This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Preparing for a financial audit can be a daunting task, especially for private equity-backed firms where accuracy and efficiency are paramount. This article provides a deeper look at the steps CFOs can take to create a seamless, streamlined audit experience.

Audit season presents a set of unique challenges for private equity-backed companies, particularly those that must balance the expectations of investors with the demands of compliance. Ensure that impairment analyses are completed according to audit priorities, with asset groupings and forecast data that align with GAAP standards.

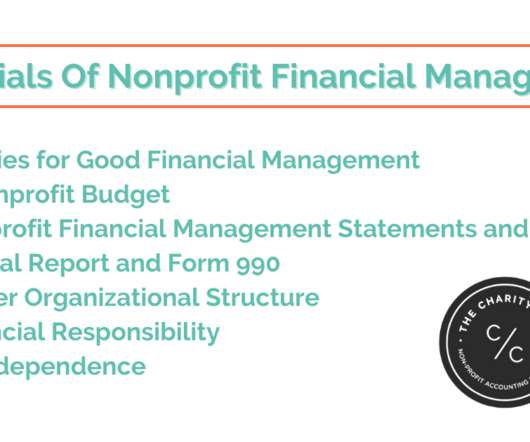

Contrary to what many people envision, a nonprofit audit doesn’t usually start with a letter from the IRS. Instead, an independent nonprofit audit is something you choose to build trust in your nonprofit organization. An audit can be a critical step for a growing nonprofit that needs to raise increasing amounts of funds.

Horton: I think auditors, for sure, because they want to know their audit risk, especially if you are taking over from a previous auditor. The Public Company Accounting Oversight Board [PCAOB] looks at companies accounts and audit papers and tries to make sure that the accounting is being done correctly. But nothings impossible.

Discover how SAP solutions lay a solid foundation for audits and next level PCAOB or AICPA compliance reviews. While passing each audit is a critically important milestone, companies also should understand that it is only one aspect of ensuring their financial transparency and integrity.

Audit season presents a set of unique challenges for private equity-backed companies, particularly those that must balance the expectations of investors with the demands of compliance. Ensure that impairment analyses are completed according to audit priorities, with asset groupings and forecast data that align with GAAP standards.

Audit season presents a set of unique challenges for private equity-backed companies, particularly those that must balance the expectations of investors with the demands of compliance. Ensure that impairment analyses are completed according to audit priorities, with asset groupings and forecast data that align with GAAP standards.

Preparing for a financial audit can be a daunting task, especially for private equity-backed firms where accuracy and efficiency are paramount. This article provides a deeper look at the steps CFOs can take to create a seamless, streamlined audit experience.

Preparing for a financial audit can be a daunting task, especially for private equity-backed firms where accuracy and efficiency are paramount. This article provides a deeper look at the steps CFOs can take to create a seamless, streamlined audit experience.

Embarking on your first financial audit can be nerve-wracking. This article includes small business accounting tips to prepare for an audit while minimizing its expenses and findings. An audit evaluates: Compliance with accounting standards (GAAP or IFRS.) Do not expect to walk away from an audit with zero findings.

Cash accounting does not comply with Generally Accepted Accounting Principles (GAAP) for nonprofit organizations. Financial statement audit or review – if you are required to undergo a financial statement audit or assessment, using the accrual method to be in accordance with GAAP will make the process much smoother and less expensive.

So now is the perfect time to make sure you report in kind gift donations in compliance with GAAP standards in 2022. The changes to in kind donation reporting are specifically for organizations that follow generally accepted accounting principles (GAAP) in preparing their financial statements.

Audits, while essential for maintaining the integrity and trustworthiness of an organization’s financial reporting, can be a daunting task. This is not just because of the intricacies and specificities required by the auditing standards but also due to the numerous challenges faced by organizations in the run-up to an audit.

The difference between cost of goods sold and ordinary business expenses is well defined in Generally Accepted Accounting Principles (GAAP) but routinely ignored by small business bookkeeping services. Even worse, an IRS income tax return does not follow the same rules as GAAP. How do I maximize tax deductions under section 280E?

