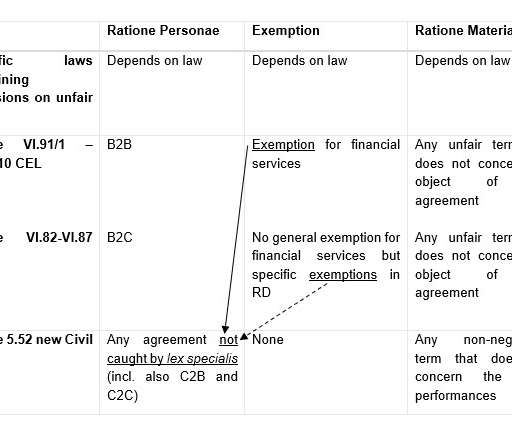

Before that, the B2B and B2C legislation had already introduced a similar prohibition, but financial services had been (partially) exempted. of the new Civil Code, the B2B and the B2C regime. of the Code of Economic Law which contains a full exemption for “financial services” [ii]. of the Code of Economic Law […].

The outmoded B2B payments landscape stands in stark contrast to the business-to-consumer (B2C) and peer-to-peer (P2P) spaces where instant money and real-time payments are becoming the norm. It works both ways as traditionally B2C sellers dip their toes into lucrative B2B waters. There are psychological benefits as well.

With a focus on enabling corporations to manage payroll in a remote work environment, India-based Skuad has reportedly secured a $4 million seed investment round , according to the Economic Times of India. Italy's Deliveristo secured a $5.51 Deliveristo. million investment, Tech.eu

She noted that firms such as PULSE have enabled payments functionality spanning push payments, peer-to-peer (P2P) and business-to-consumer (B2C) for the past decade and that operating rules require funds to be available in customer accounts within 30 minutes.”. The Security Angle.

While the B2B payments landscape is taking a page out of the B2C world's book when it comes to adopting new payment models, other paradigms are emerging that are built to tackle the unique pain points of business-to-business transactions not always seen in the consumer world. New Payment Models Emerging.

Partnering with other C-suites executives To be able to adapt with the shifts, Ho takes note of the fact that CFOs often have a seat at the Board and are required to act as the CEOs' business partner working hand-in-hand to steer the company through the current economic climate. Partnering’ is nothing new," says Ho.

Western Union CEO Hikmet Ersek told Karen Webster that real time means that receivers will have funds available to spend within minutes, enabling new real-time, cross-border, cross-currency payments capabilities for C2C, B2C and B2B use cases. “We We believe we can help FIs create opportunities and serve their customers better.”.

The pandemic and economic headwinds have spurred millions of consumers to eye their finances with caution. There are significant segments of the American consumer base that appreciate the pay-as-you-go aspect, convenience and trusted security of debit,” he said. The Shift To Safety.

The idea started in the B2C world, but it wasn’t long before online sellers were asking about the use of point-of-sale financing for B2B — at least according to Chris Tsai, co-founder and CEO of Resolve, an Affirm spin-off, in an in-depth PYMNTS interview earlier this week. How to Shake up B2B Financing at the Point of Sale.

to fully embrace real-time payments for both B2B and B2C activity.”. There’s an economic shift afoot, too, as the growth of the gig economy will likely spur Requests for Payment (RFPs) directly to companies that engage gig workers on projects. Where We Stand In The US. RTP isn’t just another payment type a bank can offer.”.

The price and complexity of more sophisticated payments collections technologies are among the tallest, Gray said, with tools like text-to-pay functionality simply not economical enough to warrant an investment — even despite a better customer experience. Accelerating Collections.

Recent reports in Citing Venture Intelligence data, LiveMint said B2B FinTech has secured $657 million in India so far this year, compared to $617 million for B2C FinTechs. B2B FinTech companies are more predictable than B2C firms,” he told the publication. “B2B

Small- to medium-sized businesses (SMBs) are now a critical component of the government’s push for economic growth. Looking ahead, Mittal noted, B2B eCommerce will play a key role in India’s economic expansion. ”

Such a move would enable people in need of such space – for, say, retailers or warehouses – to bypass the brokers typically involved in securing that real estate. Excess capacity could also be interpreted as a sign of a company’s poor economic situation and viewed critically with regard to cooperation.

B2B eCommerce doesn’t command the spotlight as does B2C retail, but that’s not the way it should be — that’s one of the messages you take away after listening to Brandon Spear, president of MSTS. Employers investing in this space is not just about making happy, healthy employees — it’s also a good economic investment.”.

In many cases, they wish to remove friction: the impediment of phone calls, expense of a high-commission salesperson, cognitive load of a sales decision and economic friction of following through — the dance between the buyer and the salesperson. Different industries are trying subscription services for a variety of reasons.

For instance, attracting B2B and B2C customers with more sustainable products can help achieve better access to resources through stronger community and government relations. It is crucial to see the pursuit of economic and environmental performance as a two-pronged innovation agenda, which is closely related.

Merritt is a former executive of Simple, an alternative banking solution for consumers, where he said he saw SMBs trying to force that B2C service to work for their B2B needs. “At Already, Brian Merritt said, he sees small businesses desperate to try something new. We think there are risks in mixing personal and business finances. “The

percent more B2C merchants than B2B merchants offer discounts, for example, and 11.1 percent more B2C merchants than B2B merchants allow their customers to rate products and write reviews. percent trust that their information is secure. Key Data Points: It takes only 78.5 Disbursement Satisfaction: Sizing The Choice Gap.

Fifth Third’s Williams noted that when speaking to CFOs and treasurers “issues that are top of mind” include the ambition that “everyone wants to streamline in some form or another … they find pressure to be more efficient economically” or to be, as he called it “opportunistic” in recognizing the potential of technology and capturing that potential.

I think the way to think about this is we’re a business-to-business organization in terms of if you’re going to look at the revenue lines, but with B2C responsibilities, right? RITHOLTZ: And security is a huge one. NADIG: And security is a huge one, knowing your customer is a big one, anti-money laundering.

That, along with tokenization and point to point encryption became the trifecta of payments security. Which suggests that the focus in payments needs to shift toward keeping customer data secure , not just the payment card information they carry around in their physical or virtual wallets. All pure goodness, with two big exceptions.

Some of the executives who offered testimony sought to paint a picture that lessons have been learned, and that things have gotten better even against the backdrop of slowing economic growth. Dimon pointed to the speed in which loans can be done through digital means, both P2P and B2C.

Some of the executives who offered testimony sought to paint a picture that lessons have been learned, and that things have gotten better even against the backdrop of slowing economic growth. Dimon pointed to the speed in which loans can be done through digital means, both P2P and B2C.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content