AI driven automation is expected to extend to more complex tasks such as, audits, risk management, and financial planning and analysis. As AI permeates finance, questions about its compliance with audits and financial governance will arise. For instance, could financial statements generated by ChatGPT withstand audit scrutiny?

Accrual accounting is required by Generally Accepted Accounting Principles (GAAP), which means that you’ll need accrual-based reports to complete a nonprofit audit. Accrual accounting is the preferred method for any organization that needs to be audited or anticipates significant growth. Difference #3: Functional Expenses.

Both Generally Accepted Accounting Principles (GAAP) and Financial Accounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit. And the more transparent your accounting system is, the more accountable you’ll be with the public and GAAP.

In the United States, these Generally Accepted Accounting Principles (or GAAP) are set by the Financial Accounting Standards Board (FASB). The goal is to create an accurate and comprehensive record of all transactions that can be used for both internal and external reporting, including audits and tax returns. 117 (FASB 117).

Only 52% of survey respondents believe that IFRS 17 earnings / equity will be slightly or much more helpful than current GAAP earnings / equity, and 54% believe that the need for non-GAAP reporting will either slightly or significantly increase.

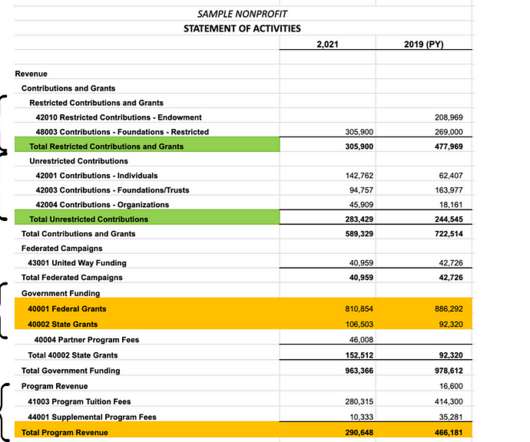

But, since auditable nonprofit financial statements, we’ll talk about accrual accounting practices in this article. To comply with Generally Accepted Accounting Principles (GAAP), you must separate your revenue into at least 2 categories: Restricted Revenue shows funds with donor-placed restrictions on how or when you can spend the money.

After he graduated, he went to work as an audit manager for Deloitte, Haskins & Sells (now Deloitte). He has worked as audit manager and controller for topline public (SEC) companies such as American Home Products, Estée Lauder, Quaker State, and GTE. He earned his CPA license and was promoted twice in four years.

Implementing robust security measures, such as encryption, access controls, and regular audits, is essential to protect sensitive financial information. Regular updates to the system to reflect changes in these regulations are also crucial.

All these sources must be carefully managed to ensure compliance with Generally Accepted Accounting Principles (GAAP) and guidelines. Failing to recognize revenue properly may lead to inaccurate financial reporting, which could result in penalties, restrictions, and audits. Undergo annual financial audits. Receive grants.

To pass an independent audit. Reporting functional expenses has been required by Generally Accepted Accounting Principles (GAAP) since 2017, as detailed in ASU 2016-14. That means you’ll need to present a Functional Expense Report to pass an audit. So you really don’t have a choice, but if you want more reasons….

How can a small business ensure compliance in reporting without overspending on accounting staff and audits? In general, financial statement compliance involves adhering to established standards and regulations, such as Generally Accepted Accounting Principles (GAAP) and the Financial Accounting Standards Board (FASB) guidelines.

Using CLM, global companies are better able to manage lease classification such as sales type leases and operating leases, as well as to meet lessor accounting requirements of US GAAP and other country GAAP requirements, or IFRS mandates. Multiple Regulatory Compliance Mandates: Meeting regulatory requirements (e.g.,

In this new role, he will serve as one of our in-house experts on existing and emerging nonprofit accounting standards and auditing best practices. In doing so, Zack will help ensure that our clients’ financials are prepared in accordance with general accepted accounting principles (GAAP) and their 990s meet IRS guidelines.

Governments taking a more flexible approach to tax audits and filing: APAC companies can extend tax/statutory filing deadlines in 50% of places and 43% allow firms to postpone the start of a tax audit.

Prepare financial statements per Generally Accepted Accounting Principles (GAAP). Submit to an annual audit. For the purposes of GAAP, donations of goods and services are valid revenue. You need to track and report in-kind donations if your organization is required to… . File IRS Form 990 ( in-kind goods only ) .

Assessing Accounting For entities preparing GAAP compliant financial statements, adoption of Revenue Recognition Standard (ASC 606) and Lease Accounting Standard (ASC 842) is now mandatory. audited or reviewed financial statements). Reviewing the asset register and eliminating assets that have been scrapped.

If your organization falls into the $50,000-$200,000 range but must complete an annual audit for funding or GAAP purposes, it is wise to skip Form 990-EZ and head straight to the full form. . When you outsource your bookkeeping and accounting to us, we’ll ensure your books are always audit-ready. Full Form 990.

The internal audit had two major and disturbing reveals. The audit discovered the then-CEO guided Lending Club’s board and risk team toward the firm’s purchase of a 15 percent limited-partnership interest in Cirrix this year for $10 million last year — without disclosing that he himself was an investor in the firm.

It should also be noted that, at least for state-registered advisers, financial statements must typically be prepared in accordance with GAAP. RIA Fee Itemization And Surprise Custody Audits.

What is the difference between a quality of earnings report and an audit? Audited financial statements focus on compliance with GAAP accounting standards, whereas Quality of Earnings reports focus on the company’s earnings history and potential.

The IRS has different reporting requirements than GAAP, so the balance sheet section of your 990 may not match your audited financial statements. They’ll be looking for any large loans, investments, your operating reserve , and your ratio of restricted to unrestricted assets. . How do you spend your money?

Nonprofits must maintain thorough and accurate financial records to comply with both Generally Accepted Accounting Principles ( GAAP ) and maintain their tax-exempt status with the IRS. With our nonprofit bookkeeping and accounting services, we’ll ensure your books are always audit-ready.

Familiarity with Generally Accepted Accounting Principles (GAAP) is essential. Additionally, you open yourself up to compliance and audit issues, and you’ll potentially decrease your chances of securing funding and financing.

As a result, the organization might not adhere to Generally Accepted Accounting Principles (GAAP), which can trip them up come tax time or during an audit. This mitigates penalties, late filings, audits, and fraud (all too common in the nonprofit sector). Prepare for and manage an annual audit. Boosts donor confidence.

Acquiring these advanced types of services, like setting up a permanent audit trail, rolling cash forecast, month-end reporting, and strategic planning, is the secret sauce your potential client needs to know how their money flows in and out of their company (and what their financial future will look like).

AI driven automation is expected to extend to more complex tasks such as, audits, risk management, and financial planning and analysis. As AI permeates finance, questions about its compliance with audits and financial governance will arise. For instance, could financial statements generated by ChatGPT withstand audit scrutiny?

When creating your fiscal policy, ensure that it complies with the Generally Accepted Accounting Principles (GAAP). Bring GAAP compliance. It also involves staying up to date on the latest auditing standards, tax regulations, and IRS filing requirements. A Nonprofit Budget. Net assets (difference between revenue and expenses).

Consolidating the financial results following US GAAP or IFRS guidelines, including these steps: Performing currency conversions. Ensuring adequate audit trails for internal and external auditors. They’ll conclude that there’s a total lack of security, control, and audit trails when using spreadsheets.

You’re preparing for an IPO or external audit, which requires having rock-solid financial statements. Multi-GAAP reporting (i.e., US GAAP, Canadian GAAP, IFRS, etc.). So what does the financial consolidation and close process entail? This includes dealing with the following issues: Currency translation.

Not being compliant with US GAAP or IFRS. Lack of controls and audit trails. Time-consuming and costly audit process. Improve audit trails, reduce audit costs. Challenges in consolidating multiple spreadsheets and correcting errors. Limited reporting and analysis capabilities, and too much manual effort.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content